Humana 1999 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 1999 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

|

|

19 9 8 EX P E NS E S

Market Exits, Non-Core Asset Sales and Merger

Dissolution Costs

On August 10, 1998, the Company and UnitedHealth Group

Company (“United”) announced their mutual agreement to

terminate the previously announced Agreement and Plan of

Merger, dated May 27, 1998. The planned merger, among

other things, was expected to improve the operating results

of the Company’s products and markets due to overlapping

markets with United. Following the merger’s termination,

the Company conducted a strategic evaluation, which

included assessing the Company’s competitive market

positions and profit potential. As a result, the Company

recognized expenses of $34 million during the third quarter

of 1998. The expenses included costs associated with exiting

five markets ($15 million), losses on disposals of non-core

assets ($12 million) and merger dissolution costs

($7 million).

The costs associated with the market exits of $15 million

included severance, lease termination costs as well as write-

offs of equipment and uncollectible provider receivables.

The planned market exits were Sarasota and Treasure

Coast, Florida, Springfield and Jefferson City, Missouri and

Puerto Rico. Severance costs were estimated based upon the

provisions of the Company’s employee benefit plans. The

plan to exit these markets was expected to reduce the

Company’s market office workforce, primarily in Puerto

Rico, by approximately 470 employees. In 1999, the

Company reversed $2 million of the severance and lease

discontinuance liabilities after the Company contractually

agreed with the Health Insurance Administration in Puerto

Rico to extend the Company’s Medicaid contract, with

more favorable terms. The Company estimated annual

pretax savings of approximately $40 million, after all

market exits were completed by June 30, 1999, primarily

from a reduction in underwriting losses. Approximately 100

employees were ultimately terminated resulting in

insignificant severance payments.

In accordance with the Company’s policy on impairment

of long-lived assets, equipment of $5 million in the exited

markets was written down to its fair value after an

evaluation of undiscounted cash flow in each of the

markets. The fair value of equipment was based upon

discounted cash flows for the same markets. Following the

write-down, the equipment was fully depreciated.

Premium Deficiency and Provider Costs

As a result of management’s assessment of the profitability

of its contracts for providing health care services to its

members in certain markets, the Company recorded a

provision for probable future losses (premium deficiency)

of $46 million during the third quarter of 1998. The

premium deficiency resulted from events prompted by the

terminated merger with United wherein the Company had

expected to realize improved operating results in those

markets that overlapped with United, including more

favorable risk-sharing arrangements. The beneficial effect

from losses charged to the premium deficiency liability

in 1999 and 1998 was $23 million and $17 million,

respectively. In 1999, the Company reversed $6 million

of premium deficiency liabilities after the Company

contractually agreed with the Health Insurance

Administration in Puerto Rico to extend the Company’s

Medicaid contract, with more favorable terms.

The Company also recorded $27 million of expense related

to receivables written-off from financially troubled

physician groups, including certain bankrupt providers.

Non-Officer Employee Incentive and Other Costs

During the third quarter of 1998, the Company recorded a

one-time incentive of $16 million paid to non-officer

employees and a $9 million settlement related to a third

party pharmacy processing contract.

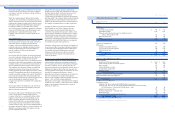

Activity related to the 1998 expenses follows:

27

19 9 9 EX P E NS E S

Premium Deficiency, Reserve Strengthening and

Provider Costs

As a result of management’s assessment of the profitability

of its contracts for providing health care services to its

members in certain markets, the Company recorded a

provision for probable future losses (premium deficiency)

of $50 million during the first quarter of 1999. Ineffective

provider risk-sharing contracts and the impact of the March

31, 1999 Columbia/HCAHealthcare Corporation

(“Columbia/HCA”) hospital agreement in Florida on

current and projected future medical costs contributed to

the premium deficiency. The beneficial effect from losses

charged to the premium deficiency liability throughout

1999 was $50 million. Because the majority of the

Company’s customers’ contracts renew annually, the

Company does not anticipate the need for a premium

deficiency in 2000, absent unanticipated adverse events or

changes in circumstances.

Prior period adverse claims development primarily in the

Company’s PPO and Medicare products initially identified

during an analysis of February and March 1999 medical

claims resulted in the $35 million reserve strengthening.

The Company releases or strengthens medical claims

reserves when favorable or adverse development in prior

periods exceed actuarial margins existing in the reserves. In

addition, the Company paid Columbia/HCA$5 million to

settle certain contractual issues associated with the March

31, 1999 hospital agreement in Florida.

