Lowe's 1997 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 1997 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

|

|

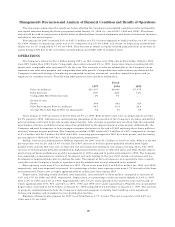

Store Pre-opening Costs – Costs of opening new retail stores are charged to operations as incurred.

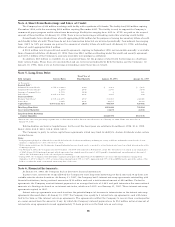

Store Closing Costs – Losses related to impairment of long-lived assets and for long-lived assets to be disposed of are

recognized when expected future cash flows are less than the assets’ carrying value. At the time management commits to

close or relocate a store location, the Company evaluates the carrying value of the assets in relation to its expected future cash

flows. If the carrying value of the assets is greater than the expected future cash flows, a provision is provided for the impairment

of the assets. When a leased location closes, a provision is provided for the present value of future lease obligations, net of

anticipated sublease income.

The estimated realizable value of closed store real estate is included in other assets.

Advertising – Costs associated with advertising are charged to operations as incurred. Advertising expenses were $125.6,

$99.8 and $87.8 million for 1997, 1996 and 1995, respectively.

Recent Accounting Pronouncements – In June 1997, Statement of Financial Accounting Standards No. 130, “Reporting

Comprehensive Income” (SFAS 130) was issued. SFAS 130 will require disclosure of comprehensive income (which is defined

as “the change in equity during a period excluding changes resulting from investments by shareholders and distributions to

shareholders”) and its components. SFAS 130 is effective for fiscal years beginning after December 15, 1997, with reclassifi-

cation of comparative years. The Company will adopt SFAS 130 in the year ending January 29, 1999. Had the new standard

been applied in 1997, there would have been no material difference between comprehensive and reported income.

Statement of Financial Accounting Standards No. 131, “Disclosures about Segments of an Enterprise and Related

Information” (SFAS 131) was also issued in June 1997. SFAS 131 is effective for the Company in the fiscal year ending

January 29, 1999. SFAS 131 redefines how operating segments are determined and requires disclosure of certain financial

and descriptive information about a company’s operating segments. Management does not believe that the adoption of

SFAS 131 will have a material impact on the Company’s current disclosures of its one operating segment, home

improvement retailing.

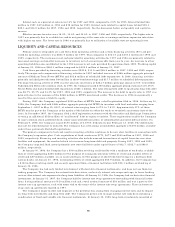

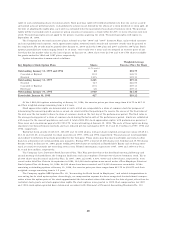

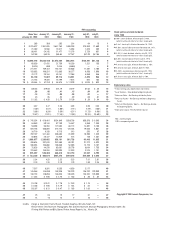

Note 2, Investments:

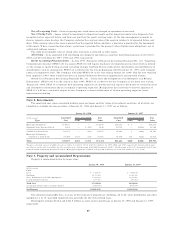

The amortized cost, gross unrealized holding gains and losses and fair values of investment securities, all of which are

classified as available-for-sale securities, at January 30, 1998 and January 31, 1997 are as follows:

January 30, 1998 January 31, 1997

(In Thousands) Amortized Gross Unrealized Fair Amortized Gross Unrealized Fair

Type Cost Gains Losses Value Cost Gains Losses Value

Municipal Obligations $14,557 — — $14,557 $19,514 $ 1 — $19,515

Adjustable Rate Preferred Stock 1,614 — $ (16) 1,598 11,010 — $(422) 10,588

Classified as Short-Term 16,171 — (16) 16,155 30,524 1 (422) 30,103

Municipal Obligations –

Classified as Long-Term 34,904

$291

(34) 35,161 35,718 139 (242) 35,615

Total

$51,075 $291 $ (50) $51,316 $66,242 $140 $(664) $65,718

The proceeds from sales of available-for-sale securities were $14.3, $15.1 and $60.4 million for 1997, 1996 and 1995, respectively. Gross realized gains

and (losses) on the sale of available-for-sale securities were $89 thousand and $(26) thousand for 1997, $80 thousand and $(535) thousand for 1996 and

$326 thousand and $(426) thousand for 1995. Municipal obligations classified as long-term at January 30, 1998 will mature in 1 to 5 years.

Note 3, Property and Accumulated Depreciation:

Property is summarized below by major class:

January 30, 1998 January 31, 1997

(In Thousands)

Cost:

Land $ 711,930 $ 484,100

Buildings 1,533,954 1,324,323

Store, Distribution and Office Equipment 1,393,718 1,175,411

Leasehold Improvements 155,392 120,269

Total Cost 3,794,994 3,104,103

Accumulated Depreciation and Amortization (789,795) (609,707)

Net Property $3,005,199 $2,494,396

The estimated depreciable lives, in years, of the Company’s property are: buildings, 20 to 40; store, distribution and office

equipment, 3 to 10; leasehold improvements, generally the life of the related lease.

Net property includes $438.4 and $421.9 million in assets under capital leases at January 30, 1998 and January 31, 1997,

respectively.

27