eBay 2009 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2009 eBay annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

Revenue Recognition

We recognize revenue from services rendered when the following four revenue recognition criteria are met:

persuasive evidence of an arrangement exists, services have been rendered, the selling price is fixed or

determinable, and collectability is reasonably assured. We may enter into certain revenue transactions that

involve multiple element arrangements (arrangements with more than one deliverable). We also may enter into

arrangements to purchase goods and/or services from certain customers. As a result, significant contract

interpretation is sometimes required to determine appropriate accounting for these transactions including:

(1) whether an arrangement exists; (2) how the arrangement consideration should be allocated among potential

multiple arrangements; (3) when to recognize revenue on the deliverables; (4) whether all elements of the

arrangement have been delivered; (5) whether the arrangement should be reported gross (as a principal) versus

net (as an agent); (6) whether we receive a separately identifiable benefit from the purchase arrangements with

our customer for which we can reasonably estimate fair value; and (7) whether the arrangement would be

characterized as revenue or reimbursement of costs incurred. Changes in judgments on these assumptions and

estimates could impact the timing or amount of revenue recognition.

Goodwill and Intangible Assets

The purchase price of an acquired company is allocated between intangible assets and the net tangible assets

of the acquired business with the residual of the purchase price recorded as goodwill. The determination of the

value of the intangible assets acquired involves certain judgments and estimates. These judgments can include,

but are not limited to, the cash flows that an asset is expected to generate in the future and the appropriate

weighted average cost of capital.

At December 31, 2009, our goodwill totaled $6.1 billion and our identifiable intangible assets, net totaled

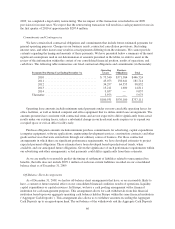

$767.8 million. We assess the impairment of goodwill of our reporting units annually, or more often if events or

changes in circumstances indicate that the carrying value may not be recoverable. This assessment is based upon

a discounted cash flow analysis and analysis of our market capitalization. The estimate of cash flow is based

upon, among other things, certain assumptions about expected future operating performance and an appropriate

discount rate determined by our management. Our estimates of discounted cash flows may differ from actual

cash flows due to, among other things, economic conditions, changes to our business model or changes in

operating performance. Additionally, certain estimates of discounted cash flows involve businesses with limited

financial history and developing revenue models, which increase the risk of differences between the projected

and actual performance. Significant differences between these estimates and actual cash flows could materially

affect our future financial results. These factors increase the risk of differences between projected and actual

performance that could impact future estimates of fair value of all reporting units. We conducted our annual

impairment test of goodwill as of August 31, 2008 and 2009. As a result of this test we determined that no

adjustment to the carrying value of goodwill for any reportable units was required. As a result our annual

impairment test of goodwill as of August 31, 2007, we concluded that the carrying amount of our

Communications reporting unit exceeded its fair value and recorded an impairment loss of approximately

$1.4 billion during the year ended December 31, 2007. The impairment charge includes the impact of the earn

out settlement payment with certain former shareholders of Skype and was determined by comparing the

carrying value of goodwill in our Communications reporting unit with the implied fair value of the goodwill. See

“Note 5 — Goodwill and Intangible Assets” to the consolidated financial statements included in this report. As of

December 31, 2009, we determined that no events or circumstances from August 31, 2009 through December 31,

2009 indicate that a further assessment was necessary.

Stock-Based Compensation

We measure and recognize stock-based compensation expense based on the fair value measurement for all

share-based payment awards made to our employees and directors, including employee stock options, employee

stock purchases and restricted stock awards over the service period for awards expected to vest. Stock-based

70