American Express 2011 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2011 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

|

|

AMERICAN EXPRESS COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 5

RESERVES FOR LOSSES

Reserves for losses relating to cardmember loans and receivables

represent management’s best estimate of the losses inherent in

the Company’s outstanding portfolio of loans and receivables.

Management’s evaluation process requires certain estimates and

judgments.

Reserves for these losses are primarily based upon statistical

models that analyze portfolio performance and reflect

management’s judgment regarding overall reserve adequacy. The

models take into account several factors, including loss

migration rates and average losses and recoveries over an

appropriate historical period. Management considers whether to

adjust the models for specific factors such as increased risk in

certain portfolios, impact of risk management initiatives on

portfolio performance and concentration of credit risk based on

factors such as vintage, industry or geographic regions. In

addition, management may increase or decrease the reserves for

losses on cardmember loans for other external environmental

factors including leading economic and market indicators such

as the unemployment rate, home price indices, Gross Domestic

Product (GDP), non-farm payrolls, personal consumption

expenditures index, consumer confidence index, bankruptcy

filings and the legal and regulatory environment. Generally, due

to the short-term nature of cardmember receivables, the impact

of additional external factors on the losses inherent within the

cardmember receivable portfolio is not significant. As part of this

evaluation process, management also considers various reserve

coverage metrics, such as reserves as a percentage of past due

amounts, reserves as a percentage of cardmember receivables or

loans and net write-off coverage.

Cardmember loans and receivables balances are written off

when management deems amounts to be uncollectible, which is

generally determined by the number of days past due and is

typically no later than 180 days. Cardmember loans and

receivables in bankruptcy or owed by deceased individuals are

written off upon notification. Recoveries are recognized on a

cash basis.

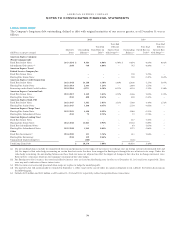

Changes in Cardmember Receivables Reserve for

Losses

The following table presents changes in the cardmember

receivables reserve for losses for the years ended December 31:

(Millions) 2011 2010 2009

Balance, January 1 $ 386 $ 546 $ 810

Additions:

Cardmember receivables provisions(a) 603 439 773

Cardmember receivables provisions –

other(b) 167 156 84

Total provision 770 595 857

Deductions:

Cardmember receivables net write-

offs(c)(d) (560) (598) (1,131)

Cardmember receivables – other(e) (158) (157) 10

Balance, December 31 $ 438 $ 386 $ 546

(a) Represents loss provisions for cardmember receivables consisting of

principal (resulting from authorized transactions) and fee reserve

components.

(b) Primarily represents loss provisions for cardmember receivables resulting

from unauthorized transactions.

(c) Represents write-offs consisting of principal (resulting from authorized

transactions) and fee components, less recoveries of $349 million, $357

million and $349 million for 2011, 2010 and 2009, respectively. For the year

ended December 31, 2009, these amounts also include net write-offs for

cardmember receivables resulting from unauthorized transactions.

(d) Through December 31, 2009, cardmember receivables in the ICS and GCS

segments were written off when 360 days past billing or earlier. During the

first quarter of 2010, consistent with applicable bank regulatory guidance,

the Company modified its methodology to write off cardmember receivables

in the ICS and GCS segments when 180 days past due or earlier. Therefore,

net write-offs for cardmember receivables for the first quarter of 2010

included approximately $108 million resulting from this change in write-off

methodology. The impact of this change to the provision for charge card

losses was not material.

(e) For the years ended December 31, 2011 and 2010, these amounts include net

write-offs related to unauthorized transactions and, for all periods, foreign

currency translation adjustments.

70