Charter 2009 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2009 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

|

|

CCH II, LLC AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2009, 2008, AND 2007

(dollars in millions, except where indicated)

F-20

historical operating performance adjusted for current and expected competitive and economic factors surrounding

the cable industry. The estimates and assumptions made in the Company’ s valuations are inherently subject to

significant uncertainties, many of which are beyond its control, and there is no assurance that these results can be

achieved. The primary assumptions for which there is a reasonable possibility of the occurrence of a variation that

would significantly affect the measurement value include the assumptions regarding revenue growth, programming

expense growth rates, the amount and timing of capital expenditures and the discount rate utilized. The assumptions

used are consistent with current internal forecasts, some of which differ from the assumptions used for the annual

impairment testing in December 2008 as a result of the economic and competitive environment discussed

previously. The change in assumptions reflects the lower than anticipated growth in revenues experienced during

2009 and the expected reduction of future cash flows as compared to those used in the December 2008 valuations.

Franchises, for valuation purposes, are defined as the future economic benefits of the right to solicit and service

potential customers (customer marketing rights), and the right to deploy and market new services, such as

interactivity and telephone, to potential customers (service marketing rights). Fair value is determined based on

estimated discrete discounted future cash flows using assumptions consistent with internal forecasts. The franchise

after-tax cash flow is calculated as the after-tax cash flow generated by the potential customers obtained (less the

anticipated customer churn), and the new services added to those customers in future periods. The sum of the

present value of the franchises' after-tax cash flow in years 1 through 10 and the continuing value of the after-tax

cash flow beyond year 10 yields the fair value of the franchises. Franchises increased $62 million as a result of the

application of fresh start accounting. Subsequent to finalization of the franchise impairment charge and fresh start

accounting, franchises are recorded at fair value of $5.3 billion. Franchises are expected to generate cash flows

indefinitely and as such will continue to be tested for impairment annually.

Customer relationships, for valuation purposes, represent the value of the business relationship with existing

customers (less the anticipated customer churn), and are calculated by projecting the discrete future after-tax cash

flows from these customers, including the right to deploy and market additional services to these customers. The

present value of these after-tax cash flows yields the fair value of the customer relationships. The Company

recorded $2.4 billion of customer relationships in connection with the application of fresh start accounting on the

Effective Date. Customer relationships will be amortized on an accelerated method over useful lives of 11-15 years

based on the period over which current customers are expected to generate cash flows.

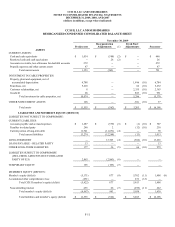

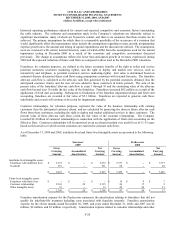

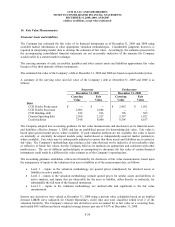

As of December 31, 2009 and 2008, indefinite-lived and finite-lived intangible assets are presented in the following

table:

Successor Predecessor

2009 2008

Gross

Net Gross Net

Carrying Accumulated Carrying Carrying Accumulated Carrying

Amount Amortization Amount Amount Amortization Amount

Indefinite-lived intangible assets:

Franchises with indefinite lives $ 5,272 $ -- $ 5,272 $ 7,377 $ -- $ 7,377

Goodwill 951 -- 951 68 -- 68

$ 6,223 $ -- $ 6,223 $ 7,445 $ -- $ 7,445

Finite-lived intangible assets:

Franchises with finite lives $ -- $ -- $ -- $ 16 $ 9 $ 7

Customer relationships 2,363 28 2,335 26 17 9

Other intangible assets 33 -- 33 45 24 21

$ 2,396 $ 28 $ 2,368 $ 87 $ 50 $ 37

Franchise amortization expense for the Predecessor represents the amortization relating to franchises that did not

qualify for indefinite-life treatment including costs associated with franchise renewals. Franchise amortization

expense for the eleven months ended November 30, 2009, and years ended December 31, 2008, and 2007 was $2

million, $2 million, and $3 million, respectively. Amortization expense related to customer relationships and other