Siemens 2015 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2015 Siemens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

Consolidated Financial Statements

As of September , and the VaR relating to foreign

currency exchange rates was € million and € million. This

VaR was calculated under consideration of items of the Consol-

idated Statement of Financial Position in addition to firm com-

mitments which are denominated in foreign currencies, as well

as foreign currency denominated cash flows from forecast

transactions for the following twelve months. A higher volatil-

ity between the U. S. dollar and the euro in comparison to prior

year resulted in an increase of the VaR. Furthermore, the VaR

was influenced by changes to hedging level and hedging hori-

zon with regard to foreign currency denominated cash flows

from forecast transactions.

Translation risk

Many Siemens units are located outside the euro zone. Since

the financial reporting currency of Siemens is the euro, the fi-

nancial statements of these subsidiaries are translated into

euro for the preparation of the Consolidated Financial State-

ments. To consider the effects of foreign currency translation in

the risk management, the general assumption is that invest-

ments in foreign-based operations are permanent and that re-

investment is continuous. Effects from foreign currency ex-

change rate fluctuations on the translation of net asset

amounts into euro are reflected in the Company’s consolidated

equity position.

INTEREST RATE RISK

Interest rate risk is the risk that the fair value or future cash

flows of a financial instrument will fluctuate because of changes

in market interest rates. This risk arises whenever interest terms

of financial assets and liabilities are different. In order to man-

age the Company’s position with regard to interest rate risk, in-

terest income and interest expenses, Corporate Treasury per-

forms a comprehensive corporate interest rate risk management

by using fixed or variable interest rates from bond issuances

and derivative financial instruments when appropriate. The in-

terest rate risk relating to the Group, excluding SFS’ business, is

mitigated by managing interest rate risk actively relatively to a

benchmark. The interest rate risk relating to the SFS’ business is

managed separately, considering the term structure of SFS’s fi-

nancial assets and liabilities. The Company’s interest rate risk

results primarily from the funding in U. S. dollar, GBP and euro.

If there are no conflicting country-specific regulations, all

Siemens operating units generally obtain any required financ-

ing through Corporate Treasury in the form of loans or inter-

company clearing accounts. The same concept is adopted for

deposits of cash generated by the units.

As of September , and the VaR relating to the inter-

est rate was € million and € million. In fiscal the

interest VaR mainly increased due to the issuance of fixed-rate

US$ bonds and higher interest rate volatilities for EUR and US$.

The issuance of fixed-rate U. S. dollar bonds locked in a fixed

rate and thus avoided additional cash flow risk.

EQUITY PRICE RISK

Siemens’ investment portfolio consists of direct and indirect

investments in publicly traded companies held for purposes

other than trading. The direct participations result mainly from

strategic partnerships, strengthening Siemens’ focus on its

core business activities or compensation from merger and ac-

quisitions transactions; indirect investments in fund shares are

mainly transacted for financial reasons.

These investments are monitored based on their current mar-

ket value, affected primarily by fluctuations in the volatile tech-

nology-related markets worldwide. As of September ,

and the market value of Siemens’ portfolio in publicly

traded companies was € , million compared to € , mil-

lion in the prior year. The increase is due mainly to higher mar-

ket values of our stakes in OSRAM and AtoS.

As of September , and , the VaR relating to the eq-

uity price was € and € million. The increase is due

mainly to higher market values related to the above-mentioned

stakes and an increased volatility.

LIQUIDITY RISK

Liquidity risk results from the Company’s inability to meet its

financial liabilities. Siemens follows a deliberated financing

policy that is aimed towards a balanced financing portfolio, a

diversified maturity profile and a comfortable liquidity cushion.

Siemens mitigates liquidity risk by the implementation of an

effective working capital and cash management, arranged

credit facilities with highly rated financial institutions, via a

debt issuance program and via a global multi-currency com-

mercial paper program. Liquidity risk may also be mitigated by

the Siemens Bank GmbH, which increases the flexibility of de-

positing cash or refinancing.

In addition, Siemens constantly monitors funding options

available in the capital markets, as well as trends in the avail-

ability and costs of such funding, with a view to maintaining

financial flexibility and limiting repayment risks.

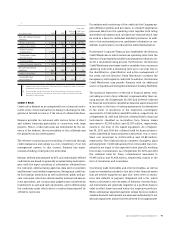

The following table reflects the contractually fixed pay-offs for

settlement, repayments and interest. The disclosed expected

undiscounted net cash outflows from derivative financial liabil-

ities are determined based on each particular settlement date

of an instrument and based on the earliest date on which

Siemens could be required to pay. Cash outflows for financial

liabilities (including interest) without fixed amount or timing

are based on the conditions existing at September , .