Lowe's 2002 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2002 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

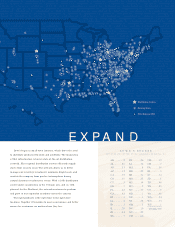

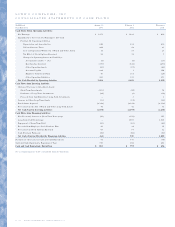

higher than 2000 levels. The increases in sales are attributable to the

Company’s ongoing store expansion and relocation program and

comparable store sales increases. Comparable store sales increased

5.6% in 2002. The Company experienced slight deflation in lum-

ber prices during the year which were offset by inflation in other

building material prices which resulted in essentially no impact on

comparable store sales. The comparable store sales increase prima-

rily resulted from improved sales in almost all merchandising cate-

gories. During the year, the Company experienced its strongest

sales increases in appliances, cabinets, flooring, home organization,

outdoor power equipment, paint, rough plumbing and walls and

windows. The following table presents sales and store information:

2002 2001 2000

Sales (in millions) $26,491 $22,111

$18,779

Sales Increases 20% 18%

18%

Comparable Store Sales Increases 6% 2%

1%

At end of year:

Stores 854 744

650

Sales Floor Square Feet (in millions) 94.7

80.7 67.8

Average Store Size Square Feet (in thousands) 111

108 104

Gross margin in 2002 was 30.3% of sales compared to 28.8%

in 2001. Both of these years showed improvement over the 28.2%

rate achieved in 2000. Margin improvements have continued

throughout all three years, primarily from product mix improve-

ments, lower costs from continued progress in line reviews and

improved shrinkage.

Selling, General and Administrative (SG&A) expenses were

$4.7 billion or 17.9% of sales in 2002. SG&A expenses in the two

previous years were $3.9 billion and $3.3 billion or 17.7% and

17.8% of sales, respectively. During 2002, SG&A increased 21%

compared to the 20% increase in sales. In 2001, SG& A increased

17% compared to the 18% sales increase. In 2000, SG&A

increased 21% compared to the 18% sales increase. The increase

as a percent to sales in SG& A in 2002 was primarily due to

increased store salaries combined with increased bonus achieve-

ment levels driven by increased earnings. The decrease as a percent

to sales in SG&A during 2001 was primarily attributable to

expense controls involving payroll and advertising costs. The

increase as a percent to sales in SG& A during 2000 was primarily

attributable to an increase in store salaries combined with lower

than expected sales levels.

Store opening costs, which were expensed as incurred, were

$128.7 million for 2002 compared to $139.9 million and $131.8

million in 2001 and 2000, respectively. These costs are associated

with the opening of 123 stores in 2002 (112 new and 11 relocat-

ed). This compares to 115 stores in 2001 (101 new and 14 relo-

cated) and 100 stores in 2000 (80 new and 20 relocated). Because

store opening costs are expensed as incurred, the expenses recog-

nized may fluctuate based on the timing of store openings in future

or prior periods. As a percentage of sales, store opening costs were

0.5% for 2002 compared to 0.6% and 0.7% in 2001 and 2000,

respectively. Store opening costs averaged approximately $1.0 mil-

lion, $1.2 million and $1.1 million per store in 2002, 2001 and

2000, respectively.

Depreciation, reflecting continued fixed asset expansion,

increased 21% to $626.6 million in 2002, compared to increases of

26% and 21% in 2001 and 2000, respectively. Depreciation as a

percentage of sales was 2.3% for 2002, a slight decrease from 2.4%

in 2001 and a slight increase from 2.2% in 2000. Approximately

6% of new store facilities opened in the last three years have been

leased, of which approximately 26% were under capital leases.

Property, less accumulated depreciation, increased to $10.4 billion

at January 31, 2003 compared to $8.7 billion at February 1, 2002.

The increase in property resulted primarily from the Company’s

store expansion program and increased distribution capacity.

Net interest costs as a percent of sales were 0.7% for 2002,

0.8% for 2001 and 0.7% for 2000. Net interest costs totaled

$181.9 million in 2002, $173.5 million in 2001 and $120.8 mil-

lion in 2000. Interest costs have increased due to an increase in

debt levels and lower capitalized interest. Interest costs relating to

capital leases were $40.1 million, $40.4 million and $42.0 million

for 2002, 2001 and 2000, respectively. See the following discus-

sion of liquidity and capital resources.

The Company’s effective income tax rates were 37.6%, 37.0%

and 36.8% in 2002, 2001 and 2000, respectively. The higher rates

in 2002 and 2001 were primarily related to expansion into states

with higher state income tax rates.

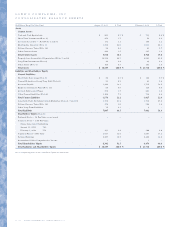

Liquidity and capital resources.

The following table summarizes the Company’s significant con-

tractual obligations and commercial commitments.

Payments Due by Period

Contractual ––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Obligations Less than 1-3 4-5 After 5

(In Millions) Total 1 year years years years

Short-Term Debt $ 50 $ 50 $ – $ – $ –

Long-Term Debt

(net of discount) 3,783 7 665 69 3,042

Capital Lease

Obligations 826 61 120 118 527

Operating Leases 3,163 212 412 403 2,136

Total Contractual

Cash Obligations $ 7,822 $ 330 $1,197 $ 590 $ 5,705