Charter 2009 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2009 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

|

|

23

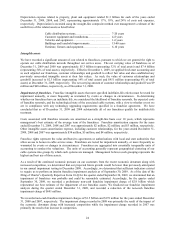

While we believe our existing capitalization policies are appropriate, a significant change in the nature or extent of

our system activities could affect management’ s judgment about the extent to which we should capitalize direct

labor or overhead in the future. We monitor the appropriateness of our capitalization policies, and perform updates

to our internal studies on an ongoing basis to determine whether facts or circumstances warrant a change to our

capitalization policies. We capitalized internal direct labor and overhead of $199 million, $199 million, and $194

million, respectively, for the years ended December 31, 2009, 2008, and 2007.

Impairment. We evaluate the recoverability of our property, plant and equipment upon the occurrence of events or

changes in circumstances indicating that the carrying amount of an asset may not be recoverable. Such events or

changes in circumstances could include such factors as the impairment of our indefinite-life franchises, changes in

technological advances, fluctuations in the fair value of such assets, adverse changes in relationships with local

franchise authorities, adverse changes in market conditions, or a deterioration of current or expected future operating

results. A long-lived asset is deemed impaired when the carrying amount of the asset exceeds the projected

undiscounted future cash flows associated with the asset. No impairments of long-lived assets to be held and used

were recorded in the years ended December 31, 2009, 2008 and 2007. However, approximately $56 million of

impairment on assets held for sale were recorded for the year ended December 31, 2007.

Fresh start accounting. As discussed above, effective December 1, 2009, we applied fresh start accounting

resulting in an approximately $2.0 billion increase to total property, plant and equipment. The cost approach was

the primary method used to establish fair value for our property, plant and equipment in connection with the

application of fresh start accounting. The cost approach considers the amount required to replace an asset by

constructing or purchasing a new asset with similar utility, then adjusts the value in consideration of all forms of

depreciation as of the appraisal date as follows.

• Physical depreciation — the loss in value or usefulness attributable solely to use of the asset and physical

causes such as wear and tear and exposure to the elements.

• Functional obsolescence — a loss in value is due to factors inherent in the asset itself and due to changes in

technology, design or process resulting in inadequacy, overcapacity, lack of functional utility or excess

operating costs.

• Economic obsolescence — loss in value by unfavorable external conditions such as economics of the

industry or geographic area, or change in ordinances.

The cost approach relies on management’ s assumptions regarding current material and labor costs required to

rebuild and repurchase significant components of our property, plant and equipment along with assumptions

regarding the age and estimated useful lives of our property, plant and equipment. For illustrative purposes only, the

impact of a one-year change in our estimated remaining useful life (holding all other assumptions unchanged) to the

fair value of our property, plant and equipment would be approximately $800 million.

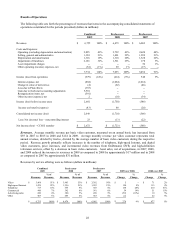

Useful lives of property, plant and equipment. We evaluate the appropriateness of estimated useful lives assigned

to our property, plant and equipment, based on annual analyses of such useful lives, and revise such lives to the

extent warranted by changing facts and circumstances. Any changes in estimated useful lives as a result of these

analyses are reflected prospectively beginning in the period in which the study is completed. In connection with the

application of fresh start accounting as of December 1, 2009, management made assumptions regarding remaining

useful lives of our existing property, plant and equipment and evaluated the appropriateness of useful lives to be

applied to future additions of property, plant and equipment. The effect of a one-year decrease in the weighted

average remaining useful life of our property, plant and equipment as of December 31, 2009 would be an increase in

annual depreciation expense of approximately $196 million. The effect of a one-year increase in the weighted

average remaining useful life of our property, plant and equipment as of December 31, 2009 would be a decrease in

annual depreciation expense of approximately $222 million.