Humana 1999 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 1999 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

|

|

assets approximated 7.7 percent and 7.5 percent for the

years ended December 31, 1998 and 1997, respectively. Tax

equivalent yield is the rate earned on invested assets,

excluding unrealized gains and losses, adjusted for the

benefit of nontaxable investment income. The weighted

average investment life increased to 2.7 years at December

31, 1998, from 2.6 years at December 31, 1997. Interest

expense increased $27 million during 1998 from funding

the PCAand ChoiceCare acquisitions with

additional borrowings.

B U S IN E S S S E G M E NT I N F OR MAT I O N FO R T H E Y E A RS

EN D E D D EC EM BER 31 , 19 98 AND 1997

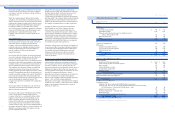

The following table presents segment medical membership

and activity for 1998 and 1997:

31

Administration in Puerto Rico in the second quarter of

1999. TRICARE premium revenues increased 8.3 percent to

$866 million in 1999, from $800 million in 1998, resulting

from an annual contract rate increase and additional

premiums recorded related to TRICARE’s risk-sharing

arrangement with the government.

The Health Plan segment’s adjusted medical expense ratio

for 1999 was 86.4 percent, increasing from 84.4 percent in

1998. The increase was the result of large group commercial

and Medicare HMO medical costs exceeding premium

increases. These higher medical cost trends were

attributable to the inability of certain risk-sharing providers

to effectively manage medical costs within their contractual

arrangements, higher pharmacy utilization and generally

higher medical cost trends across the industry. The

Company expects to realize improvements in its medical

cost trends in 2000 resulting from implementation of the

three-tier pharmacy benefit designs, improvements in risk-

sharing arrangements, the exit of unprofitable Medicare

HMO counties and the sale of its Medicare supplement and

North Florida Medicaid businesses.

The adjusted administrative expense ratio improved 50

basis points from 1998 to 12.1 percent, the result of the

continued rationalization of staffing levels commensurate

with membership levels.

Small Group

The Small Group segment’s adjusted loss before income

taxes was $3 million for 1999 compared to adjusted income

before income taxes of $31 million for 1998. The decline in

profitability is attributable to higher medical costs which

were not adequately anticipated by the Company when it

established premium rates for 1999. To mitigate the effect

of higher medical costs, the Small Group segment’s

improvement initiatives include significant premium rate

increases, improving claim payment processes, provider

re-contracting, rationalizing markets and products and

implementing three-tier pharmacy benefit designs.

The Small Group segment’s premium revenues increased

9.4 percent for 1999 to $3.1 billion from $2.9 billion for 1998.

This premium increase was the result of increased premium

yields, offset by a reduction of 38,700 members from the

sale of the individual line of business in Florida.

The Small Group segment’s adjusted medical expense ratio

for 1999 was 81.2 percent, increasing from 79.7 percent for

1998. The medical expense ratio increase was the result of

medical costs exceeding premium yields. These higher

medical cost trends were the result of the rapid growth of

the Company’s more costly open access products, higher

pharmacy utilization and the greater than expected impact

of the Health Insurance Portability and Accountability Act

or HIPAAand its guarantee issue requirements.

The adjusted administrative expense ratio improved during

1999 to 20.1 percent from 20.3 percent for 1998.

Y E A R S E N DE D D EC EMB ER 31, 199 8 AND 19 97

Adjusted income before income taxes totaled $335 million

for the year ended December 31, 1998, compared to $270

million for the year ended December 31, 1997. Adjusted net

income was $213 million or $1.27 per diluted share in 1998,

compared to $173 million or $1.05 per diluted share in

1997. The earnings increase was a result of the full year

contribution from the 1997 PCAand ChoiceCare

acquisitions, higher commercial premium yields, provider

risk-sharing initiatives, improved claims payment accuracy

across various product lines, and increased interest and

other income. These favorable items were partially offset by

higher interest expense and increased pharmacy costs.

The Company’s 1998 premium revenues increased 21.8

percent to $9.6 billion, from $7.9 billion for the year ended

December 31, 1997. This increase was attributable to the

current year effect of 1997 acquisitions, commercial and

Medicare HMO same-plan membership growth and

increased premium rates for the Company’s commercial

products. PCAand ChoiceCare premium revenues

contributed approximately $1.6 billion, a $1.1 billion

increase over 1997. Same-plan membership growth

contributed $120 million and commercial premium rate

increases added approximately $186 million, as same-plan

commercial premium yields increased 4.8 percent. Changes

in Medicare HMO premium yield had little effect on

premium revenues as same-plan yields declined 0.4 percent

in 1998. The Medicare 2 percent statutory rate increase for

1998 was offset by membership growth in geographic areas

with lower reimbursement rates.

