American Express 2011 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2011 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

|

|

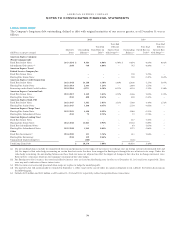

AMERICAN EXPRESS COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The following table provides information with respect to the

Company’s interest income recognized and average balances of

impaired cardmember loans and receivables for the years ended

December 31:

2011

(Millions)

Interest

Income

Recognized

Average

Balance

U.S. Card Services – Cardmember Loans $ 67 $ 1,498

International Card Services – Cardmember Loans 26 98

U.S. Card Services – Cardmember Receivables – 145

Total(a) $ 93 $ 1,741

2010

(Millions)

Interest

Income

Recognized

Average

Balance

U.S. Card Services – Cardmember Loans $ 101 $ 2,256

International Card Services – Cardmember Loans 30 142

U.S. Card Services – Cardmember Receivables – 110

Total(a) $ 131 $ 2,508

(a) These disclosures are not significant for cardmember receivables in ICS and

GCS.

CARDMEMBER LOANS AND RECEIVABLES MODIFIED

AS TDRS

The following table provides additional information with respect

to the cardmember loans and receivables modified as TDRs

during the year ended December 31, 2011:

(Accounts in thousands,

Dollars in millions)

Number of

Accounts

Aggregated

Pre-

Modification

Outstanding

Balances(a)(b)

Aggregated

Post-

Modification

Outstanding

Balances(a)(b)

Troubled Debt

Restructurings:

U.S. Card Services –

Cardmember Loans 147 $ 1,110 $ 1,064

U.S. Card Services –

Cardmember Receivables 50 402 388

Total(c) 197 $ 1,512 $ 1,452

(a) The outstanding balance includes principal and accrued interest.

(b) The difference between the pre- and post-modification outstanding balances

is solely attributable to amounts charged off for cardmember loans and

receivables being resolved through the Company’s short-term settlement

programs.

(c) These disclosures are not significant for cardmember loans modifications in

ICS.

As described previously, the Company’s cardmember loans and

receivables modification programs may include (i) reducing the

interest rate, (ii) reducing the outstanding balance,

(iii) suspending delinquency fees and (iv) placing the

cardmember on a fixed payment plan not exceeding 60 months.

Upon entering the modification program, the cardmember’s

ability to make future purchases is either cancelled, or in certain

cases suspended until the cardmember successfully exits the TDR

program.

The Company has evaluated the primary financial effects of the

impact of the changes to an account upon modification as

follows:

폷Interest Rate Reduction: For the year ended December 31,

2011, the average interest rate reduction was 11 percentage

points, which did not have a significant impact on interest and

fees on loans in the Consolidated Statements of Income. The

Company does not offer interest rate reduction programs for

USCS cardmember receivables as these receivables are

non-interest bearing.

폷Outstanding Balance Reduction: The table above presents the

financial effects on the Company as a result of reducing the

outstanding balance for Short-Term Settlement Programs. The

difference between the pre- and post-modification outstanding

balances represents the amount that either has been written off

or will be written off upon successful completion of the

settlement program.

폷Payment Term Extension: For the year ended December 31,

2011, the average payment term extension was approximately

15 months for USCS cardmember receivables. For USCS

cardmember loans, there have been no extension of payment

terms.

The following table provides information with respect to the

cardmember loans and receivables modified as TDRs on which

there was a default within 12 months of modification during the

year ended December 31, 2011. A cardmember will default from

a modification program after between one and up to three

consecutive missed payments, depending on the terms of the

modification program.

(Accounts in thousands,

Dollars in millions)

Number of

Accounts

Aggregated

Outstanding

Balances

Upon Default(a)

Troubled Debt Restructurings

That Subsequently Defaulted:

U.S. Card Services –

Cardmember Loans 46 $ 343

U.S. Card Services –

Cardmember Receivables 645

Total(b) 52 $ 388

(a) The outstanding balance includes principal and accrued interest.

(b) During the periods presented, the ICS cardmember loan

modifications on which there was a default from the modification

program within 12 months of modification were not significant.

69