Kohl's 2010 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2010 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Table of Contents

Total net sales for 2010 were $18.4 billion, a 7.1% increase over 2009. Comparable store sales increased 4.4% over 2009. The Southeast region and the

Footwear business reported the strongest comparable store sales growth.

Gross margin as a percent of net sales for the year increased approximately 40 basis points over the 2009 rate to 38.2%. Strong inventory management as

well as increased penetration of private and exclusive brands contributed to the margin strength.

Selling, general and administrative expenses (“SG&A”) increased 6% compared to the prior year. SG&A as a percentage of net sales, decreased, or

“leveraged” primarily driven by store payroll, advertising, and preopening costs.

Net income increased 12% for 2010 to $1.1 billion, or $3.65 per diluted share, compared to $991 million, or $3.23 per diluted share for 2009.

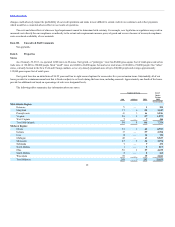

We ended the year with 1,089 stores in 49 states, including 31 which were successfully opened in 2010. We expect to open approximately 40 stores in

fiscal 2011. Remodels remain a critical part of our long-term strategy as we believe it is important to maintain our existing store base. We completed 85

remodels in 2010, compared to 51 in 2009, and expect to remodel approximately 100 stores in 2011.

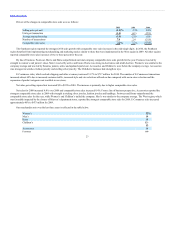

In February 2011, our Board of Directors approved our first ever dividend. The 25 cent per share quarterly dividend will be paid on March 30, 2011 to

all shareholders of record as of March 9, 2011. The dividend reflects the Board’s confidence in our long-term cash flow. We expect to use a portion of future

free cash flow to continue to pay quarterly dividends. Our Board of Directors also increased the remaining share repurchase authorization under our existing

share repurchase program by $2.6 billion, from $900 million to $3.5 billion. We expect to execute the share repurchase program primarily in open market

transactions, subject to market conditions and to complete the program by the end of Fiscal 2013.

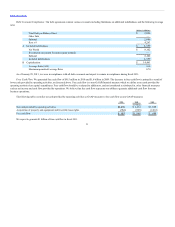

On November 17, 2010, we entered into an accelerated share repurchase transaction with Morgan Stanley & Co. Incorporated (“Morgan Stanley”) to

repurchase $1.0 billion of Kohl’s common stock on an accelerated basis. This accelerated share repurchase was part of the $2.5 billion share repurchase

program authorized by our Board of Directors in September 2007. On November 18, 2010, we paid $1.0 billion to Morgan Stanley from cash on hand. We

received a total of 18.8 million shares under the program: 12.6 million shares on November 18, 2010, 3.8 million shares on December 7, 2010, 1.5 million on

January 11, 2011, and a final delivery of 0.9 million shares on March 3, 2011.

We installed electronic signs in approximately 100 stores in 2010. We expect to have installed the signs in all stores by Holiday 2012. In-store kiosks

were effectively rolled-out to all stores in August 2010. The kiosks allow customers to order items which are not available in the store and have them delivered

to their home with no shipping costs. Preliminary results from the kiosks have exceeded our plans and we expect to add an additional kiosk in approximately

100 stores in 2011.

We believe that consumers will remain focused on value in 2011. We intend to continue to be flexible in our sales and inventory planning and in our

expense management in order to react to changes in consumer demand. Additionally, merchandise costs in all apparel categories are expected to be up

approximately 10% to 15% overall for Fall 2011 due to inflation in the cost of raw materials, labor and fuel. Specific increases are dependent on the category

and the related fabric content. We have been preparing for these cost increases for some time and are working diligently to minimize the impact of these higher

costs on a consumer that is still buying cautiously and, therefore, less open to paying higher prices for discretionary goods.

21