Sprint - Nextel 2006 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2006 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

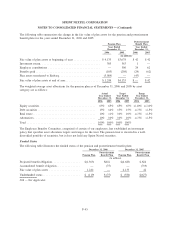

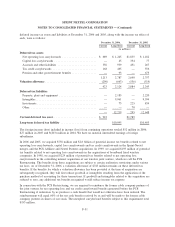

The components of the pension expense and postretirement benefit expense for the years ended December 31,

2006, 2005 and 2004 are detailed below:

2006 2005 2004 2006 2005 2004

Year Ended December 31, Year Ended December 31,

Pension Plan Postretirement Benefit Plan

(in millions)

Service cost .................................... $ 20 $134 $133 $ 7 $13 $13

Interest cost .................................... 149 264 250 18 48 56

Expected return on plan assets ...................... (195) (328) (303) (1) (3) (3)

Amortization of transition asset ..................... — — (2) — (1) (1)

Amortization of prior service cost ................... 6 16 16 (25) (57) (49)

Recognized net actuarial loss ....................... 38 110 89 10 28 28

Curtailment loss — partial freeze of benefits accruals ..... — 4 ————

Net benefit expense .............................. $ 18 $200 $183 $ 9 $28 $44

Net benefit expense includes $21 million, $63 million and $57 million for the years ended December 31,

2006, 2005 and 2004, respectively, that was allocated to the Local segment prior to the spin-off of Embarq.

We believe these amounts approximate the expense related to participants designated to work for Embarq and,

accordingly, these amounts are included in discontinued operations in the accompanying consolidated

statements of operations. In 2006, all pension service costs are attributable to the Local segment as our

pension benefits for continuing Sprint Nextel employees were frozen as of December 31, 2005.

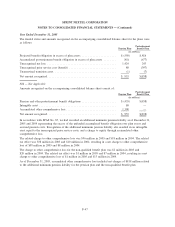

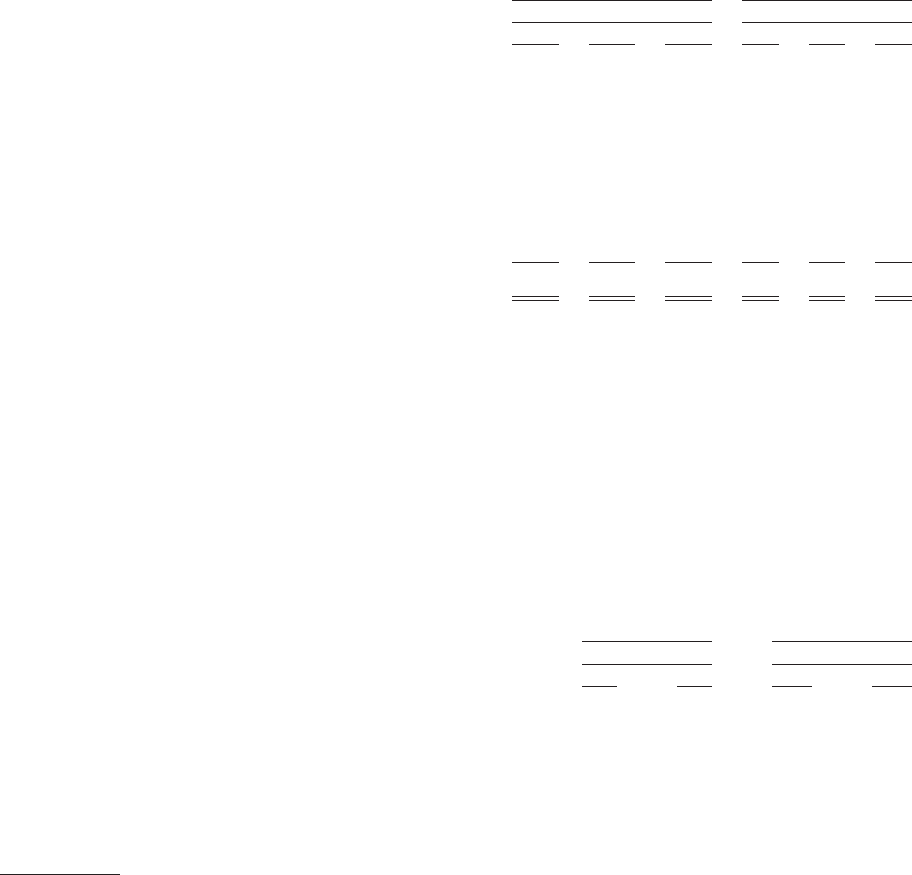

Benefit Obligations

The actuarial assumptions used to compute the funded status for the plans are based upon information

determined as of December 31, 2006 and 2005, and are as follows:

2006 2005 2006 2005

As of December 31, As of December 31,

Pension Plan

Postretirement

Benefit Plan

Actuarial assumptions at end of year:

Discount rate ....................................... 6.20% 5.75% 6.20% 5.75%

Expected rate of compensation increase .................... N/A 4.25% 4.25% 4.25%

Initial healthcare cost trend rate .......................... N/A N/A 8.6% 9.3%

Ultimate healthcare cost trend rate........................ N/A N/A 5.0% 5.0%

Year ultimate trend rate is reached........................ N/A N/A 2012 2012

N/A — Not Applicable

In addition to the above rates, the discount rate used to determine benefit obligations as of the remeasurement

date of May 17, 2006, associated with the spin-off of Embarq, was 6.50%.

SFAS Nos. 87 and 106 require that the calculation of a benefit obligation include a discount rate that reflects

the rate at which the benefits could effectively be settled and further suggest that this rate reflect the rates of

return currently available on high quality fixed income securities whose cash flows (via coupon and maturities)

match the timing and amount of future benefit payments of the plan. Accordingly, our actuaries completed a

cash flow bond matching analysis consistent with this methodology.

F-43

SPRINT NEXTEL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)