Kohl's 2010 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2010 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Table of Contents

.

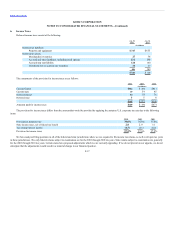

We have various facilities upon which we may draw funds, including a $900 million senior unsecured revolving facility and two demand notes with

aggregate availability of $50 million. Depending on the type of advance under these facilities, amounts borrowed bear interest at competitive bid rates; LIBOR

plus a margin, depending on our long-term unsecured debt ratings; or the agent bank’s base rate. The $900 million revolving facility expires in October 2011.

The co-leads of this facility, The Bank of New York Mellon and Bank of America, have each committed $100 million. The remaining 12 lenders have each

committed between $30 and $130 million. There were no draws on these facilities during 2010 or 2009. Prior to or upon termination of these facilities, we plan

to renew or replace them with similar arrangements.

Our debt agreements contain various covenants including limitations on additional indebtedness and certain financial tests. As of January 29, 2011, we

were in compliance with all covenants of the debt agreements.

We also have outstanding trade letters of credit and stand-by letters of credit totaling approximately $78 million at January 29, 2011, issued under

uncommitted lines with two banks.

In December 2010, we entered into a $200 million forward starting interest rate swap. We entered into this derivative financial instrument to reduce risk

associated with movements in interest rates on debt which we expect to issue in the second half of fiscal 2011. This derivative financial instrument qualifies as

a cash flow hedge. Accordingly, the effective portion of the instrument’s gains or losses is reported as a component of other comprehensive income and will be

reclassified into earnings when the interest payments on the forecasted debt transaction affect earnings. Amounts related to this financial instrument were not

material in 2010.

Interest payments, net of amounts capitalized, were $140 million for 2010, $133 million for 2009 and $145 million for 2008.

.

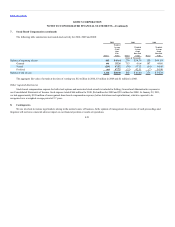

We lease certain property and equipment. Rent expense is recognized on a straight-line basis over the expected lease term. The lease term begins on the

date we become legally obligated for the rent payments or we take possession of the building or land, whichever is earlier. The lease term includes cancelable

option periods where failure to exercise such options would result in an economic penalty. Failure to exercise such options would result in the recognition of

accelerated depreciation expense of the related assets.

Rent expense charged to operations was $533 million for 2010, $498 million for 2009 and $448 million for 2008. Rent expense includes contingent

rents, which are based on sales, of $3 million for 2010, $2 million for 2009 and $3 million for 2008. In addition, we are often required to pay real estate taxes,

insurance and maintenance costs. These items are not included in the rent expenses listed above. Many store leases include multiple renewal options,

exercisable at our option, that generally range from four to eight additional five-year periods.

F-15