Kohl's 2010 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2010 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Table of Contents

Stock-based compensation expense, including stock options and nonvested stock awards, is recognized on a straight-line basis over the vesting period

based on the fair value of awards which are expected to vest. The fair value of all share-based awards is estimated on the date of grant.

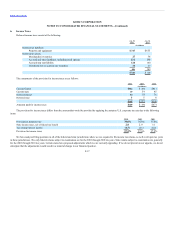

As of January 29, 2011, the par value of our long-term investments was $338 million and the estimated fair value was $277 million. Our auction rate

securities (“ARS”) portfolio consists entirely of highly-rated, insured student loan backed securities. Substantially all of the principal and interest is insured

by the federal government and the remainder is insured by highly-rated insurance companies. Approximately $145 million of our ARS (at fair value) are rated

“AAA” by Moody’s, Standard & Poor’s and/or Fitch Ratings.

Beginning in February 2008, liquidity issues in the global credit markets resulted in the failure of auctions for all of our ARS. A “failed” auction occurs

when the amount of securities submitted for sale in the auction exceeds the amount of purchase bids. As a result, holders are unable to liquidate their

investment through the auction. A failed auction is not a default of the debt instrument, but does set a new interest rate in accordance with the terms of the debt

instrument. A failed auction limits liquidity for holders until there is a successful auction or until such time as another market for ARS develops. ARS are

generally callable by the issuer at any time. Scheduled auctions continue to be held until the ARS matures or is called.

To date, we have collected all interest payable on outstanding ARS when due and expect to continue to do so in the future. At this time, we have no reason

to believe that any of the underlying issuers of our ARS or their insurers are presently at risk or that the reduced liquidity has had a significant impact on the

underlying credit quality of the assets backing our ARS. While the auction failures limit our ability to liquidate these investments, we do not believe these

failures will have any significant impact on our ability to fund ongoing operations and growth initiatives.

We intend to hold these ARS until maturity or until we can liquidate them at par value. Based on our other sources of liquidity, we do not believe we will

be required to sell them before recovery of par value. Therefore, impairment charges are considered temporary and have been included in Accumulated Other

Comprehensive Loss within our Consolidated Balance Sheet. In certain cases, holding the investments until recovery may mean until maturity, which ranges

from 2015 to 2056. The weighted-average maturity date is 2035. As a result of the persistent failed auctions and the uncertainty of when these investments

could be successfully liquidated at par, we have recorded all of our ARS as Long-term Investments within the Consolidated Balance Sheet.

ASC No. 820, “Fair Value Measurements and Disclosures,” requires fair value measurements be classified and disclosed in one of the following three

categories:

Level 1: Financial instruments with unadjusted, quoted prices listed on active market exchanges.

Level 2:

Financial instruments lacking unadjusted, quoted prices from active market exchanges, including over-the-counter traded

financial instruments. The prices for the financial instruments are determined using prices for recently traded financial

instruments with similar underlying terms as well as directly or indirectly observable inputs, such as interest rates and yield

curves that are observable at commonly quoted intervals.

Level 3:

Financial instruments that are not actively traded on a market exchange. This category includes situations where there is little, if

any, market activity for the financial instrument. The prices are determined using significant unobservable inputs or valuation

techniques.

F-13