Charter 2009 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2009 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90

|

|

CCH II, LLC AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2009, 2008, AND 2007

(dollars in millions, except where indicated)

F-41

which were previously classified as minority interest. On the Effective Date, Mr. Allen’ s 5.6% preferred

membership interest was transferred to Charter.

In June 2009, the FASB issued guidance included in ASC 105-10, Generally Accepted Accounting Principles –

Overall (“ASC 105-10”). ASC 105-10 is intended to be the source of GAAP and reporting standards as issued by

the FASB. Its primary purpose is to improve clarity and use of existing standards by grouping authoritative literature

under common topics. ASC 105-10 is effective for financial statements issued for interim and annual periods ending

after September 15, 2009. The Company adopted ASC 105-10 effective September 30, 2009. The Codification

does not change or alter existing GAAP and there was no impact on the Company’ s financial statements.

In August 2009, the FASB issued guidance included in ASC 820-10-65 which states companies determining the fair

value of a liability may use the perspective of an investor that holds the related obligation as an asset. This guidance

included in ASC 820-10-65 addresses practice difficulties caused by the tension between fair-value measurements

based on the price that would be paid to transfer a liability to a new obligor and contractual or legal requirements

that prevent such transfers from taking place. This guidance included in ASC 820-10-65 is effective for interim and

annual periods beginning after August 27, 2009, and applies to all fair-value measurements of liabilities required by

GAAP. No new fair-value measurements are required by this guidance. The Company adopted this guidance

included in ASC 820-10-65 effective October 1, 2009. The adoption of this guidance included in ASC 820-10-65

did not have a material impact on the Company’ s financial statements.

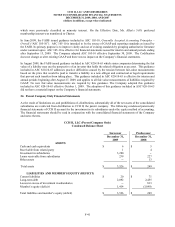

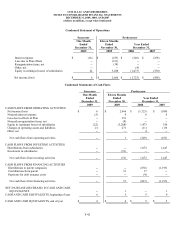

24. Parent Company Only Financial Statements

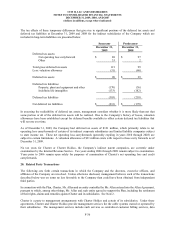

As the result of limitations on, and prohibitions of, distributions, substantially all of the net assets of the consolidated

subsidiaries are restricted from distribution to CCH II, the parent company. The following condensed parent-only

financial statements of CCH II account for the investment in its subsidiaries under the equity method of accounting.

The financial statements should be read in conjunction with the consolidated financial statements of the Company

and notes thereto.

CCH II, LLC (Parent Company Only)

Condensed Balance Sheet

Successor Predecessor

December 31,

2009

December 31,

2008

ASSETS

Cash and cash equivalents $ 6 $ 5

Receivable from related party 1 4

Investment in subsidiaries 3,280 --

Loans receivable from subsidiaries 239 227

Other assets -- 13

Total assets $ 3,526 $ 249

LIABILITIES AND MEMBER’S EQUITY (DEFICIT)

Current liabilities $ 20 $ 71

Long-term debt 2,092 2,455

Losses in excess of investment in subsidiaries -- 813

Member’ s equity (deficit) 1,414 (3,090)

Total liabilities and member’ s equity (deficit) $ 3,526 $ 249