Lowe's 1997 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 1997 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

|

|

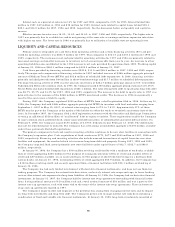

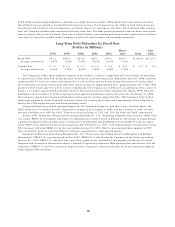

$35.2 million in municipal obligations, classified as available-for-sale securities. Although the fair value of these securities,

like all fixed income securities, would fall if interest rates increase, the Company has the ability to hold its fixed income

investments until maturity and not experience an adverse impact on earnings or cash flows. The following table summa-

rizes the Company’s market risks associated with long-term debt. The table presents principal cash out flows and related

interest rates by fiscal year of maturity. Fair values included below were determined using quoted market rates or interest

rates that are currently available to the Company on debt with similar terms and remaining maturities.

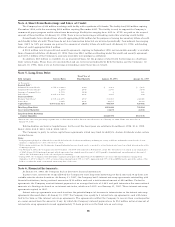

Long-Term Debt Maturities by Fiscal Year

(Dollars in Millions) There- Fair

1998 1999 2000 2001 2002 after Total Value

Fixed Rate $11.3 $96.4 $47.4 $29.5 $59.1 $810.7 $1,054.4 $1,139.7

Average interest rate 8.67% 7.32% 7.27% 8.23% 8.05% 7.94%

Variable Rate $ 1.1 $ 1.5 $ 0.4 $ 0.4 $ 0.4 $ 2.9 $ 6.7 $ 6.7

Average interest rate 4.26% 3.99% 4.25% 4.25% 4.25% 3.76%

The Company’s 1998 capital budget is targeted at $1.4 billion, inclusive of approximately $400 million of operating

or capital leases. More than 80% of this planned commitment is for store expansion. Expansion plans for 1998 consist of

approximately 75 to 80 new stores with about 60% in new markets and the balance being relocations of existing stores

the combination of which will increase sales floor square footage by approximately 20%. Approximately 30% of the 1998

projects will be leased and 70% will be owned. Additionally, the Company has entered into an agreement with a lessor to

build a 1.17 million square foot distribution center in Pennsylvania which will be operational in Spring 1999. This new

distribution center includes a 195 thousand square foot specialty distribution center at the same site. At January 30, 1998,

the Company operated four regional distribution centers and ten smaller support facilities. The Company believes that

funds from operations, funds from debt issuances, leases and existing short-term credit agreements will be adequate to

finance the 1998 expansion plan and other operating needs.

General inflation has not had a material impact on the Company during the past three years. As noted above, the

LIFO credit was $7.0 million in 1997 compared to charges of $1.4 million in 1996, and $8.3 million in 1995. Overall

inventory deflation was .99% for 1997. There was overall inflation of .15% and .79% for 1996 and 1995, respectively.

In June 1997, Statement of Financial Accounting Standards No. 130, “Reporting Comprehensive Income” (SFAS 130)

was issued. SFAS 130 will require disclosure of comprehensive income (which is defined as “the change in equity during

a period excluding changes resulting from investments by shareholders and distributions to shareholders”) and its compo-

nents. SFAS 130 is effective for fiscal years beginning after December 15, 1997, with reclassification of comparative years.

The Company will adopt SFAS 130 in the year ending January 29, 1999. Had the new standard been applied in 1997,

there would have been no material difference between comprehensive and reported income.

Statement of Financial Accounting Standards No. 131, “Disclosures about Segments of an Enterprise and Related

Information” (SFAS 131) was also issued in June 1997. SFAS 131 is effective for the Company in the fiscal year ending

January 29, 1999. SFAS 131 redefines how operating segments are determined and requires disclosure of certain

financial and descriptive information about a company’s operating segments. Management does not believe that the

adoption of SFAS 131 will have a material impact on the Company’s current disclosures of its one operating segment,

home improvement retailing.

20