Best Buy 2013 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2013 Best Buy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

47

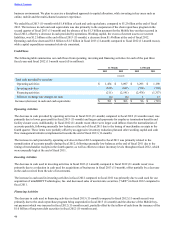

The increase in cash used in financing activities in fiscal 2012 compared to fiscal 2011 was primarily the result of $1.3 billion

of cash we used for the Mobile buy-out, an increase in cash used to repurchase our common stock and the repurchase of

convertible debentures during fiscal 2012, partially offset by the issuance of $1.0 billion of long-term debt securities in the first

quarter of fiscal 2012.

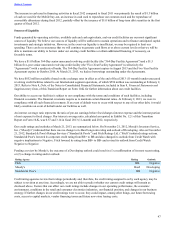

Sources of Liquidity

Funds generated by operating activities, available cash and cash equivalents, and our credit facilities are our most significant

sources of liquidity. We believe our sources of liquidity will be sufficient to sustain operations and to finance anticipated capital

investments and strategic initiatives. However, in the event our liquidity is insufficient, we may be required to limit our

spending. There can be no assurance that we will continue to generate cash flows at or above current levels or that we will be

able to maintain our ability to borrow under our existing credit facilities or obtain additional financing, if necessary, on

favorable terms.

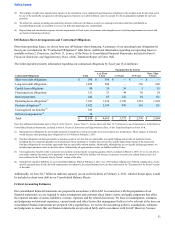

We have a $1.0 billion 364-Day senior unsecured revolving credit facility (the "364-Day Facility Agreement") and a $1.5

billion five-year senior unsecured revolving credit facility (the "Five-Year Facility Agreement") (collectively the

"Agreements") with a syndicate of banks. The 364-Day Facility Agreement expires in August 2013 and the Five-Year Facility

Agreement expires in October 2016. At March 21, 2013, we had no borrowings outstanding under the Agreements.

We have $852 million available (based on the exchange rates in effect as of the end of fiscal 2013 (11-month)) under unsecured

revolving credit facilities related to our International segment operations, of which $596 million was outstanding at February 2,

2013. Refer to Note 8, Debt, of the Notes to Consolidated Financial Statements, included in Item 8, Financial Statements and

Supplementary Data, of this Transition Report on Form 10-K for further information about our credit facilities.

Our ability to access our facilities is subject to our compliance with the terms and conditions of such facilities, including

financial covenants. The financial covenants require us to maintain certain financial ratios. At February 2, 2013, we were in

compliance with all such financial covenants. If an event of default were to occur with respect to any of our other debt, it would

likely constitute an event of default under our facilities as well.

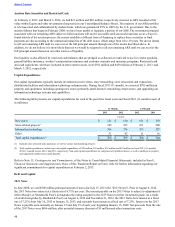

An interest coverage ratio represents the ratio of pre-tax earnings before fixed charges (interest expense and the interest portion

of rent expense) to fixed charges. Our interest coverage ratio, calculated as reported in Exhibit No. 12.1 of this Transition

Report on Form 10-K, was 0.57 and 3.14 in fiscal 2013 (11-month) and 2012, respectively.

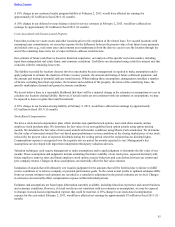

Our credit ratings and outlooks at March 21, 2013, are summarized below. On November 21, 2012, Moody's Investors Service,

Inc. (“Moody's”) indicated that there was no change to its Baa2 long-term rating and outlook of Developing. Also on November

21, 2012, Standard & Poor's Ratings Services (“Standard & Poor's”) and Fitch Ratings Ltd. (“Fitch”) initiated ratings actions.

Standard & Poor's lowered its corporate credit rating from BB+ to BB and also changed its outlook from Credit Watch with

negative implications to Negative. Fitch lowered its rating from BB+ to BB- and revised its outlook from Credit Watch

Negative to Negative.

Pending a review by Moody's, the outcome of a Developing outlook could result in (1) a reaffirmation of its most recent rating,

or (2) a change in rating and/or outlook.

Rating Agency Rating Outlook

Fitch BB- Negative

Moody's Baa2 Developing

Standard & Poor's BB Negative

Credit rating agencies review their ratings periodically and, therefore, the credit rating assigned to us by each agency may be

subject to revision at any time. Accordingly, we are not able to predict whether our current credit ratings will remain as

disclosed above. Factors that can affect our credit ratings include changes in our operating performance, the economic

environment, conditions in the retail and consumer electronics industries, our financial position, and changes in our business

strategy. If further changes in our credit ratings were to occur, they could impact, among other things, our future borrowing

costs, access to capital markets, vendor financing terms and future new-store leasing costs.

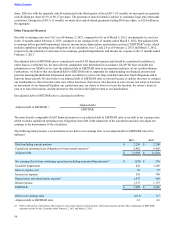

Table of Contents