McDonalds 2014 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2014 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

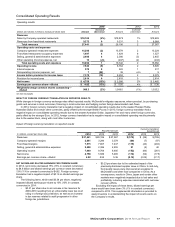

22 McDonald’s Corporation 2014 Annual Report

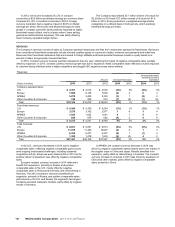

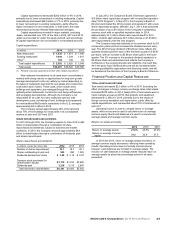

INTEREST EXPENSE

Interest expense increased 9% and 1% in 2014 and 2013,

respectively, primarily due to higher average debt balances. In

addition, interest expense in 2013 benefited from lower average

interest rates.

NONOPERATING (INCOME) EXPENSE, NET

Nonoperating (income) expense, net

In millions 2014 2013 2012

Interest income $(20) $(15) $ (28)

Foreign currency and hedging activity 20 8 9

Other expense 745 28

Total $ 7 $ 38 $ 9

Interest income consists primarily of interest earned on short-term

cash investments. Foreign currency and hedging activity includes

net gains or losses on certain hedges that reduce the exposure to

variability on certain intercompany foreign currency cash flow

streams.

PROVISION FOR INCOME TAXES

In 2014, 2013 and 2012, the reported effective income tax rates

were 35.5%, 31.9% and 32.4%, respectively.

In 2014, the higher effective income tax rate was primarily due

to a change in tax reserves for 2003-2010 resulting from an

unfavorable lower tax court ruling in a foreign tax jurisdiction, as

well as the impact of changes in tax reserves related to audit

progression in multiple foreign tax jurisdictions. Excluding these

items, the effective income tax rate would have been 31.4%.

In 2013, the effective income tax rate included a tax benefit of

nearly $50 million, reflecting the retroactive impact of certain tax

benefits as a result of the American Taxpayer Relief Act of 2012.

In 2012, the effective income tax rate reflected the negative

impact of certain tax benefits in the U.S. that had expired at

December 31, 2011 and were reinstated retroactively in 2013 as

noted above.

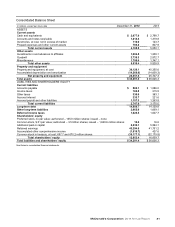

Consolidated net deferred tax liabilities included tax assets,

net of valuation allowance, of $1.6 billion in 2014 and $1.5 billion

in 2013. Substantially all of the net tax assets are expected to be

realized in the U.S. and other profitable markets.

RECENTLY ISSUED ACCOUNTING STANDARD

In May 2014, the Financial Accounting Standards Board issued

guidance codified in Accounting Standards Codification ("ASC")

606, "Revenue Recognition - Revenue from Contracts with

Customers," which amends the guidance in ASC 605, "Revenue

Recognition," and becomes effective beginning January 1, 2017.

The Company is currently evaluating the impact of the provisions

of ASC 606.

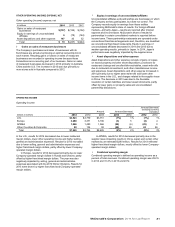

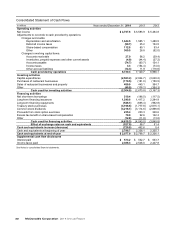

Cash Flows

The Company generates significant cash from its operations and

has substantial credit availability and capacity to fund operating

and discretionary spending such as capital expenditures, debt

repayments, dividends and share repurchases.

Cash provided by operations totaled $6.7 billion and

exceeded capital expenditures by $4.1 billion in 2014, while cash

provided by operations totaled $7.1 billion and exceeded capital

expenditures by $4.3 billion in 2013. In 2014, cash provided by

operations decreased $390 million or 5% compared with 2013

primarily due to lower operating results, partly offset by lower

income tax payments. In 2013, cash provided by operations

increased $155 million or 2% compared with 2012 primarily due to

increased operating results.

Cash used for investing activities totaled $2.3 billion in 2014,

a decrease of $369 million compared with 2013. The decrease

primarily reflected lower capital expenditures, a decrease in other

investing activities related to short-term time deposits and higher

proceeds from sales of restaurant businesses. Cash used for

investing activities totaled $2.7 billion in 2013, a decrease of $493

million compared with 2012. The decrease primarily reflected

lower capital expenditures and a decrease in other investing

activities related to short-term time deposits.

Cash used for financing activities totaled $4.6 billion in 2014,

an increase of $575 million compared with 2013, primarily due to

higher treasury stock purchases, partly offset by an increase in net

borrowings. Cash used for financing activities totaled $4.0 billion in

2013, an increase of $193 million compared with 2012, primarily

due to lower net debt issuances and higher dividend payments,

partly offset by lower treasury stock purchases.

The Company’s cash and equivalents balance was $2.1

billion and $2.8 billion at year end 2014 and 2013, respectively. In

addition to cash and equivalents on hand and cash provided by

operations, the Company can meet short-term funding needs

through its continued access to commercial paper borrowings and

line of credit agreements.

RESTAURANT DEVELOPMENT AND CAPITAL EXPENDITURES

In 2014, the Company opened 1,298 traditional restaurants and 18

satellite restaurants (small, limited-menu restaurants for which the

land and building are generally leased), and closed 317 traditional

restaurants and 170 satellite restaurants. In 2013, the Company

opened 1,393 traditional restaurants and 45 satellite restaurants

and closed 295 traditional restaurants and 194 satellite

restaurants. The majority of restaurant openings and closings

occurred in the major markets in both years. The Company closes

restaurants for a variety of reasons, such as existing sales and

profit performance or loss of real estate tenure.

Systemwide restaurants at year end(1)

2014 2013 2012

U.S. 14,350 14,278 14,157

Europe 7,855 7,602 7,368

APMEA 10,345 9,918 9,454

Other Countries & Corporate 3,708 3,631 3,501

Total 36,258 35,429 34,480

(1) Includes satellite units at December 31, 2014, 2013 and 2012, as follows:

U.S.—919, 973, 997; Europe—273, 261, 246; APMEA (primarily Japan)—

641, 733, 871; Other Countries & Corporate—433, 451, 453.

Approximately 70% of Company-operated restaurants and

nearly 75% of franchised restaurants were located in the major

markets at the end of 2014. Over 80% of the restaurants at year-

end 2014 were franchised.