Humana 1999 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 1999 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30

|

|

Options to purchase 9,427,060, 1,562,949 and 2,414,148

shares for the years ended December 31, 1999, 1998 and

1997, respectively, were not included in the computation of

(loss) earnings per common share-assuming dilution due to

the Company’s loss in 1999 and because the options’

exercise prices were greater than the average market price

of the Company’s common stock in 1998 and 1997.

Reclassifications

Certain reclassifications have been made to the prior years’

consolidated financial statements to conform with the

current year presentation.

Recently Issued Accounting Pronouncements

In June 1998, the Financial Accounting Standards Board

issued Statement of Financial Accounting Standards No.

133, “Accounting for Derivative Instruments and Hedging

Activities” (“SFAS No. 133”). In general, SFAS No. 133

requires that all derivatives be recognized as either assets or

liabilities in the balance sheet at their fair value, and sets

forth the manner in which gains or losses thereon are

to be recorded. The treatment of such gains or losses is

dependent upon the type of exposure, if any, for which the

derivative is designated as a hedge. This standard is

effective for the Company’s financial statements

beginning January 1, 2001, with early adoption permitted.

Management of the Company anticipates that the adoption

of SFAS No. 133 on January 1, 2001 will not have a material

impact on the Company’s financial position, results of

operations or cash flows.

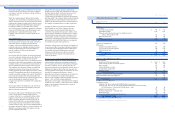

3. A S S E T W RI TE -D O W NS A ND OPER ATIONA L EXPE NSE S

The following table presents the components of the asset

write-downs and operational expenses and their respective

classifications in the 1999 and 1998 Consolidated Statements

of Operations:

41

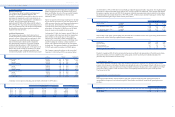

Long-Lived Assets

Property and equipment is carried at cost, and is comprised

of the following at December 31, 1999 and 1998:

(In millions) 1999 1998

Land $ 32 $ 33

Buildings 364 355

Equipment and computer software 432 400

828 788

Accumulated depreciation (410) (355)

$ 418 $ 433

Depreciation is computed using the straight-line method

over estimated useful lives ranging from three to ten years

for equipment, three to five years for computer software

and twenty years for buildings. Depreciation expense was

$79 million, $75 million and $66 million for the years ended

December 31, 1999, 1998 and 1997, respectively.

Cost in excess of net assets acquired, or goodwill,

represents the unamortized excess of cost over the fair

value of net tangible and identifiable intangible assets

acquired. Identifiable intangible assets, which are included

in other long-term assets in the accompanying Consolidated

Balance Sheets, primarily relate to subscriber and provider

contracts. Goodwill and identifiable intangible assets are

amortized on a straight-line method over their estimated

useful lives. Goodwill has been amortized over periods

ranging from six to 40 years and identifiable intangible

assets are being amortized over periods ranging from seven

to 14 years. After a re-evaluation, effective January 1, 2000,

the Company adopted a 20 year amortization period from

the date of acquisition for goodwill previously amortized

over 40 years. Amortization expense was $45 million,

$53 million and $42 million for the years ended December

31, 1999, 1998 and 1997, respectively.

The carrying values of all long-lived assets are periodically

reviewed by management for impairment, based upon

undiscounted market level cash flows, whenever adverse

events or changes in circumstances occur. Losses are

recognized when the carrying value of a long-lived asset

may not be recoverable. See Note 3 for a discussion related

to the Company’s impairment review.

Revenue and Medical Cost Recognition

Premium revenues are recognized as income in the period

members are entitled to receive services. Premiums

received prior to such period are recorded as unearned

premium revenues.

Medical costs include claim payments, capitation payments,

physician salaries, allocations of certain centralized

expenses and various other costs incurred to provide

medical care to members, as well as estimates of future

payments to hospitals and others for medical care provided

prior to the balance sheet date. Capitation payments

represent monthly prepaid fees disbursed to participating

primary care physicians and other providers who are

responsible for providing medical care to members. The

estimates of future medical claim and other expense

payments are developed using actuarial methods and

assumptions based upon payment patterns, medical

inflation, historical development and other relevant factors.

