Humana 1999 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 1999 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

|

|

file closings, the Company reduced these liabilities by $36

million ($23 million after tax, or $0.14 per diluted share)

and $5 million ($3 million after tax, or $0.02 per diluted

share) in 1999 and 1998, respectively.

The adjusted administrative expense ratio improved

during 1999 to 14.6 percent from 14.9 percent in 1998. The

year-over-year improvement in the administrative expense

ratio reflects continued rationalization of staffing levels

commensurate with membership levels. The administrative

expense ratio is expected to increase slightly in 2000 from

increased spending on information technology.

Interest income totaled $132 million for 1999 and $150

million for 1998. This decrease resulted from a decrease in

realized investment gains, lower average invested balances

and lower investment yields. The tax equivalent yield on

invested assets approximated 7.1 percent for 1999 and 7.7

percent for 1998. Tax equivalent yield is the rate earned on

invested assets, excluding unrealized gains and losses,

adjusted for the benefit of nontaxable investment income.

The weighted average investment life was 2.7 years at both

December 31, 1999 and 1998. Other income declined $12

million during 1999, due to the reduction of income from

ancillary businesses the Company sold in 1998 and a lower

contribution from the Company’s ASO business, partially

offset by a $12 million gain from the sale of a tangible asset

in 1999. Interest expense declined $14 million during 1999

as a result of lower average outstanding borrowings.

BUS I N E S S S E G M E N T I N F O RM AT I ON FO R T H E Y EA RS

EN D E D D EC EM BER 31 , 19 99 AND 1998

The following table presents segment medical membership

and activity for 1999 and 1998:

Y E A RS E N D E D DE C EMB ER 31, 199 9 AN D 19 98

Adjusted income before income taxes totaled $181 million

for the year ended December 31, 1999, compared to $335

million for the year ended December 31, 1998. Adjusted net

income was $117 million or $0.69 per diluted share in 1999,

compared to $213 million or $1.27 per diluted share in 1998.

The earnings decline was attributable to higher medical cost

trends which were not adequately anticipated by the

Company when it established premium rates for 1999.

These higher medical cost trends primarily resulted from

the introduction and rapid growth of an open access

product, ineffective risk-sharing arrangements, significant

increases in pharmacy costs and the unfavorable

negotiations of the Florida Columbia/HCAprovider

contract. During 1999, the Company implemented

initiatives to mitigate the effect of these issues. The

initiatives include pricing products commensurate with the

higher medical costs, rationalizing markets and products,

rehabilitating the large group commercial business,

re-contracting with providers and cost management

improvements focused mainly on medical and claims cost

management disciplines. These initiatives began to improve

operating results in the second half of 1999 but in large

part will be realized in January 2000 when the majority of

the Company’s large group commercial customers renew

and when the Company’s Medicare product offerings

were adjusted.

The Company’s premium revenues increased 3.8 percent to

a record $10.0 billion for 1999, compared to $9.6 billion for

1998. Higher premium revenues resulted from increased

premium yields of 7.4 percent and 3.4 percent for the

Company’s commercial and Medicare HMO products,

respectively. This increase was partially offset by a decline

in commercial membership of 177,900, due to selling the

Florida individual business line and the result of substantial

premium increases delivered to large group and small

group commercial customers. Membership levels are

expected to decline in 2000 due to the sale of certain non-

core businesses and substantial premium rate increases.

The Company expects commercial and Medicare HMO

premium yields to approximate 10 to 12 percent and 6 to 7

percent, respectively, in 2000, the result of commercial

premium rate increases and newly introduced Medicare

member premiums.

The Company’s adjusted medical expense ratio for 1999

was 84.8 percent, compared to 83.0 percent for 1998. The

increase was the result of medical cost increases in the

Company’s commercial products exceeding premium

rate increases. Offsetting the impact of the increasing

commercial medical costs was the continued favorable

claim liability development in the Company’s run-off

workers’ compensation business acquired in connection

with its acquisition of PCA. After evaluating the workers’

compensation claim liabilities against claim payments and

29

C O M PARIS O N O F R E S U LT S O F O P E RAT I O N S

In order to enhance comparability as well as to provide a

baseline against which historical and prospective periods

can be measured, the following discussion comparing

results for the years ended December 31, 1999, 1998 and

1997, excludes the previously described expenses, but does

include the beneficial effect related to premium deficiency

on operating results for the periods shown. There were no

adjustments to results for 1997. The following table

reconciles the results reported in the Consolidated

Statements of Operations (“Reported Results”) to the results

contained in the following discussion (“Adjusted Results”)

for 1999 and 1998:

28

HU M A N A IN C .

MANAGEMENT’S DI SCUSSION AN D A NA LYSIS OF FINANCIAL CONDITION AND RESULTS O F O PERATIONS

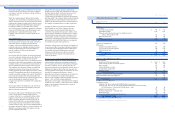

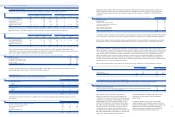

Reported Results Excluded Expenses Adjusted Results

(In millions, except per share results) 1999 1998 1999 (a) 1998 (b) 1999 1998

Consolidated Statements of Operations caption items that are adjusted:

Operating expenses:

