Windstream 2009 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2009 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

Changes in the market value of this portion of the swap, which has an unamortized notional value of $96.3 million as

of December 31, 2009, are recognized in net income, including a $3.0 million gain in the consolidated statement of

income in 2009. Changes in the market value of the designated portion of the swaps are recognized in other

comprehensive income.

As of December 31, 2009, the unhedged portion of the Company’s variable rate senior secured credit facility was

$569.7 million, or approximately 9.1 percent of its total outstanding long-term debt. Windstream has estimated its

interest rate risk using a sensitivity analysis. For variable rate debt instruments, market risk is defined as the potential

change in earnings resulting from a hypothetical adverse change in interest rates. A hypothetical increase of 100 basis

points in variable interest rates would reduce annual pre-tax earnings by approximately $5.7 million. Actual results

may differ from this estimate.

Equity Risk

The Company utilizes various financial institutions to invest its cash on hand in short-term securities. These financial

institutions are generally a party to the existing Windstream credit facility. Windstream has maintained an average cash

balance of approximately $351.2 million during the twelve months ended December 31, 2009. These monies have been

invested in both taxable funds as well as tax-exempt municipal funds, and monies will often be moved between these

two types of securities depending on their respective yields. These monies are all invested in AAA rated funds with

same day access, and thus are highly liquid.

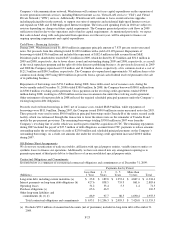

In addition, the Company has exposure to market risk through the Company’s pension plan investments. During 2009,

Windstream’s pension plan assets increased from approximately $654.0 million to $784.0 million. This increase is

primarily due to a return on plan assets of $152.0 million, or 23.2 percent, transfers from the D&E pension plan (see

Note 8) of $61.4 million and contributions of $3.3 million. Partially offsetting these increases were $51.1 million in

routine benefit payments, $35.6 million of lump sum distributions and administrative expenses. Primarily as a result of

the increase in the market value of pension assets, pension expense is expected to decline from $91.8 million

recognized in 2009, to $62.9 million in 2010. The Company does not expect to make any contributions to the plan in

2010. The amount and timing of future contributions will depend on various factors including future investment

performance, the finalization of funding regulations, changes in future discount rates and changes in demographics of

the population participating in the Company’s qualified pension plan.

Foreign Currency Risk

Although the Company does not operate in foreign countries, the Windstream pension plan invests in international

securities. As of December 31, 2009 approximately $61.5 million or 7.8 percent of total pension assets are invested in

debt or equity securities denominated in foreign currencies. The investments are diversified in terms of country,

industry and company risk, limiting the overall foreign currency exposure.

Critical Accounting Policies and Estimates

We prepare our consolidated financial statements in accordance with accounting principles generally accepted in the

United States. Our significant accounting policies are discussed in detail in Note 2. Certain of these accounting policies

as discussed below require management to make estimates and assumptions about future events that could materially

affect the reported amounts of assets, liabilities, revenues and expenses and disclosure of contingent assets and

liabilities. We believe that the estimates, judgments and assumptions made when accounting for the items described

below are reasonable, based on information available at the time they are made. However, there can be no assurance

that actual results will not differ from those estimates.

Revenue Recognition – We recognize revenues and sales as services are rendered or as products are sold in accordance

with authoritative guidance on revenue recognition. Wireline local access revenues are recognized over the period that

the corresponding services are rendered to customers. Revenues derived from other telecommunications services,

including interconnection, long distance and custom calling feature revenues are recognized monthly as services are

provided. Service revenues are primarily derived from providing access to or usage of the Company’s networks and

facilities. Due to varying customer billing cycle cut-off, the Company must estimate service revenues earned but not

yet billed at the end of each reporting period. Sales of communications products including customer premise equipment

and modems are recognized when products are delivered to and accepted by customers. Fees assessed to

communications customers for service activation are deferred upon service activation and recognized as service

revenue on a straight-line basis over the expected life of the customer relationship in accordance with authoritative

guidance on multiple element arrangements. Costs associated with activating such services, up to the related amount of

deferred revenue, are deferred and recognized as an operating expense over the same period.

F-25