Sprint - Nextel 2006 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2006 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

Adoption of Statement of Financial Accounting Standards No. 123R

Effective January 1, 2006, we adopted SFAS No. 123R, Share-Based Payment, which revises SFAS No. 123.

SFAS No. 123R requires us to measure the cost of employee services received in exchange for an award of

equity-based securities using the fair value of the award on the date of grant, and we recognize that cost over

the period that the award recipient is required to provide service to us in exchange for the award. Any awards

of liability instruments to employees would be remeasured at fair value at each reporting date through

settlement.

We adopted SFAS No. 123R using the modified prospective transition method and, accordingly, the results of

prior periods have not been restated. This method requires that the provisions of SFAS No. 123R generally are

applied only to share-based awards granted, modified, repurchased, or cancelled on or after January 1, 2006.

As we voluntarily adopted fair value accounting for share-based awards effective January 1, 2003 (under

SFAS No. 123 as amended by SFAS No. 148, Accounting for Stock-Based Compensation — Transition and

Disclosure), using the prospective method, we measured the cost of share-based awards granted or modified

on or after January 1, 2003 using the fair value of the award and began recognizing that cost in our

consolidated statements of operations over the service period. We will recognize the remaining cost of these

awards over the remaining service period following the provisions of SFAS No. 123R. For those grants issued

prior to January 1, 2003 that were unvested and outstanding as of January 1, 2006, we started recognizing the

remaining cost of these awards over the remaining service period as required by the new standard. The

adoption of SFAS No. 123R did not have a material effect on our consolidated financial statements.

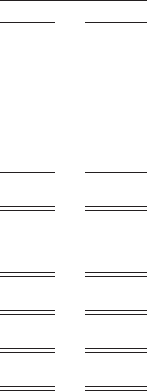

The following table illustrates the effect on net income (loss) and earnings (loss) per common share of share-

based awards included in net income (loss) and the effect on net income (loss) and earnings (loss) per common

share for grants issued prior to January 1, 2003, had we applied the fair value recognition provisions of

SFAS No. 123 to those grants in 2005 and 2004.

2005 2004

Year Ended

December 31,

(In millions)

Net income (loss), as reported ............................................ $1,785 $(1,012)

Add: share-based compensation expense, included in reported net income (loss), net of

income tax of $111 and $47 ............................................. 192 82

Deduct: total share-based compensation expense determined under fair value based

method for all awards, net of income tax of $117 and $64 ....................... (204) (111)

Net income (loss), pro forma ............................................. $1,773 $(1,041)

Earnings (loss) per common share

Basic, as reported ..................................................... $ 0.87 $ (0.71)

Basic, pro forma ..................................................... $ 0.87 $ (0.73)

Diluted, as reported ................................................... $ 0.87 $ (0.71)

Diluted, pro forma .................................................... $ 0.86 $ (0.73)

Share-based compensation cost charged against net income (loss) and charged against income (loss) from

continuing operations for our share-based award plans was $361 million and $338 million for 2006,

$303 million and $254 million for 2005 and $129 million and $85 million for 2004, respectively. Of the total

share-based compensation amounts, $234 million and $81 million in 2005 and 2004, respectively, related to

stock-based grants issued after December 31, 2002; $37 million and $48 million in 2005 and 2004,

respectively, related to the recombination of our two tracking stocks (note 16), and $32 million in 2005 related

to the separation of certain of our employees employed with us prior to the Sprint-Nextel merger.

F-25

SPRINT NEXTEL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)