During 1998, the Company’s adjusted medical expense ratio

increased to 83.0 percent from 82.8 percent for the year

ended December 31, 1997. The year to year increase was the

result of the higher medical expense ratio of acquired plans

being included for a full year during 1998. The same-plan

medical expense ratio improved 20 basis points to 82.2

percent from 82.4 percent in 1997, the result of the afore-

mentioned premium rate increases, provider risk-sharing

initiatives and improved claim payment accuracy. These

improvements were partially offset by increased year-over-

year pharmacy costs of 16 percent and 9 percent for the

Company’s commercial and Medicare HMO products,

respectively.

The Company’s adjusted administrative expense ratio was

14.9 percent and 15.5 percent for the years ended December

31, 1998 and 1997, respectively. This improvement was the

result of efforts to streamline the organization, as well as

realized cost savings from the Company’s 1997 acquisitions.

Interest income totaled $150 million for the year ended

December 31, 1998, compared to $131 million for the year

ended December 31, 1997. The increase was attributable to

the full year impact of including PCA’s and ChoiceCare’s

investment portfolios, as well as increased realized

investment gains. The tax equivalent yield on invested

30

HU M A N A IN C .

MANAGEMENT’S DI SCUSSION AN D A NA LYSIS OF FINANCIAL CONDITION AND RESULTS O F O PERATIONS

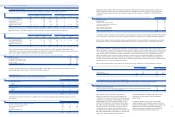

1998 1997

(In thousands) Health Plan Small Group Total Health Plan Small Group Total

Beginning medical membership 4,610 1,597 6,207 3,526 1,325 4,851

Sales 610 571 1,181 499 458 957

Cancellations (700) (466) (1,166) (465) (392) (857)

Acquisitions 1,188 206 1,394

Dispositions (147) (147)

TRICARE change (26) (26) 9 9

Ending medical membership 4,494 1,702 6,196 4,610 1,597 6,207

Ending specialty membership 444 2,189 2,633 507 1,934 2,441

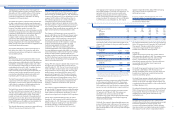

The following table presents certain financial data for the

Company’s two segments for the years ended December 31,

1998 and 1997:

(In millions) 1998 (a) 1997

Premium revenues:

Health Plan $ 6,734 $ 5,487

Small Group 2,863 2,393

$ 9,597 $ 7,880

Adjusted income before income taxes:

Health Plan $ 304 $ 244

Small Group 31 26

$ 335 $ 270

Adjusted medical expense ratios:

Health Plan 84.4% 84.3%

Small Group 79.7% 79.4%

83.0% 82.8%

Adjusted administrative expense ratios:

Health Plan 12.6% 13.1%

Small Group 20.3% 21.0%

14.9% 15.5%

(a) Excludes the previously discussed medical exp enses of $73 million ($60 million Health

(a) Plan and $13 million Small Group), administra tive exp enses of $25 million ($13 million

(a) Health Plan and $12 million Small Group) and asset write-downs and other expenses of

(a) $34 million ($23 million Health Pl an and $ 11 million Sm all G ro u p ) .

Health Plan

Adjusted income before income taxes totaled $304 million

in 1998 compared to $244 million in 1997. The earnings

increase is attributable to the full year contribution from

1997 acquisitions of PCAand ChoiceCare, improved claim

payment accuracy and administrative expense reductions.

The Health Plan segment’s premium revenues increased

22.7 percent to $6.7 billion in 1998. This increase was

attributable to the current year effect of the 1997

acquisitions, large group commercial and Medicare HMO

same-plan membership growth and higher large group

commercial premium yields.

The Health Plan segment’s adjusted medical expense ratio

increased 10 basis points to 84.4 percent. The increase was

the result of the higher medical expense ratio of acquired

plans being included for a full year during 1998 and higher

pharmacy costs.

The adjusted administrative expense ratio improved during

1998 to 12.6 percent from 13.1 percent in 1997 in the Health

Plan segment. This improvement reflects realized cost

savings from integrating the PCAand ChoiceCare

acquisitions into Humana’s operating model.

Small Group

Adjusted income before income taxes was $31 million in

1998 compared to $26 million in 1997. The earnings increase

is primarily attributable to improved claims payment

accuracy, increased interest and other income and

administrative expense reductions. These favorable items

were partially offset by higher interest expense and

increased pharmacy costs.

The Small Group segment’s premium revenues increased

19.6 percent to $2.9 billion in 1998. This increase was

primarily attributable to the current year effect of the 1997

acquisitions and small group commercial and specialty

same-plan membership growth.

The Small Group segment’s adjusted medical expense ratio

increased 30 basis points to 79.7 percent. The year to year

increase was the result of the higher medical expense ratio

of acquired plans being included for a full year during 1998

and higher pharmacy costs.

The adjusted administrative expense ratio improved during

1998 to 20.3 percent from 21.0 percent in 1997 in the Small

Group segment. This improvement reflects the continued

rationalization of staffing levels commensurate with

membership levels.

L I Q U I D I T Y

Operating cash flows improved to $217 million in 1999

from $55 million in 1998, due to increased premium receipts

and reduced payments for accrued expenses, taxes,

severance and professional liabilities. Partially offsetting

these improvements were higher claim payments related to

the Company’s run-off workers’ compensation business.