APC 2005 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2005 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

80

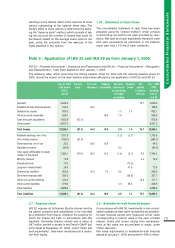

2.3 - Derivative instruments and

hedge accounting

IAS 39 requires all derivative instruments to be recog-

nized in the balance sheet and measured at fair value,

whereas in the French GAAP accounts, these instru-

ments were generally carried off-balance sheet. The

treatment of gains and losses arising from remeasure-

ment at fair value depends on whether or not the

instruments qualify for hedge accounting under IAS 39.

Currency instruments qualified as cash flow hedges

under IAS 39 have been recognized in the balance

sheet under "Other receivables" at their fair value of

12.2 million, leading to an adjustment of equity in the

same amount, recorded under "Other reserves".

Hedges of future metal purchases qualified as cash

flow hedges under IAS 39 have been recognized in

the balance sheet under "Other receivables" at their

fair value of 7.7 million, leading to an adjustment of

equity in the same amount, recorded under "Other

reserves".

2.4 - Derivative instruments

not qualifying for hedge accounting

Derivative instruments not qualifying for hedge

accounting under IAS 39 have been recognized at fair

value in the balance sheet, in assets for 1.8 million

and in liabilities for 3.3 million, leading to correspon-

ding adjustments to equity. The instruments con-

cerned consist mainly of interest rate hedges on intra-

group debt.

2.5 - Perpetual bonds

In the French GAAP accounts, the 1991 perpetual

bonds are recorded in debt at their nominal value,

while the related interest rate swaps are carried off-

balance sheet.

In accordance with interpretation SIC 12 and IAS 39,

the Group has consolidated the special purpose enti-

ty that holds the perpetual bonds. The swaps taken out

by the special purpose entity in connection with the

perpetual bonds have been measured at fair value.

Interest rate swaps on the perpetual bonds taken out

directly by the Group, which do not qualify for hedge

accounting, are recognized in the balance sheet at fair

value, with gains and losses arising from remeasure-

ment at fair value recognized in "Other financial

income and expense".

At January 1, 2005, the value of the perpetual bonds

and the fair value of the swaps taken out by the spe-

cial purpose entity was 21 million, and the fair value

of the swaps entered into directly by the Group was

56.4 million.

2.6 - Put options

granted to minority shareholders

The Group has given commitments to buy out the

minority shareholders of consolidated subsidiaries

(put options). These commitments were reported off-

balance sheet in the French GAAP accounts at

December 31, 2004.

IAS 32 requires their recognition in debt, at fair value,

which corresponds to the option strike price. As

explained in note 1.21, in the absence of established

accounting practice and pending publication of an

interpretation by the IFRIC specifying the accounting

treatment of the related adjustment, the difference

between the fair value of the put options and the under-

lying minority interests has been posted to goodwill.

Dec. 31, 2005 Dec. 31, 2004 Dec. 31, 2003

(Number of companies)

France International France International France International

Parent company and fully consolidated subsidiaries 69 366 65 328 52 266

Proportionally consolidated companies - - - - 1 1

Companies accounted for by the equity method 1 3 2 5 2 7

Sub-total by region 70 369 67 333 55 274

Total 439 400 329

Acquisitions

On April 14, 2005, Schneider Electric acquired all out-

standing shares in Canada’s Power Measurement Inc.,

a leader in the design, production and marketing of

energy management systems. Power Measurement

Inc. has been fully consolidated since April 14, 2005.

On May 30, 2005, Schneider Electric acquired 50.9% of

the outstanding shares of ELAU Administration GmbH,

thereby raising its interest from 41.9% to 100%.

ELAU was accounted for by the equity method until

May 31, 2005 and has been fully consolidated since

June 1, 2005.

Note 3 - Changes in the scope of consolidation

3.1 - Additions and removals

The consolidated financial statements for the year ended December 31, 2005 include the accounts of the com-

panies listed in note 30. The scope of consolidation at December 31, 2005, 2004 and 2003 is summarized as

follows: