Lowe's 1997 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 1997 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40

|

|

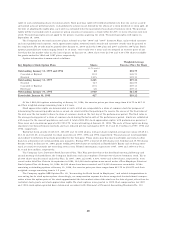

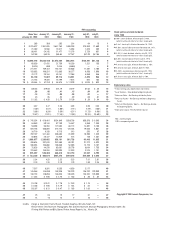

Note 4, Short-Term Borrowings and Lines of Credit:

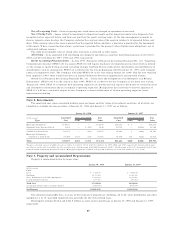

The Company has a $300 million revolving credit facility with a syndicate of 10 banks. The facility has $100 million expiring

November 1998, with the remaining $200 million expiring November 2001. The facility is used to support the Company’s

commercial paper program and for short-term borrowings. Facility fees ranging from .06% to .075% are paid on the unused

amount of these facilities. At January 30, 1998, there were no borrowings outstanding under this revolving credit facility.

Several banks have extended lines of credit aggregating $206 million for the purpose of issuing documentary letters of credit

and standby letters of credit. These lines do not have termination dates but are reviewed periodically. Commitment fees ranging

from .085% to .50% per annum are paid on the amounts of standby letters of credit used. At January 30, 1998, outstanding

letters of credit aggregated $66.9 million.

A $100 million revolving credit and security agreement, expiring in September 1998 and renewable annually, is available

from a financial institution. At January 30, 1998, there was $98.1 million outstanding under this credit and security agreement

and $105.3 million of the Company’s accounts receivable were pledged as collateral.

In addition, $80 million is available, on an unsecured basis, for the purpose of short-term borrowings on a bid basis

from various banks. These lines are uncommitted and are reviewed periodically by both the banks and the Company. At

January 30, 1998, there were no borrowings outstanding under these lines of credit.

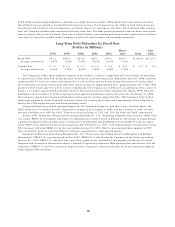

Note 5, Long-Term Debt: Fiscal Year of

Debt Category Interest Rates Final Maturity January 30, 1998 January 31, 1997

(In Thousands)

Secured Debt1:

Industrial Revenue Bonds 3.55% to 6.46%* 2020 $ 4,314 $ 5,497

Industrial Revenue Bonds24.25%* 2005 2,700 5,400

Insurance Company Notes 6.75%*1998 4 161

Other Notes 8.00% to 9.50%*2005 2,497 388

Unsecured Debt3:

Medium Term Notes46.50% to 8.20%*2037 504,787 249,985

Senior Note 6.38% 2005 99,177 99,072

Capital Leases 6.58% to 13.31%*2033 444,569 429,401

Total Long-Term Debt 1,058,048 789,904

Less Current Maturities 12,478 22,566

Long-Term Debt, Excluding

Current Maturities $1,045,570 $767,338

*Interest rate varies as a percentage of prime rate or other interest index. Interest rates shown are as of January 30, 1998. Prime rate was 8.5% at

January 30, 1998.

Debt maturities, exclusive of capital leases, for the next five fiscal years are as follows (in millions): 1998, $1.6; 1999,

$86.0; 2000, $34.9; 2001, $15.8; 2002, $43.9.

The Company is party to certain capital lease agreements which may limit its ability to declare dividends under certain

circumstances.

Notes:

1Real properties pledged as collateral for secured debt had net book values (in millions) at January 30, 1998, as follows: industrial revenue bonds – $13.9;

insurance company notes – $3.3; other notes – $.6.0.

2With certain restrictions, the floating rate demand industrial revenue bonds can be converted to a fixed interest rate based on a fixed interest index at the

Company’s option.

3On February 9, 1998, the Company issued $300 million of 6.875% Debentures due February 15, 2028. The debentures were issued at an original price

of $987.20 per $1,000 principal amount, which represented an original issue discount of .405% payable at maturity and an underwriters’ discount of

.875%. The debentures may not be redeemed prior to maturity.

4During 1997, the Company sold $268 million aggregate principal of Medium-Term Notes (MTN’s) to investors with final maturities ranging from

September 1, 2007 to May 15, 2037, at interest rates ranging from 6.70% to 7.61%. Approximately 37% of these MTN’s may be put at the option of the

holder on either the tenth or twentieth anniversary date of the issue.

Note 6, Financial Instruments:

At January 30, 1998, the Company had no derivative financial instruments.

In prior years, interest rate swaps allowed the Company to raise long-term borrowings at fixed rates and swap them into

variable rates for shorter durations. At January 31, 1997, the Company had 5 interest rate swap agreements outstanding with

financial institutions, having notional amounts of $10 million each and a total notional amount of $50 million. Under the

agreements, the Company received interest payments at an average fixed rate of 6.20% and paid interest on the same notional

amounts at a floating rate based on an interest rate index, which was 5.69% as of January 31, 1997. These interest rate swap

agreements expired in 1997.

Interest rate cap agreements were used to reduce the potential impact of increases in interest rates on the interest rate swap

agreements discussed above. At January 31, 1997, the Company was a party to 5 interest rate cap agreements, each with terms

tied to the terms of the interest rate swap agreements. The agreements entitled the Company to receive from counterparties

on a semi-annual basis the amounts, if any, by which the Company’s interest payments on its $50 million notional amount of

interest rate swap agreements exceed approximately 75 basis points over the fixed rate on each swap.

28