Lowe's 1997 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 1997 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

|

|

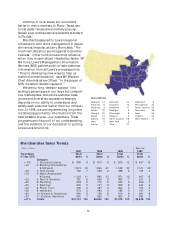

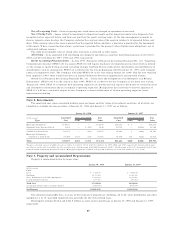

Interest costs as a percent of sales were 0.6% for 1997 and 1996, compared to 0.5% for 1995. Interest totaled $66

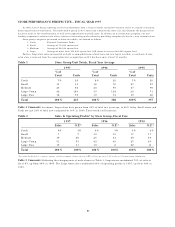

million in 1997, $49 million in 1996 and $38 million for 1995. Interest costs related to capital leases totaled $38.3,

$29.1 and $16.9 million for 1997, 1996 and 1995, respectively. See the discussion below on liquidity and capital re-

sources.

Effective income tax rates were 36.0%, 35.6% and 35.8% in 1997, 1996 and 1995, respectively. The higher rate in

1997 was primarily due to available tax credits not growing at the same rate as earnings and from expansion into states

with higher tax rates. The lower rate in 1996 was primarily due to utilization of available state net operating losses.

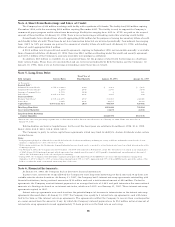

LIQUIDITY AND CAPITAL RESOURCES

Primary sources of liquidity are cash flows from operating activities and certain financing activities. Net cash pro-

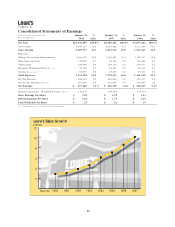

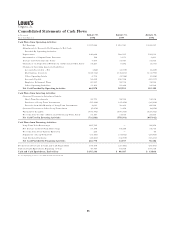

vided by operating activities was $664.9 million for 1997. This compared to $543.0 and $303.3 million for 1996 and

1995, respectively. The increases in net cash provided by operating activities for 1997 and 1996 are primarily related to

increased earnings and smaller increases in inventory net of accounts payable from year to year. An increase in other

operating liabilities also contributed to the 1996 increase in net cash provided by operations from 1995. Working capital

at January 30, 1998 was $660.3 million compared to $502.9 million at January 31, 1997.

Cash flows provided by financing activities were $221.8, $11.9 and $58.2 million in 1997, 1996 and 1995, respec-

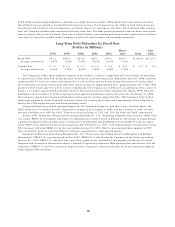

tively. The major cash components of financing activities in 1997 included issuance of $268 million aggregate principal

amount of Medium Term Notes (MTN’s) and $32.8 million of scheduled debt repayments. In 1996, financing activities

primarily included proceeds from $64 million in short-term borrowings and $17.7 million of scheduled debt repayments.

The major financing activity of 1996 was the noncash conversion of $284.7 million principal amount of 3% Convertible

Subordinated Notes into common stock. In 1995, the Company issued $100 million aggregate principal amount of 6.375%

Senior Notes and had scheduled debt repayments of $25.1 million. The ratio of long-term debt to equity plus long-term debt

was 28.7%, 25.7% and 34.3% for 1997, 1996 and 1995, respectively. The increase in the debt to equity ratio in 1997 was

primarily due to the issuance of the $268 million in MTN’s mentioned earlier. The decrease in 1996 was primarily a

result of the conversion of debt to equity.

During 1997, the Company registered $350 million of MTN’s from a shelf registration filed in 1996. At January 30,

1998, the Company had sold $268 million aggregate principal of MTN’s to investors with final maturities ranging from

September 1, 2007 to May 15, 2037, at interest rates ranging from 6.07% to 7.61%. Approximately 37% of these

MTN’s may be put to the Company at the option of the holder on either the tenth or twentieth anniversary date of the

issue. In December 1997, the Company filed a shelf registration statement with the Securities and Exchange Commission

covering an additional $518 million of “unallocated” debt or equity securities. These registrations enable the Company

to issue common stock, preferred stock, senior unsecured debt securities, or subordinated unsecured debt securities. On

February 9, 1998, the Company issued $300 million of 6.875% Debentures due February 15, 2028. The debentures

may not be redeemed prior to maturity. The Company has a remaining uncommitted aggregate of $300 million available

under these previously filed shelf registrations.

The primary component of net cash used in investing activities continues to be new store facilities in connection with

the Company’s expansion plan. Cash acquisitions of fixed assets were $773, $677 and $520 million in 1997, 1996 and

1995, respectively. Financing and investing activities also include noncash transactions of capital leases for new store

facilities and equipment, the result of which is to increase long-term debt and property. During 1997, 1996 and 1995,

the Company acquired fixed assets (primarily new store facilities) under capital leases of $32.7, $182.7 and $96.9

million, respectively.

At January 30, 1998, the Company has a $300 million revolving credit facility with a syndicate of ten banks, available

lines of credit aggregating $206 million for the purpose of issuing documentary letters of credit and standby letters of

credit and $80 million available, on an unsecured basis, for the purpose of short-term borrowings on a bid basis from

various banks. At January 30, 1998, outstanding letters of credit aggregated $66.9 million. In addition, the Company has

a $100 million revolving credit and security agreement from a financial institution with $98.1 million outstanding at

January 30, 1998.

The Company has had only limited involvement with derivative financial instruments, and does not use them for

trading purposes. The Company has entered into derivatives, exclusively interest rate swaps and caps, to lower funding

costs or alter interest rate exposures for long-term liabilities. At January 30, 1998, the Company had no derivative financial

instruments. At January 31, 1997, the Company had five interest rate swap agreements outstanding with financial institu-

tions, having notional amounts of $10 million each and a total notional amount of $50 million and was a party to five

interest rate cap agreements, each with terms tied to the terms of the interest rate swap agreements. These interest rate

swap and cap agreements expired in 1997.

The Company’s major market risk exposure is the potential loss arising from changing interest rates and its impact

on long-term investments and long-term debt. The Company’s policy is to manage interest rate risks by maintaining a

combination of fixed and variable rate financial instruments. At January 30, 1998, long-term investments consisted of

19