McDonalds 2014 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2014 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

26 McDonald’s Corporation 2014 Annual Report

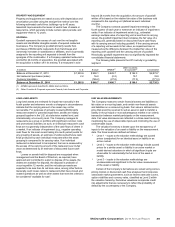

life and the expected dividend yield. The Company uses historical

data to determine these assumptions and if these assumptions

change significantly for future grants, share-based compensation

expense will fluctuate in future years. The fair value of each RSU

granted is equal to the market price of the Company’s stock at

date of grant less the present value of expected dividends over the

vesting period.

Long-lived assets impairment review

Long-lived assets (including goodwill) are reviewed for impairment

annually in the fourth quarter and whenever events or changes in

circumstances indicate that the carrying amount of an asset may

not be recoverable. In assessing the recoverability of the

Company’s long-lived assets, the Company considers changes in

economic conditions and makes assumptions regarding estimated

future cash flows and other factors. Estimates of future cash flows

are highly subjective judgments based on the Company’s

experience and knowledge of its operations. These estimates can

be significantly impacted by many factors including changes in

global and local business and economic conditions, operating

costs, inflation, competition, and consumer and demographic

trends. A key assumption impacting estimated future cash flows is

the estimated change in comparable sales. If the Company’s

estimates or underlying assumptions change in the future, the

Company may be required to record impairment charges. Based

on the annual goodwill impairment test, conducted in the fourth

quarter, the Company does not have any reporting units (defined

as each individual country) with risk of material goodwill

impairment.

Litigation accruals

In the ordinary course of business, the Company is subject to

proceedings, lawsuits and other claims primarily related to

competitors, customers, employees, franchisees, government

agencies, intellectual property, shareholders and suppliers. The

Company is required to assess the likelihood of any adverse

judgments or outcomes to these matters as well as potential

ranges of probable losses. A determination of the amount of

accrual required, if any, for these contingencies is made after

careful analysis of each matter. The required accrual may change

in the future due to new developments in each matter or changes

in approach such as a change in settlement strategy in dealing

with these matters. The Company does not believe that any such

matter currently being reviewed will have a material adverse effect

on its financial condition or results of operations.

Income taxes

The Company records a valuation allowance to reduce its deferred

tax assets if it is more likely than not that some portion or all of the

deferred assets will not be realized. While the Company has

considered future taxable income and ongoing prudent and

feasible tax strategies, including the sale of appreciated assets, in

assessing the need for the valuation allowance, if these estimates

and assumptions change in the future, the Company may be

required to adjust its valuation allowance. This could result in a

charge to, or an increase in, income in the period such

determination is made.

The Company operates within multiple taxing jurisdictions and

is subject to audit in these jurisdictions. The Company records

accruals for the estimated outcomes of these audits, and the

accruals may change in the future due to new developments in

each matter.

In 2014, the Company increased the balance of unrecognized

tax benefits related to tax positions taken in prior years by $505

million, most of which came from foreign-related tax matters. After

considering the impact of deferred tax offsets, interest and

penalties, these foreign-related tax matters impacted the effective

tax rate by 4.1%. See the Income Taxes footnote in the

Consolidated Financial Statements for the related tax

reconciliations. The most significant new developments in 2014

are described below.

In 2014, the Company received an unfavorable lower tax

court ruling in a foreign tax jurisdiction related to exempt income

matters. As a result of this new information, the Company changed

its judgment on the sustainability of this tax position for 2003-2010

and recorded an increase in the gross unrecognized tax benefits

of $188 million. The Company intends to pursue all available

remedies to defend this tax position.

In addition, the Company received new information from tax

authorities during the progression of tax audits in multiple foreign

tax jurisdictions, including the receipt of proposed tax

assessments primarily related to transfer pricing matters. As a

result of this new information, the Company changed its judgment

on the measurement of the related unrecognized tax benefits and

recorded an increase in the gross unrecognized tax benefits of

$207 million. The Company settled certain of these tax audits in

2014 and plans to defend its position with the tax authorities on

the remaining audits.

Also in 2014, the Internal Revenue Service (“IRS”) concluded

its field examination of the Company’s U.S. Federal income tax

returns for 2009 and 2010. In connection with this examination,

the Company agreed to certain adjustments proposed by the IRS.

The liabilities previously recorded related to these adjustments

were adequate. In connection with this examination, the Company

also received notices of proposed adjustments ("NOPAs") related

to certain transfer pricing matters and engaged in audit defense

discussions with the IRS. As a result of this new information, the

Company changed its judgment on the measurement of the

related unrecognized tax benefits and recorded an increase in the

gross unrecognized tax benefits of $38 million. The Company

disagrees with these proposed adjustments and will file a protest

with the IRS Appeals Office in 2015.

While the Company cannot predict the ultimate resolution of

the aforementioned tax matters, we believe that the liabilities

recorded are appropriate and adequate as determined in

accordance with Topic 740 - Income Taxes of the Accounting

Standards Codification (“ASC”).

In 2012, the IRS completed its examination of the Company's

U.S. federal income tax returns for 2007 and 2008. The Company

and the IRS reached an agreement on adjustments that had been

previously proposed by the IRS. The agreement did not have a

material impact on the Company's cash flows, results of

operations or financial position.

Deferred U.S. income taxes have not been recorded for

temporary differences totaling $15.4 billion related to investments

in certain foreign subsidiaries and corporate affiliates. The

temporary differences consist primarily of undistributed earnings

that are considered permanently invested in operations outside

the U.S. If management's intentions change in the future, deferred

taxes may need to be provided.

EFFECTS OF CHANGING PRICES—INFLATION

The Company has demonstrated an ability to manage inflationary

cost increases effectively. This ability is because of rapid inventory

turnover, the ability to adjust menu prices, cost controls and

substantial property holdings, many of which are at fixed costs and

partly financed by debt made less expensive by inflation.