Windstream 2009 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2009 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

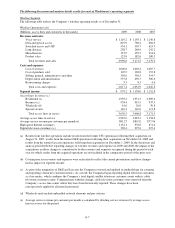

Business Trends

The following is a discussion of trends affecting Windstream’s operations.

•Access line losses: Wireline voice and switched access revenues are expected to continue to be adversely impacted

by future declines in access lines due to competition in the telecommunications industry from cable television

providers, wireless communications providers, and providers using other emerging technologies. As of

December 31, 2009, all of the Company’s access lines had wireless competition and approximately 64 percent of

the Company’s access lines had fixed line voice competition, which represented an increase in fixed line

competition of approximately 4 percent from December 31, 2008. After removing the impact of residential lines

acquired from D&E and Lexcom of 82,000 and 15,000, respectively, residential lines decreased 87,000, or 4.5

percent during 2009, primarily due to the effects of competition. After removing the impact of business lines

acquired from D&E and Lexcom of 63,000 and 7,000, respectively, business lines decreased 48,000, or 5.3

percent during 2009, primarily due to weakness in the general economic environment, competitive pressures, and

the migration of services to larger circuits with enhanced functionality representing lost access lines but not a lost

customer relationship. We believe weakness in the economic environment has caused some businesses to close or

reduce staff, which has had a corresponding impact on the demand for business access lines. Continued weakness

in the general economic environment may contribute to further acceleration of line losses.

•Product bundles: To combat competitive pressures, the Company continues to emphasize its bundled products and

services. Our residential customers can bundle local phone, high-speed Internet, long distance and video services.

These bundles provide customers with one convenient location to obtain all their communications and entertainment

needs, a convenient billing solution and bundle discounts. Operating trends for access lines and high-speed Internet

customers were favorably impacted during the second half of the year by the Company’s latest bundle promotion,

which offers a price for life guarantee and package discount on its local phone, unlimited national calling and high-

speed Internet bundle. In addition, during the second quarter of 2009, we began offering bundle discounts to

businesses that choose to bundle their phone, high-speed Internet and long distance services with Windstream. We

believe that product bundles positively impact our customer retention, and the associated discounts provide our

customers the best value for their communications and entertainment needs. In an effort to further develop enhanced

services and bundled product offerings, the Company will continue to invest in its network to offer faster speeds in

its high-speed Internet offerings. As of December 31, 2009, the Company could deliver speeds of 3Mb to

approximately 96 percent of its addressable lines. Additionally, speeds of 6Mb and 12Mb are available to

approximately 65 percent and 34 percent of its high-speed Internet addressable lines, respectively.

•High-speed Internet: Growth in high-speed Internet sales, together with the continued migration to higher speeds,

are expected to continue to offset some of the revenue declines from the unfavorable access line trends discussed

above. After removing the impact of high-speed Internet customers acquired from D&E and Lexcom of 45,000

and 9,000, respectively, the Company added approximately 98,900 high-speed Internet customers during 2009,

representing an approximate increase in high-speed Internet customers of 10.1 percent. As of December 31, 2009,

Windstream provided high-speed Internet service to approximately 37.4 percent of total access lines in service,

and 55.1 percent of primary residential access lines in service. As of December 31, 2009, approximately

75 percent of total access lines had high-speed Internet competition, primarily from cable service providers, which

is relatively unchanged from December 31, 2008. We expect the pace of high-speed Internet customer growth to

slow as the number of households without high-speed Internet service continues to shrink. Competitive

expansions, primarily from cable facilities, into our service areas are expected to slow in 2010, but we could

experience some increased competition from high-speed Internet offerings from wireless competitors.

•Business data and special access: Wireline revenues and sales are expected to be favorably impacted by growth in

next generation data services provided to business customers. During 2009, revenues from next generation

services such as VPN and VLS grew 21.9 percent to approximately $45.9 million, excluding the impact of D&E

and Lexcom. Likewise, due to continued trends toward increasing data traffic, we expect growth in special access

revenues from the provisioning of circuits to wireless and other carriers. However, weakness in the general

economic environment may have the effect of suppressing near term growth in these revenues.

•Operational efficiencies: We continue to evaluate our operating structure to identify opportunities for increased

operational efficiency and effectiveness. Among other things, this involves evaluating opportunities for task

automation, network efficiency and the balancing of our workforce based on the current needs of our customers.

As a result of these efforts, the Company successfully reduced its cost of services by approximately $80.0 million

in 2009, excluding the impact of D&E and Lexcom and pension expense (see “Cost of Services”). As part of this

continuing effort, the Company announced a work force reduction in the third quarter of 2009. In conjunction

therewith, we recognized restructuring charges of approximately $9.3 million. The Company expects to realize

annual savings approximating $20.0 million from this workforce reduction.

F-3