Charter 2009 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2009 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

|

|

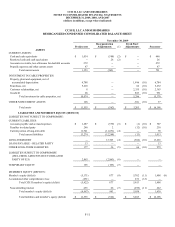

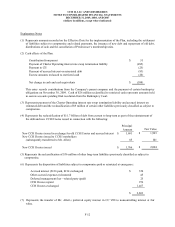

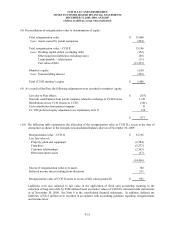

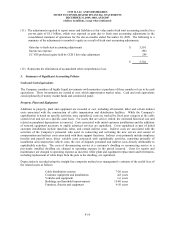

CCH II, LLC AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2009, 2008, AND 2007

(dollars in millions, except where indicated)

F-9

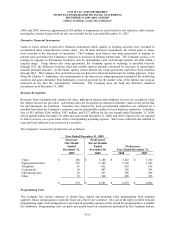

Fresh start accounting provides, among other things, for a determination of the value to be assigned to the equity of

the emerging company as of a date selected for financial reporting purposes. In the disclosure statement related to

the Plan, the reorganization value of Charter was set forth as approximately $14.1 billion to $16.6 billion, with a

midpoint estimate of $15.4 billion. Reorganization value represents the amount of resources available for the

satisfaction of post-petition liabilities and allowed claims, as negotiated between the Debtors and their creditors.

Reorganization value, along with other terms of the Plan, was determined after extensive arms-length negotiations

with the Company’ s and its parent companies’ creditors. The value was based upon expected future cash flows of

the business after emergence from Chapter 11, discounted at rates reflecting perceived business and financial risks

(the discounted cash flows). This valuation and a valuation using market value multiples for peer companies were

blended to arrive at the reorganization value. Reorganization value is intended to approximate the amount a willing

buyer would pay for the assets of Charter immediately after the reorganization.

The valuation analysis relied predominantly on the discounted cash flows (“DCF”) analysis and the comparable

company analysis. While a precedent transaction analysis was performed, the reliance on such methodology for

purposes of determining the reorganization value was minimal. The precedent transaction analysis is based on the

enterprise values of companies involved in public merger and acquisition transactions that have operating and

financial characteristics similar to Charter. Due to factors including, (i) the market environment is not identical for

transactions occurring at different periods, and (ii) circumstances pertaining to the financial position of the company

may have an impact on the resulting purchase price, less reliance is applied to the precedent transaction analysis. A

more detailed explanation of the DCF analysis and comparable company analysis is discussed below.

The basis for the DCF analysis was the projections published in the Plan. These five-year projections were based on

management’ s assumptions including among others, penetration rates for basic and digital video, high-speed

Internet, and telephone; revenue growth rates; operating margins; and capital expenditures. The assumptions are

derived based on Charter’ s and its peers’ historical operating performance adjusted for current and expected

competitive and economic factors surrounding the cable industry. The DCF analysis was completed using discount

rates ranging from 10.5% to 11.5% based on Charter’ s cost of equity and after-tax cost of debt and perpetuity

growth rates of 2.5% - 3.5%. The reorganization value and the resulting equity value are highly dependent on the

achievement of the future financial results contemplated in the projections that were published in the Plan. The

estimates and assumptions made in the valuation are inherently subject to significant uncertainties, many of which

are beyond its control, and there is no assurance that these results can be achieved. The primary assumptions for

which there is a reasonable possibility of the occurrence of a variation that would have significantly affected the

reorganization value include the assumptions regarding revenue growth, programming expense growth rates, the

amount and timing of capital expenditures and the discount rate utilized.

The valuation also utilized a comparable companies methodology which identified a group of publicly traded

companies whose financial and operating characteristics were similar to those of Charter as a whole; examined the

trading prices for the equity securities of such companies in the public markets; added the aggregate amount of

outstanding net debt for such companies (at book value and at current market values); and noncontrolling interest

less the market value of unconsolidated investments. A range of valuation multiples was then applied to the

projections to derive a range of implied enterprise values for Charter as a whole. The multiples ranged from 5.0 to

6.0 depending on the comparable company.

Based on conditions in the cable industry and general economic conditions, the mid-point of the range of valuations

was used to determine the reorganization value. Under fresh start accounting, this reorganization value, as adjusted

for assets owned by its parent companies, was allocated to the Company’ s assets based on their respective fair

values. The reorganization value, after adjustments for working capital, is reduced by the fair value of debt and

other noncurrent liabilities with the remainder representing the value to the member.

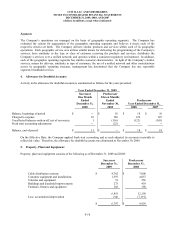

The significant assumptions related to the valuations of the Company’ s assets in connection with fresh start

accounting include the following:

Property, plant and equipment — Property, plant and equipment was valued at fair value of $6.8 billion as of

November 30, 2009. In establishing fair value for the vast majority of the Company’ s property, plant and

equipment, the cost approach was utilized. The cost approach considers the amount required to replace an asset by