Long-Lived Asset Impairment

Historical and current period operating losses in certain of

the Company’s markets prompted a review during the

fourth quarter of 1999 for the possible impairment of long-

lived assets. This review indicated that estimated future

undiscounted cash flows were insufficient to recover the

carrying value of long-lived assets, primarily goodwill,

associated with the Company’s Austin, Dallas and

Milwaukee markets. Accordingly, the Company adjusted

the carrying value of these long-lived assets to their

estimated fair value resulting in a non-cash impairment

charge of $342 million. Estimated fair value was based on

discounted cash flows.

The long-lived assets associated with the Austin and Dallas

markets primarily result from the Company’s 1997

acquisition of PCA. Operating losses in Austin and

Dallas were related to the deterioration of risk-sharing

arrangements with providers and the failure to effectively

convert the PCAoperating model and computer platform

to Humana’s. The long-lived assets associated with the

Milwaukee market primarily result from the Company’s

1994 acquisition of CareNetwork, Inc. Operating losses in

Milwaukee were the result of competitor pricing strategies

resulting in lower premium levels to large employer groups

as well as market dynamics dominated by limited provider

groups causing higher than expected medical costs.

The Company also re-evaluated the amortization period

of its goodwill and as a result, effective January 1, 2000,

adopted a 20 year amortization period from the date of

acquisition for goodwill previously amortized over

40 years.

The $342 million long-lived asset impairment will decrease

depreciation and amortization expense $13 million annually

($13 million after tax, or $0.08 per diluted share), while the

change in the amortization period of goodwill will increase

amortization expense $25 million annually ($24 million

after tax, or $0.15 per diluted share).

Losses on Non-Core Asset Sales

The Company has entered into definitive agreements for

the disposition of its workers’ compensation, Medicare

supplement and North Florida Medicaid businesses, which

are considered non-core. As a result of the carrying value of

the net assets of these businesses exceeding the estimated

sale proceeds, the Company has recorded a loss of $118

million. Estimated fair value was established based upon

definitive sale agreements, net of expected transaction costs.

These transactions are expected to be completed in the first

and second quarters of 2000. Total assets of $725 million,

primarily consisting of marketable securities and

reinsurance recoverables and total liabilities of $490 million,

primarily consisting of worker’s compensation reserves

related to these businesses are included in the

accompanying Consolidated Balance Sheets. The

accompanying Consolidated Statements of Operations

include 1999 revenues of $214 million and pretax operating

income of $38 million from these businesses. Included in

1999 and 1998 pretax operating (loss) income is $36 million

and $5 million of workers’ compensation reserve releases

resulting from favorable claim liability development.

Professional Liability Reserve Strengthening and

Other Costs

The Company insures substantially all professional liability

risks through a wholly owned captive insurance subsidiary

(the “Subsidiary”). The Subsidiary recorded an additional

$25 million expense during the fourth quarter of 1999

primarily related to expected claim and legal costs to be

incurred by the Company.

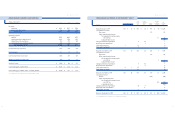

26

Balance at

1999 1999 Activity December 31,

(In millions) Expenses Cash Non-Cash 1999

Premium deficiency $ 50 $ (50) —

Reserve strengthening 35 (35) —

Provider costs 5 (5) —

Long-lived asset impairment 342 $ (342) —

Losses on non-core asset sales 118 (28) $ 90

Professional liability reserve

strengthening and other costs 35 35

$ 585 $ (90) $ (370) $ 125

Balance at Balance at

1998 1998 Activity December 31, 1999 Activity December 31,

(In millions) Expenses Cash Non-cash 1998 Cash Adjustment 1999

Premium deficiency $ 46 $ (17) $ 29 $ (23) $ (6) $ —

Provider costs 27 $ (27) —

Market exit costs 15 (10) 5 (2) (2) 1

Losses from non-core asset sales 12 (5) (7) —

Merger dissolution costs 7 (5) 2 (2) —

Non-officer employee incentive

and other costs 25 (25) —

$ 132 $ (52) $ (44) $ 36 $ (27) $ (8) $ 1

HU M A N A IN C .

MANAGEMENT’S DI SCUSSION AN D A NA LYSIS OF FINANCIAL CONDITION AND RESULTS O F O PERATIONS

Selling, Asset

General and Write-Downs

(In millions) Medical Administrative and Other Total

1998:

T H IR D Q U A R T E R 1 9 9 8 :

Premium deficiency $ 46 $ 46

Provider costs 27 27

Market exit costs $ 15 15

Losses on non-core asset sales 12 12

Merger dissolution costs 7 7

Non-officer employee incentive and other costs $ 25 25

Total third quarter 1998 $ 73 $ 25 $ 34 $ 132

In addition, other expenses of $10 million were recorded

during the fourth quarter related to a claim payment

dispute with a contracted provider and government audits.

Activity related to the 1999 expenses follows: