Humana 1999 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 1999 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

|

|

Changes in equity valuations (based upon the Standard &

Poor’s 500 stock index) over the past ten years which were in

excess of 30 percent occurred four times, between 20 percent

and 30 percent occurred three times and between 10 percent

and 20 percent also occurred three times.

C A P I TAL R E S O U R C ES

The Company’s ongoing capital expenditures relate

primarily to information systems and administrative

facilities necessary for activities such as claims processing,

billing and collections, medical utilization review and

customer service. Total capital expenditures, excluding

acquisitions, were $89 million, $104 million and $73 million

for the years ended December 31, 1999, 1998 and 1997,

respectively. Capital expenditures during 1998 included the

$32 million purchase and renovation of a regional customer

service center in Jacksonville, Florida.

Excluding acquisitions, planned capital spending in 2000

will approximate $130 million to $140 million for the

funding of the Company’s technology initiatives and

expansion and improvement of its administrative facilities.

E F F E C TS O F I N F LATI ON A ND CH A NG IN G P R I C E S

The Company’s operations are regulated by various state

and federal government agencies. Actuarially determined

premium rate increases for commercial products are

generally approved by the respective state insurance

commissioners, while increases in premiums for Medicaid

and Medicare HMO products are established by various

state governments and the Health Care Financing

Administration. Premium rates under the TRICARE

contract with the United States Department of Defense may

be adjusted on a year by year basis to reflect inflation,

changes in the workload volumes of military medical

facilities and contract modifications.

The Company’s 2000 average rate of statutory increase

under the Medicare HMO contracts is approximately two

percent. Over the last five years, annual increases have

ranged from as low as the January 1999 increase of two

percent to as high as nine percent in January 1996, with an

average of approximately five percent. The Company’s

Medicare HMO contracts with the federal government are

renewed for a one-year term each December 31 unless

terminated 90 days prior thereto.

Legislative proposals are being considered which may

revise the Medicare program’s current support of the use of

managed health care for Medicare beneficiaries and the

future reimbursement rates thereunder. Management is

unable to predict the outcome of these proposals or the

impact they may have on the Company’s financial position,

results of operations or cash flows. The Company’s

Medicaid contracts are generally annual contracts with

various states except for the two-year contract with the

Health Insurance Administration in Puerto Rico.

Additionally, the Company’s TRICARE contract is a one-

year contract renewable on July 1, 2000, for one additional

year. The loss of these contracts or significant changes in

these programs as a result of legislative action, including

reductions in payments or increases in benefits without

corresponding increases in payments, would have a

material adverse effect on the revenues, profitability and

business prospects of the Company.

In addition, the Company continually contracts and seeks

to renew contracts with providers at rates designed to

ensure adequate profitability. To the extent the Company is

unable to obtain such rates, its financial position, results of

operations and cash flows could be adversely impacted.

TH E C O M PAN Y’ S YE AR 20 0 0 D I S C L OS U R E S TAT E M E N T

The Company commenced its assessment of Year 2000

exposures in early 1996. In December 1998, the Company

was 100 percent complete with the remediation of its core

business systems and by December 1999 had remediated

100 percent of its business application systems. As of

December 31, 1999, the Company had completed all Year

2000 initiatives.

To date, the Company has experienced no outages or

problems related to the Year 2000 date rollover. All business

systems are functioning normally and the Company has not

experienced any disruptions in service with third party

organizations with which it interacts related to the

century change.

The Company’s application systems are largely developed

and maintained in-house by a staff of 400 application

programmers who are versed in the utilization of state-of-

the-art technology. All application systems are fully

integrated and automatically pass data through various

system processes. The Company’s primary data center and

the majority of its programming and support staff are

located at the Company’s corporate offices in Louisville,

Kentucky. In order to create the necessary internal focus

surrounding the Year 2000 issue, the Company established

a centralized Year 2000 Program Management Office

(“PMO”) which is charged with overall coordination of

enterprise wide Year 2000 initiatives and regular progress

reporting to the Company’s senior management.

The Year 2000 project is currently estimated to have a

minimum total cost of approximately $30 million of which

approximately $10 million was spent during 1999. Year 2000

expenses represented less than ten percent of the

Information Systems budget during 1999. Year 2000 costs

are expensed as incurred and funded with cash flows from

operations. The Company does not expect to incur

significant Year 2000 project costs in the year 2000.

The extent and magnitude of the Year 2000 project, as it will

affect the Company for some period after January 1, 2000, is

difficult to predict or quantify. In order to mitigate these

risks, the Company developed business continuity and

contingency plans which were finalized in the second

quarter of 1999. These plans would be enacted if Year 2000

problems were to occur within the Company, or if third

party constituents have failures due to the millennium

change. Contingency plans were developed for six major

functional areas encompassing 22 operational subdivisions

33

Cash provided by investing activities was $18 million

in 1999, compared to $28 million in 1998. These amounts

reflect the net effect of investment and capital

expenditure transactions.

