Windstream 2009 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2009 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

FINANCIAL CONDITION, LIQUIDITY AND CAPITAL RESOURCES

Liquidity and Capital Resources

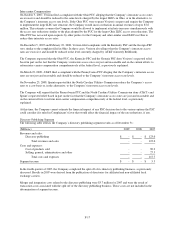

During 2009, the Company generated $1,120.8 million in cash flows from operations and increased its cash position by

$766.3 million to $1,062.9 million at December 31, 2009, primarily due to the proceeds of a $1,100.0 million debt

offering in 2009 (see “Cash Flows – Financing Activities”). We expect that cash on hand, along with cash generated

from operations over the next year, will be adequate to finance our ongoing operating requirements, capital

expenditures, scheduled principle payments of long-term debt, the payment of dividends in 2010 and the NuVox

acquisition. In addition, we expect these same sources, together with available capacity under our $500.0 million

revolving credit facility (see Note 5), will be sufficient to finance the acquisition of Iowa Telecom.

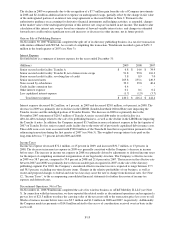

The Company’s board of directors has adopted a current dividend practice for the payment of quarterly cash dividends

at a rate of $0.25 per share of the Company’s common stock. This practice can be changed at any time at the discretion

of the board of directors, and is subject to the Company’s restricted payment capacity under its debt covenants as

further discussed below. Dividends paid to shareholders were $1.00 per share during 2009, totaling $437.4 million.

Windstream also paid $109.2 million to shareholders in January 2010 pursuant to a $0.25 quarterly dividend declared

during the fourth quarter of 2009.

In February 2008, the Windstream Board of Directors approved a stock repurchase program for up to $400 million of

the Company’s common stock continuing until December 31, 2009. During 2009, the Company repurchased

13.0 million shares totaling $121.3 million bringing total repurchases under the stock repurchase program to

29.0 million shares for approximately $321.6 million. The stock repurchase program expired on December 31, 2009.

As of December 31, 2009, the Company had approximately $783.0 million of restricted payment capacity as governed

by its credit facility. The Company builds additional capacity through cash generated from operations while dividend

payments, share repurchases and other certain restricted investments reduce the available restricted payments capacity.

The Company will continue to opportunistically consider free cash flow accretive initiatives, including strategic

opportunities and debt repurchases.

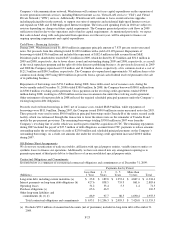

Additionally, during October of 2009, Windstream received consent from its lenders to an amendment and restatement

of its $2,148.4 million senior secured credit facility (the “Amendment”). Windstream amended and restated its senior

secured credit facility to, among other things, extend the maturities of the facility and amend certain covenants to

afford Windstream additional flexibility, resulting in increased interest rates on the extended maturities. The extended

maturities and related interest rate increases associated with the Amendment as of December 31, 2009 were as follows:

Non-extended Extended Total

Due

Amount

(Millions)

Interest

Rate Increase

(Basis Points) Due

Amount

(Millions)

Amount

(Millions)

Senior secured credit facility:

Tranche A - variable rates July 17, 2011 $114.4 100 July 17, 2013 $ 168.9 $ 283.3

Tranche B - variable rates July 17, 2013 $289.8 125 December 17, 2015 $1,075.3 $1,365.1

Revolving line of credit -

variable rates (a) July 17, 2011 $152.4 100 July 17, 2013 $ 347.6 $ 500.0

(a) As of December 31, 2009, the Company had repaid the full amount outstanding under the revolving line of credit.

As of December 31, 2009, the Company had $6,295.2 million in long-term debt outstanding, including current maturities

(see Note 5). This outstanding debt is principally comprised of approximately $2,148.4 million secured primarily under

the Company’s senior secured credit facility and approximately $4,146.8 million in unsecured senior notes. Scheduled

principal payments for debt outstanding as of December 31, 2009 for each of the twelve month periods ended

December 31, 2010, 2011, 2012, 2013 and 2014 were $23.8 million, $139.4 million, $50.4 million, $1,242.6 million and

$10.8 million, respectively. Scheduled principle payments remaining after 2014 approximate $4,867.4 million.

The terms of the senior secured credit facility and indentures include customary covenants that, among other things,

require Windstream to maintain certain financial ratios, restrict its ability to incur additional indebtedness and limit its

cash payments. These financial ratios include a maximum leverage ratio of 4.5 to 1.0 and a minimum interest coverage

F-20