Sprint - Nextel 2006 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2006 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

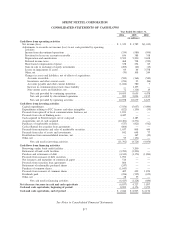

Earnings (Loss) per Common Share

Basic earnings (loss) per common share is calculated by dividing income (loss) available to common

shareholders by the weighted average number of common shares outstanding during the period. Diluted

earnings (loss) per common share adjusts basic earnings (loss) per common share for the effects of potentially

dilutive common shares. Potentially dilutive common shares include the dilutive effects of shares issuable

under our equity plans computed using the treasury stock method, and the dilutive effects of shares issuable

upon the conversion of our convertible senior notes computed using the if-converted method.

Dilutive shares issuable under our equity plans used in calculating earnings per common share were about

22 million shares for 2006. All 11 million shares issuable upon the assumed conversion of our convertible

senior notes could potentially dilute earnings per common share in the future, however, they were excluded

from the calculation of diluted earnings per common share for 2006 due to their antidilutive effects.

Additionally, about 115 million average shares issuable under the equity plans that could also potentially dilute

earnings per common share in the future were excluded from the calculation of diluted earnings per common

share in 2006 as the exercise prices exceeded the average market price during this period.

Dilutive shares issuable under our equity plans used in calculating earnings per common share were about

21 million shares for 2005. As of December 31, 2005, there were 11 million shares issuable upon the assumed

conversion of our convertible senior notes that could have potentially diluted earnings per common share in

the future, but were excluded from the calculation of diluted earnings per common share for 2005 due to their

antidilutive effects. Additionally, as of December 31, 2005, there were about 66 million average shares

issuable under the equity plans that could also have potentially diluted earnings per common share in the

future, however, they were excluded from the calculation of diluted earnings per common share in 2005 as the

exercise prices exceeded the average market price during this period.

Shares issuable under our equity plans were antidilutive in 2004 because we incurred net losses from

continuing operations. Although not used in the determination of earnings (loss) per common share for 2004,

we had about 12 million shares issuable under the equity plans whose exercise prices were below the average

market price during this period. As of December 31, 2004, there were about 88 million average shares issuable

under the equity plans that could have potentially diluted earnings per common share in the future, however,

they were excluded from the calculation of diluted earnings per common share in 2004 as the exercise prices

exceeded the average market price during this period.

Significant New Accounting Pronouncements

In September 2006, the FASB issued SFAS No. 157, Fair Value Measurements. This statement defines fair

value and establishes a framework for measuring fair value. Additionally, this statement expands disclosure

requirements for fair value with a particular focus on measurement inputs. SFAS No. 157 is effective for our

quarterly reporting period ending March 31, 2008.

In September 2006, the EITF reached a consensus on Issue No. 06-1, Accounting for Consideration Given by

a Service Provider to Manufacturers or Resellers of Equipment Necessary for an End-Customer to Receive

Service from the Service Provider. EITF Issue No. 06-1 provides guidance regarding whether the consideration

given by a service provider to a manufacturer or reseller of specialized equipment should be characterized as a

reduction of revenue or an expense. This issue is effective for our quarterly reporting period ending March 31,

2008. Entities are required to recognize the effects of applying this issue as a change in accounting principle

through retrospective application to all prior periods unless it is impracticable to do so.

In June 2006, the EITF reached a consensus on Issue No. 06-3, How Taxes Collected from Customers and

Remitted to Governmental Authorities Should Be Presented in the Income Statement (That Is, Gross Versus Net

Presentation). EITF Issue No. 06-3 requires that companies disclose their accounting policy regarding the

gross or net presentation of certain taxes. Taxes within the scope of EITF Issue No. 06-3 are any tax assessed

by a governmental authority that is directly imposed on a revenue-producing transaction between a seller and

F-16

SPRINT NEXTEL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)