Nike 2006 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2006 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

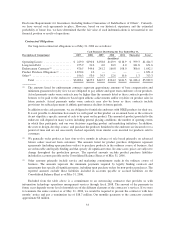

The discussion following includes disclosure of pre-tax income for our operating segments. We have

reported pre-tax income for each of our operating segments in accordance with Statement of Financial

Accounting Standard No. 131, “Disclosures about Segments of an Enterprise and Related Information.” As

discussed in Note 17 — Operating Segments and Related Information in the accompanying Notes to

Consolidated Financial Statements, certain corporate costs are not included in pre-tax income of our operating

segments.

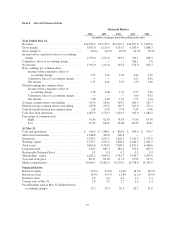

U.S. Region

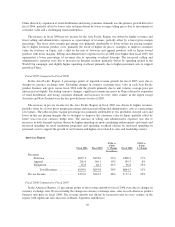

Fiscal 2006 Fiscal 2005

FY06 vs.

FY05

% Change Fiscal 2004

FY05 vs.

FY04

% Change

(In millions)

Revenues

Footwear ................... $3,832.2 $3,358.2 14% $3,070.4 9%

Apparel .................... 1,591.6 1,457.7 9% 1,433.5 2%

Equipment .................. 298.7 313.4 (5)% 277.9 13%

Total Revenues .......... $5,722.5 $5,129.3 12% $4,781.8 7%

Pre-tax Income .................. $1,244.5 $1,127.9 10% $1,007.3 12%

Fiscal 2006 Compared to Fiscal 2005

The increase in footwear revenues was due to a strong increase in unit sales, accounting for 12 percentage

points of the growth, and an increase in the average selling price per pair, accounting for 2 percentage points of

the growth. The strong unit increase was driven by increased consumer demand across a majority of the footwear

product categories, most significantly high demand for our Jordan branded and sport culture products. The higher

average selling price per pair was primarily due to increased consumer demand for products with a suggested

retail price over $100, driven by Jordan branded products as well as NIKE branded sport performance and sport

culture products.

The increase in U.S. apparel sales for fiscal 2006 was driven by increased unit sales in NIKE and Jordan

branded apparel, partially offset by sales declines in licensed apparel, primarily due to the expiration of our

license agreement with the NBA in the second quarter of fiscal 2005. The increases in NIKE branded apparel

were primarily due to increased sales of sport performance products.

For the U.S. Region, the increase in pre-tax income for fiscal 2006 as compared to 2005 was driven by

higher revenues and lower selling and administrative expenses as a percentage of revenues, more than offsetting

a lower gross margin percentage. The lower gross margin percentage was primarily the result of lower in-line net

pricing margins for footwear due to higher product costs, primarily the result of higher oil prices, and additional

costs incurred to meet strong footwear unit demand. Selling and administrative expenses were higher than fiscal

2005, but represented a lower percentage of revenues due to operating overhead leverage. The increase in selling

and administrative costs was due to increases in both demand creation and operating overhead. The increase in

demand creation was primarily driven by increased spending on sports marketing endorsements and events and

increased advertising, primarily due to the global campaigns discussed above. The increase in operating overhead

spending was driven by increased spending for new NIKE-owned retail stores, higher personnel costs and higher

travel and meeting expenses.

Fiscal 2005 Compared to Fiscal 2004

The increase in footwear revenue was due to a 5 percentage point increase in unit sales and a 4 percentage point

increase in the average price per pair. The increases in unit sales and the average price per pair were due to increased

consumer demand for sport performance products, especially those with a suggested retail price over $100.

27