Sprint - Nextel 2006 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2006 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

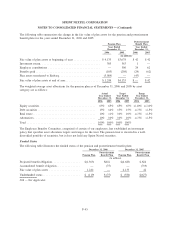

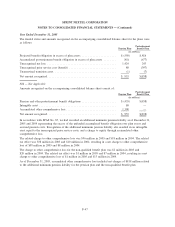

Bank Credit Facilities

Our bank credit facility provides for total unsecured financing capacity of $6.0 billion. As of December 31,

2006, we had $2.6 billion of outstanding letters of credit, including a $2.5 billion letter of credit that is

required by the FCC’s Report and Order, and $514 million in commercial paper, net of discounts, backed by

the facility, resulting in $2.9 billion of available revolving credit. We also have an additional $16 million of

outstanding letters of credit as of December 31, 2006 used for various financial obligations that are not backed

by our bank credit facility.

On December 19, 2005, we entered into our bank credit facility, which consisted not only of the five year

$6.0 billion revolving credit facility, but also a 364 day $3.2 billion term loan. The terms of this loan provide

for an interest rate equal to the London Interbank Offered Rate, or LIBOR, or Prime Rate plus a spread that

varies depending on our credit ratings. This bank credit facility does not include a rating trigger that would

allow the lenders involved to terminate the facility in the event of a credit rating downgrade. The $6.0 billion

revolving credit facility is also subject to a facility fee on the total facility which is payable quarterly. Facility

fees can vary between 4 to 15 basis points based upon our credit ratings. This facility replaced an existing

credit agreement, which included a $4.0 billion revolving credit facility and a $2.2 billion term loan.

Our credit facility requires compliance with a financial ratio test as defined in the credit agreement. The

maturity dates of the loans may accelerate if we do not comply with the financial ratio test. As of

December 31, 2006, we were in compliance with the financial ratio test under our credit facility. We are also

obligated to repay the loans if certain change of control events occur. Borrowings under the facility are

unsecured.

The credit facility also contains covenants which limit our ability and the ability of some of our subsidiaries to

incur additional indebtedness, including guaranteeing obligations of other entities and creating liens, to

consolidate, merge or sell all or substantially all of our and their assets and to enter into transactions with

affiliates.

Our ability to borrow additional amounts under the credit facility may be restricted by provisions included in

some of our public notes that limit the incurrence of additional indebtedness in certain circumstances. The

availability of borrowings under this facility also is subject to the satisfaction or waiver of specified borrowing

conditions. As of December 31, 2006, we have satisfied the conditions under this facility.

During the second quarter 2006, we retired our $3.2 billion term loan with a portion of the proceeds received

in connection with the spin-off of Embarq. See note 2 for further details on the spin-off of Embarq.

On August 1, 2006, we repaid and terminated a credit facility that we assumed as part of the Nextel Partners

acquisition, which had a $500 million outstanding term loan and provided for a $100 million revolving credit

facility, which had no outstanding borrowings against it.

In 2005, we entered into a revolving credit facility of $1.0 billion. This facility was unsecured and was

structured as a 364-day credit line with a subsequent one-year, $1.0 billion term-out option, which had no

borrowings drawn against it and was permitted to expire during the second quarter 2006.

Commercial Paper

In April 2006, we commenced a commercial paper program, which has reduced our borrowing costs by

allowing us to issue short-term debt at lower rates than those available under our $6.0 billion revolving credit

facility. The $2.0 billion program is backed by our revolving credit facility and reduces the amount we can

borrow under the facility to the extent of the commercial paper outstanding. As of December 31, 2006, we had

$514 million of commercial paper outstanding, net of discounts, included in the current maturities of long-

term debt with a weighted average interest rate of 5.515% and a weighted average maturity of about 47 days.

F-38

SPRINT NEXTEL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)