American Express 2011 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2011 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

|

|

AMERICAN EXPRESS COMPANY

2011 FINANCIAL REVIEW

non-accrual in the Company’s TDR disclosures), (ii) reducing

the outstanding balance (in the event of a settlement),

(iii) suspending delinquency fees until the cardmember exits the

TDR program, and (iv) placing the cardmember on a fixed

payment plan not exceeding 60 months. Upon entering the

modification program, the cardmember’s ability to make future

purchases is either cancelled, or in certain cases suspended until

the cardmember successfully exits the TDR program. In

accordance with the modification agreement with the

cardmember, loans with modified terms will revert back to their

original contractual terms (including their contractual interest

rate) when they exit the TDR program, either (i) when all

payments have been made in accordance with the modification

agreement or (ii) in the event that a payment is not made in

accordance with the modification agreement and the

cardmember defaults out of the program. In either case, in

accordance with its normal policy, the Company establishes a

reserve for cardmember interest charges that it believes will not

be collected.

The performance of a loan or a receivable modified as a TDR is

closely monitored to understand its impact on the Company’s

reserve for losses. Though the ultimate success of these

modification programs remains uncertain, the Company believes

the programs improve the cumulative loss performance of such

loans and receivables.

Reserves for cardmember loans and receivables modified as

TDRs are determined by the difference between the cash flows

expected to be received from the cardmember, taking into

consideration the probability of subsequent defaults, discounted

at the original effective interest rates, and the carrying value of

the cardmember loan or receivable balance. The Company

determines the original effective interest rate as the interest rate

in effect prior to the imposition of any penalty rate. All changes

in the impairment measurement, including the component due

to the passage of time are included in the provision for losses

within the Consolidated Statements of Income.

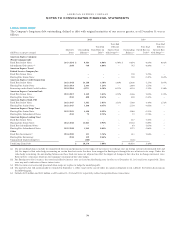

The following tables provide additional information with respect to the Company’s impaired cardmember loans and receivables as of

December 31:

(Millions)

Loans over

90 Days Past

Due &

Accruing

Interest(a)

Non-

Accrual

Loans(b)

Loans &

Receivables

Modified

as a TDR(c)(d)

Total

Impaired

Loans &

Receivables

Unpaid

Principal

Balance(e)

Allowance

for TDRs(f)

2011

U.S. Card Services – Cardmember Loans $ 64 $ 529 $ 736 $ 1,329 $ 1,268 $ 174

International Card Services – Cardmember Loans 67 6 8 81 80 2

U.S. Card Services – Cardmember Receivables – – 174 174 165 118

Total(g) $ 131 $ 535 $ 918 $ 1,584 $ 1,513 $ 294

(Millions)

Loans over

90 Days Past

Due &

Accruing

Interest(a)

Non-

Accrual

Loans(b)

Loans &

Receivables

Modified

as a TDR(c)

Total

Impaired

Loans &

Receivables

Unpaid

Principal

Balance(e)

Allowance

for TDRs(f)

2010

U.S. Card Services – Cardmember Loans $ 90 $ 628 $ 1,076 $ 1,794 $ 1,704 $ 274

International Card Services – Cardmember Loans 95 8 11 114 112 5

U.S. Card Services – Cardmember Receivables – – 114 114 109 63

Total(g) $ 185 $ 636 $ 1,201 $ 2,022 $ 1,925 $ 342

(a) The Company’s policy is generally to accrue interest through the date of charge-off (at 180 days past due). The Company establishes reserves for interest that the

Company believes will not be collected.

(b) Non-accrual loans not in modification programs include certain cardmember loans placed with outside collection agencies for which the Company has ceased

accruing interest. The Company’s policy is not to resume the accrual of interest on these loans. Payments received are applied against the recorded loan balance.

Interest income is recognized on a cash basis for any payments received after the loan balance has been paid in full.

(c) The total loans and receivables modified as a TDR include $410 million and $655 million that are non-accrual and $4 million and $7 million that are pastdue90days

and still accruing interest as of December 31, 2011 and 2010, respectively. These amounts are excluded from the previous two columns.

(d) During the third quarter of 2011, the Company reassessed all cardmember loans and receivables modifications that occurred on or after January 1, 2011, to determine

whether any such modifications met the definition of a TDR under new GAAP effective July 1, 2011. As a result, in the third quarter of 2011 the Company began

classifying its short-term settlement programs as TDRs which had an outstanding balance of $5.8 million and associated reserves for losses of $3.7 million.

(e) Unpaid principal balance consists of cardmember charges billed and excludes other amounts charged directly by the Company such as interest and fees.

(f) Represents the reserve for losses for TDRs, which are evaluated separately for impairment. The Company records a reserve for losses for all impaired loans. Refer to

Cardmember Loans Evaluated Separately and Collectively for Impairment in Note 5 for further discussion of the reserve for losses on loans over 90 days past due and

accruing interest and non-accrual loans, which are evaluated collectively for impairment.

(g) These disclosures are not significant for cardmember receivables in ICS and GCS.

68