eBay 2015 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2015 eBay annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

we are unable to repay those borrowings from other sources when they become due. As a result, at December 31, 2015,

$500 million of borrowing capacity was available for other purposes permitted by the credit agreement.

Loans under the credit agreement bear interest at either (i) the London Interbank Offered Rate (“LIBOR”)

plus a margin (based on our public debt credit ratings) ranging from 0.875 percent to 1.5 percent or (ii) a formula

based on the agent bank’s prime rate, the federal funds effective rate plus 0.5 percent or LIBOR plus 1.0 percent,

plus a margin (based on our public debt credit ratings) ranging from 0.0 percent to 0.5 percent. The credit

agreement will terminate and all amounts owing thereunder will be due and payable on November 9, 2020,

unless (a) the commitments are terminated earlier, either at our request or, if an event of default occurs, by the

lenders (or automatically in the case of certain bankruptcy-related events of default), or (b) the maturity date is

extended upon our request, subject to the agreement of the lenders. The credit agreement contains customary

representations, warranties, affirmative and negative covenants, including financial covenants, events of default

and indemnification provisions in favor of the banks. The negative covenants include restrictions regarding the

incurrence of liens and subsidiary indebtedness, in each case, subject to certain exceptions. The financial

covenants require us to meet a quarterly financial test with respect to a minimum consolidated interest coverage

ratio and a maximum consolidated leverage ratio.

We were in compliance with all covenants in our outstanding debt instruments for the period ended

December 31, 2015.

Credit Ratings

Our credit ratings were downgraded as a result of the Distribution. As of January 1, 2014, our long-term

debt and short-term funding were rated investment grade by Standard and Poor’s Financial Services, LLC (long-

term rated A, short-term rated A-1, with a stable outlook), Moody’s Investor Service (long-term rated A2, short-

term rated P-1, with a stable outlook), and Fitch Ratings, Inc. (long-term rated A, short-term rated F-1, with a

stable outlook). All of these credit rating agencies lowered their ratings in connection with the Distribution,

which occurred on July 17, 2015. Since July 20, 2015, we have been rated investment grade by Standard and

Poor’s Financial Services, LLC (long-term rated BBB+, short-term rated A-2, with a stable outlook), Moody’s

Investor Service (long-term rated Baa1, short-term rated P-2, with a stable outlook), and Fitch Ratings, Inc.

(long-term rated BBB, short-term rated F-2, with a stable outlook). We disclose these ratings to enhance the

understanding of our sources of liquidity and the effects of these ratings on our costs of funds. Our borrowing

costs depend, in part, on our credit ratings and any further actions taken by these credit rating agencies to lower

our credit ratings, as described above, will likely increase our borrowing costs.

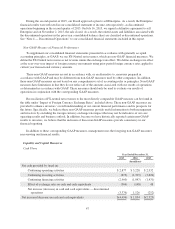

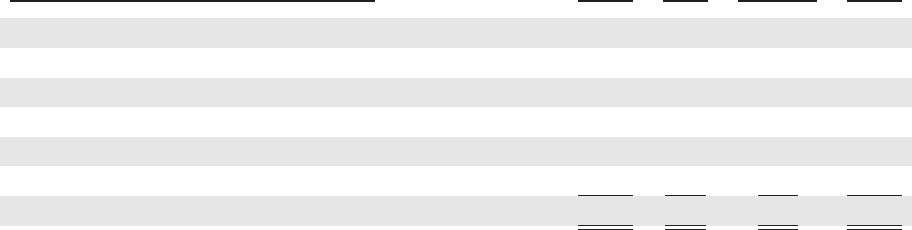

Commitments and Contingencies

We have certain fixed contractual obligations and commitments that include future estimated payments for

general operating purposes. Changes in our business needs, contractual cancellation provisions, fluctuating

interest rates, and other factors may result in actual payments differing from the estimates. We cannot provide

certainty regarding the timing and amounts of these payments. The following table summarizes our fixed

contractual obligations and commitments:

Payments Due During the Year Ending December 31, Debt Leases

Purchase

Obligations Total

(In millions)

2016 $ 164 $ 55 $175 $ 394

2017 1,613 52 83 1,748

2018 148 35 64 247

2019 1,697 30 13 1,740

2020 516 25 5 546

Thereafter 4,191 25 — 4,216

$8,329 $222 $340 $8,891

51