Estimates of future payments relating to services incurred

in the current and prior periods are continually reviewed

by management and adjusted as necessary.

The Company assesses the profitability of its contracts for

providing health care services to its members when current

market operating results or forecasts indicate probable

future losses. The Company records a premium deficiency

in current operations to the extent that the sum of expected

health care costs, claim adjustment expenses and

maintenance costs exceeds related future premiums.

Anticipated investment income is not considered for

purposes of computing the premium deficiency. Because

the majority of the Company’s member contracts renew

annually, the Company does not anticipate premium

deficiencies, except when unanticipated adverse events or

changes in circumstances indicate otherwise. See Note 3 for

a discussion related to premium deficiencies.

Management believes the Company’s medical and other

expenses payable are adequate to cover future claims

payments required, however, such estimates are based on

knowledge of current events and anticipated future events,

and, therefore, the actual liability could differ from

amounts provided.

Book Overdraft

Under the Company’s cash management system, checks

issued but not presented to banks frequently result in

overdraft balances for accounting purposes and are

classified as a current liability in the Consolidated

Balance Sheets.

Stock Options

The Company has adopted the disclosure-only provisions

of Statement of Financial Accounting Standards No. 123,

“Accounting for Stock-Based Compensation” (“SFAS 123”)

and uses Accounting Principles Board Opinion No. 25 and

related interpretations in the accounting for its stock option

plans. No compensation expense has been recognized in

connection with the granting of stock options. See Note 8

for discussion of stock options and the disclosures required

by SFAS 123.

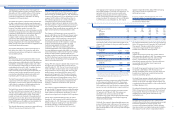

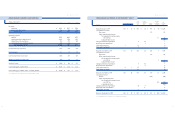

(Loss) Earnings Per Common Share

Detail supporting the computation of (loss) earnings per

common share and (loss) earnings per common share-

assuming dilution follows:

40

HU M A N A IN C .

NOTES TO CONSOLIDATED FINANCIAL STAT E M E N T S

(Dollars in millions, except per share results) Net (Loss) Income Shares Per Share Results

YE A R E N D E D D E C E M B E R 3 1 , 1 9 9 9

Loss per common share $ (382) 167,555,917 $ (2.28)

Effect of dilutive stock options

Loss per common share – assuming dilution $ (382) 167,555,917 $ (2.28)

YE A R E N D E D D E C E M B E R 3 1 , 1 9 9 8

Earnings per common share $ 129 166,471,824 $ 0.77

Effect of dilutive stock options 1,792,756

Earnings per common share – assuming dilution $ 129 168,264,580 $ 0.77

YE A R E N D E D D E C E M B E R 3 1 , 1 9 9 7

Earnings per common share $ 173 163,406,460 $ 1.06

Effect of dilutive stock options 2,436,019 (0.01)

Earnings per common share – assuming dilution $ 173 165,842,479 $ 1.05

Selling, Asset

General and Write-Downs

(In millions) Medical Administrative and Other Total

1999:

FI R S T Q U A R T E R 1 9 9 9 :

Premium deficiency $ 50 $ 50

Reserve strengthening 35 35

Provider costs 5 5

Total first quarter 1999 90 90

F O U R T H Q UA RT ER 1 999 :

Long-lived asset impairment $ 342 342

Losses on non-core asset sales 118 118

Professional liability reserve strengthening and other costs $ 35 35

Total fourth quarter 1999 35 460 495

Total 1999 $ 90 $ 35 $ 460 $ 585

1998:

THIRD QUARTER 1998:

Premium deficiency $ 46 $ 46

Provider costs 27 27

Market exit costs $ 15 15

Losses on non-core asset sales 12 12

Merger dissolution costs 7 7

Non-officer employee incentive and other costs $ 25 25

Total third quarter 1998 $ 73 $ 25 $ 34 $ 132