Cash used in financing activities totaled $170 million in

1999 compared to cash provided by financing activities of

$51 million in 1998. This decrease primarily resulted from

1999 debt repayments and changes in book overdrafts.

The Company’s subsidiaries operate in states that require

minimum levels of equity and regulate the payment of

dividends to the parent company. As a result, the

Company’s ability to use operating subsidiaries’ cash flows

is restricted to the extent of the subsidiaries’ ability to

obtain regulatory approval to pay dividends.

The National Association of Insurance Commissioners has

recommended that states adopt a risk-based capital (“RBC”)

formula for companies established as HMO entities, similar

to the current requirement for insurance companies. The

RBC provisions may require new minimum capital and

surplus levels for some of the Company’s HMO sub-

sidiaries. Many states have not yet determined when they

will adopt the RBC formula or if they will allow a phase-in

to the required levels of capital and surplus.

The Company currently maintains approximately $768

million of capital and surplus in its health insurance and

HMO entities, compared to the minimum statutory

required capital and surplus levels of approximately $569

million. If the states in which the Company conducts

business adopt the proposed RBC formula, without a

phase-in provision, the Company estimates it would be

required to fund additional capital into its various

subsidiaries of approximately $45 million. After this capital

infusion, the Company would have $138 million of capital

and surplus above the required RBC level.

The Company maintains a revolving credit agreement

(“Credit Agreement”) which provides a line of credit of up

to $1.0 billion and expires in August 2002. Principal

amounts outstanding under the Credit Agreement bear

interest at either a fixed rate or a floating rate, ranging from

LIBOR plus 35 basis points to LIBOR plus 80 basis points,

depending on the Company’s credit ratings. The Credit

Agreement, which was amended in 1999 to reduce the line

of credit by $500 million from $1.5 billion and modify

certain covenants, contains customary covenants and events

of default including, but not limited to, financial tests for

interest coverage and leverage. The Company is in

compliance with all covenants. The Company also

maintains and issues short-term debt securities under a

commercial paper program.

Management believes that funds from planned divestitures,

future operating cash flows and funds available under the

existing Credit Agreement and commercial paper program

are sufficient to meet future liquidity needs. Management

also believes the aforementioned sources of funds are

adequate to allow the Company to pursue selected

acquisition and expansion opportunities, as well as to fund

capital requirements.

RI S K - S EN S I T I V E F IN A NC I A L IN S T R U M E N TS A ND PO SI T IO NS

The Company’s risk of fluctuation in earnings due to

changes in interest income from its fixed income portfolio is

partially mitigated by the Company’s debt position, as well

as the short duration of the fixed income portfolio.

The Company has evaluated the interest income and debt

expense impact resulting from a hypothetical change in

interest rates of 100, 200 and 300 basis points over the next

twelve-month period, as reflected in the following table. In

the past ten years, annual changes in commercial paper

rates have never exceeded 300 basis points, changed

between 200 and 300 basis points twice and changed

between 100 and 200 basis points once. The modeling

technique used to calculate the pro forma net change

considered the cash flows related to fixed income

investments and debt, which are subject to interest rate

changes during a prospective twelve-month period.

32

HU M A N A IN C .

MANAGEMENT’S DI SCUSSION AN D A NA LYSIS OF FINANCIAL CONDITION A ND RESULTS OF OPERATI ONS

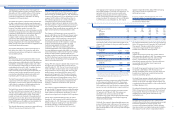

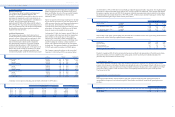

Increase (decrease) in earnings given an interest rate Increase (decrease) in earnings given an interest rate

(In millions) decrease of X basis points increase of X basis points

(300) (200) (100) 100 200 300

1999

Fixed income portfolio $ (10.1) $ (6.7) $ (3.4) $ 3.4 $ 6.8 $ 10.2

Debt 9.1 6.1 3.0 (3.0) (6.1) (9.1)

Total $ (1.0) $ (0.6) $ (0.4) $ 0.4 $ 0.7 $ 1.1

1998

Fixed income portfolio $ (11.9) $ (7.9) $ (4.0) $ 4.0 $ 8.0 $ 12.0

Debt 5.7 3.8 1.9 (1.9) (3.8) (5.7)

Total $ (6.2) $ (4.1) $ (2.1) $ 2.1 $ 4.2 $ 6.3

The following table presents the hypothetical change in fair market values of common equity securities held by the Company

at December 31, 1999 and 1998, which are sensitive to changes in stock market values. These common equity securities are held

for purposes other than trading.

Decrease in valuation of securities Increase in valuation of securities

given an X% decrease in Fair Value at given an X% increase in

(In millions) each equity security’s value December 31, each equity security’s value

(30%) (20%) (10%) 10% 20% 30%

1999

Common equity securities $ (5.6) $ (3.7) $ (1.9) $ 18.6 $ 1.9 $ 3.7 $ 5.6

1998

Common equity securities $ (18.6) $ (12.4) $ (6.2) $ 62.1 $ 6.2 $ 12.4 $ 18.6