Kohl's 2010 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2010 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Table of Contents

includes a neighborhood location close to home, convenient parking, easily accessible entry, knowledgeable and friendly associates, wide aisles, a

functional store layout, shopping carts/strollers and fast, centralized checkouts. Though our stores have fewer departments than traditional, full-

line department stores, the physical layout of the store and our focus on strong in-stock positions in style, color and size is aimed at providing a

convenient shopping experience for an increasingly time-starved customer.

Remodels are also an important part of our in-store shopping experience initiatives as we believe it is extremely important to maintain our existing

store base. We completed 85 store remodels in 2010—an increase from the 51 stores which were remodeled in 2009 — and currently plan to

remodel approximately 100 stores in 2011. We have effectively compressed the remodel duration period which minimizes costs and disruption to

our stores and benefits our sales and customer experience. We expect a typical remodel in 2011 will take seven weeks; a reduction of

approximately 50 percent since 2007.

As a result of our in-store experience and other initiatives, we continue to see improvement in our customer service scorecard results. Customer

service scores are derived from direct customer surveys conducted by an independent research firm.

For discussion of our financial results, see Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

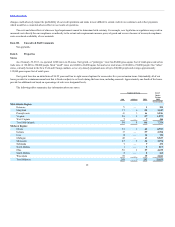

Our expansion strategy has been, and will continue to be, designed to achieve profitable growth. At the time of our initial public offering in 1992, we

had 79 stores in the Midwest. As of year-end 2010, we operated 1,089 stores. We have stores in 49 states and in every large and intermediate sized market in

the United States.

Number of stores 1,058 31 1,089 40 1,129

Gross square footage (in millions) 93 3 96 3 99

Retail selling square footage (in millions) 78 2 80 2 82

We expect approximately two-thirds of our new stores in 2011 to be what we consider “small” stores (approximately 64,000 square feet of retail space).

Though our expansion rate has slowed in recent years, we will continue to focus our future expansion efforts on opportunistic acquisitions as well as fill-in

stores in our better performing markets.

The Kohl’s concept has proven to be transferable to markets across the country. New market entries are supported by extensive advertising and

promotions which are designed to introduce new customers to the Kohl’s concept of brands, value and convenience. Additionally, we have been successful in

acquiring, refurbishing and operating locations previously operated by other retailers. Approximately one-fourth of our current stores are take-over locations,

which facilitated our initial entry into several markets. Once a new market is established, we add additional stores to further strengthen market share and

enhance profitability.

We remain focused on providing the solid infrastructure needed to ensure consistent, low-cost execution. We proactively invest in distribution capacity

and regional management to facilitate growth in new and existing markets. Our central merchandising organization tailors merchandise assortments to reflect

regional climates and preferences. Management information systems support our low-cost culture by enhancing productivity and providing the information

needed to make key merchandising decisions.

5