Medical $ 8,532 $ 8,041 $ (90) $ (73) $ 8,442 $ 7,968

Selling, general and administrative 1,368 1,328 (35) (25) 1,333 1,303

Depreciation and amortization 124 128 124 128

Asset write-downs and other expenses 460 34 (460) (34) — —

Total operating expenses 10,484 9,531 (585) (132) 9,899 9,399

(Loss) income from operations (371) 250 585 132 214 382

(Loss) income before income taxes (404) 203 585 132 181 335

Net (loss) income $ (382) $ 129 $ 499 $ 84 $ 117 $ 213

(Loss) earnings per common share $ (2.28) $ 0.77 $ 2.97 $ 0.50 $ 0.69 $ 1.28

Diluted (loss) earnings per common share $ (2.28) $ 0.77 $ 2.97 $ 0.50 $ 0.69 $ 1.27

Reported Ratios Ratio Effect of Excluded Expenses Adjusted Ratios

1999 1998 1999 (a) 1998 (b) 1999 1998

Medical expense ratios:

Health Plan 87.4% 85.3% (1.0)% (0.9)% 86.4% 84.4%

Small Group 81.9% 80.2% (0.7)% (0.5)% 81.2% 79.7%

Total 85.7% 83.8% (0.9)% (0.8)% 84.8% 83.0%

Administrative expense ratios:

Health Plan 12.5% 12.8% (0.4)% (0.2)% 12.1% 12.6%

Small Group 20.4% 20.7% (0.3)% (0.4)% 20.1% 20.3%

Total 15.0% 15.2% (0.4)% (0.3)% 14.6% 14.9%

(a) Reflects the previously discussed m edical, ad mi nistrative, asse t write-downs and other expenses of $90 million, $35 million and $ 460 million, re s p e c t i v e l y.

(b) Reflects the previously discussed m edical, ad mi ni strative, asset write-downs and other expenses of $73 million, $2 5 million and $ 34 mi ll ion, re s p e c t i v e l y.

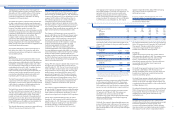

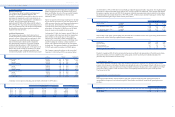

1999 1998

(In thousands) Health Plan Small Group Total Health Plan Small Group Total

Beginning medical membership 4,494 1,702 6,196 4,610 1,597 6,207

Sales 588 436 1,024 610 571 1,181

Cancellations (778) (475) (1,253) (700) (466) (1,166)

TRICARE change (28) (28) (26) (26)

Ending medical membership 4,276 1,663 5,939 4,494 1,702 6,196

Ending specialty membership 477 2,484 2,961 444 2,189 2,633

The following table presents certain financial data for the

Company’s two segments for the years ended December 31,

1999 and 1998:

(In millions) 1999 (a) 1998 (b)

Premium revenues:

Health Plan $ 6,827 $ 6,734

Small Group 3,132 2,863

$ 9,959 $ 9,597

Adjusted income (loss) before income taxes:

Health Plan $ 184 $ 304

Small Group (3) 31

$ 181 $ 335

Adjusted medical expense ratios:

Health Plan 86.4% 84.4%

Small Group 81.2% 79.7%

84.8% 83.0%

Adjusted administrative expense ratios:

Health Plan 12.1% 12.6%

Small Group 20.1% 20.3%

14.6% 14.9%

(a) Excludes the previously discussed medical expenses of $9 0 mill ion ($66 million Health

(a) Plan and $24 million Small Group), administra tive expenses of $35 million ($27 million

(a) Health Plan and $8 million Small G ro up) and asset writ e-downs and other expenses of

(a) $460 million ($460 million Health Pla n).

(b) Excludes the previously discussed medica l exp enses of $73 million ($60 million Health

(a) Plan and $13 million Small Group), adm inistra tive expe nses of $2 5 mil lion ($13 million

(a) Health Plan and $12 million Small Group) and asset w rite-downs and other expenses of

(a) $34 million ($23 million Health Pl an and $ 11 million Sm all G ro u p ) .

Health Plan

Adjusted income before income taxes totaled $184 million

for 1999 compared to $304 million for 1998. The earnings

decline was attributable to higher medical cost trends

which were not adequately anticipated by the Company

when it established premium rates for 1999. These higher

medical cost trends primarily resulted from ineffective risk-

sharing arrangements, pharmacy cost increases and the

result of unfavorable negotiations of the Florida

Columbia/HCAprovider contract. Initiatives to mitigate

the effect of these issues include significant large group

commercial rate increases, re-contracting with, or

eliminating certain risk-sharing providers, implementing

three-tier pharmacy benefit designs, instituting Medicare

HMO member premium and benefit changes and exiting

various Medicare markets. These initiatives began to

improve operating results in the second half of 1999 but

in large part will be realized in January 2000 when the

majority of the Company’s large group commercial

customers renew and when the Company’s Medicare

product offerings were adjusted.

The Health Plan segment’s premium revenues increased 1.4

percent to $6.8 billion for 1999. Large group commercial

and Medicare HMO premiums remained unchanged at $2.3

billion and $2.9 billion, respectively. Higher premium yields

of 5.5 percent and 3.4 percent for the large group

commercial and Medicare HMO lines, respectively, were

offset by membership reductions. Large group commercial

membership decreased 139,200 from 1998 reflecting the

effects of the Company’s commercial premium pricing

actions intended to maintain profitability. Medicare HMO

membership decreased 13,500 members from the exit of the

Treasure Coast and Sarasota, Florida markets. The Medicare

HMO membership reduction from market exits was

somewhat mitigated by increased membership achieved

through the redirecting of sales and marketing efforts

focused on key Medicare markets like Chicago, Tampa and

South Florida. The Company’s Medicaid premiums

increased 8.8 percent to $603 million for 1999 compared to

$554 million in 1998. This increase resulted from the more

favorable rates obtained from the renewal of the

Company’s contract with the Health Insurance