Lowe's 2002 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2002 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

|

|

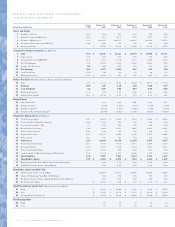

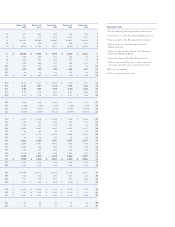

Note 4: Impairment and

store closing costs.

When management makes the decision to close or relocate a store,

or when there are indicators that the carrying amount of a long-

lived asset may not be recoverable, the carrying value of the relat-

ed assets is evaluated in relation to their expected future cash

flows. Losses related to impairment of long-lived assets are recog-

nized when the expected future cash flows are less than the assets’

carrying value. If the carrying value of the assets is greater than the

expected future cash flows and the fair value of the assets is less

than the carrying value, a provision is made for the impairment of

the assets based on the excess of carrying value over fair value. The

fair value of the assets is generally based on internal or external

appraisals and the Company’s historical experience. Provisions for

impairment and store closing costs are included in selling, general

and administrative expenses.

The carrying amount of closed store real estate is included in

other assets and amounted to $93.5 million and $81.6 million at

January 31, 2003 and February 1, 2002, respectively.

When leased locations are closed or become impaired, a liability

is recognized for the net present value of future lease obligations net

of anticipated sublease income. The following table illustrates this lia-

bility and the respective changes in the obligation, which is included

in other current liabilities in the consolidated balance sheet.

(In Millions) Lease Liability

Balance at January 28, 2000 $ 17

Accrual for Store Closing Costs 8

Lease Payments, Net of Sublease Income (6)

Balance at February 2, 2001 $ 19

Accrual for Store Closing Costs 6

Lease Payments, Net of Sublease Income (8)

Balance at February 1, 2002 $ 17

Accrual for Store Closing Costs 9

Lease Payments, Net of Sublease Income (10)

Balance at January 31, 2003 $ 16

Note 5: Short-term borrowings

and lines of credit.

The Company has an $800 million senior credit facility. The facility

is split into a $400 million five-year tranche, expiring in August

2006 and a $400 million 364-day tranche, expiring in July 2003,

which is renewable annually. The facility is used to support the

Company’s $800 million commercial paper program and for short-

term borrowings. Borrowings made are priced based upon market

conditions at the time of funding in accordance with the terms of the

senior credit facility. The senior credit facility contains certain restric-

tive covenants which include maintenance of specific financial

ratios, among others. The Company was in compliance with these

covenants at January 31, 2003. Sixteen banking institutions are par-

ticipating in the $800 million senior credit facility and, as of January

31, 2003, there were no outstanding loans under the facility.

The Company also has a $100 million revolving credit and secu-

rity agreement, expiring in November 2003 and renewable annual-

ly, with a financial institution. Interest rates under this agreement

are determined at the time of borrowing based on market condi-

tions in accordance with the terms of the agreement. The Company

had $50 million outstanding at January 31, 2003 under this agree-

ment. At January 31, 2003, the Company had $136.3 million in

accounts receivable pledged as collateral under this agreement.

Five banks have extended lines of credit aggregating $249.8 mil-

lion for the purpose of issuing documentary letters of credit and

standby letters of credit. These lines do not have termination dates

but are reviewed periodically. Commitment fees ranging from .25%

to .50% per annum are paid on the amounts of standby letters of

credit. Outstanding letters of credit totaled $122.4 million as of

January 31, 2003 and $162.2 million as of February 1, 2002.

The interest rate on short-term borrowings outstanding at

January 31, 2003 was 1.4%. At February 1, 2002, the weighted

average interest rate on short-term borrowings was 1.9%.

Note 6: Long-term debt.

Fiscal Year

(In Millions) of Final January 31, February 1,

Debt Category Interest Rates Maturity 2003 2002

Secured Debt:1

Mortgage Notes 7.00% to 9.25% 2028 $ 55 $ 65

Unsecured Debt:

Debentures 6.50% to 6.88% 2029 692 692

Notes 7.50% to 8.25% 2010 995 994

Medium Term Notes

Series A 7.35% to 8.20% 2023 74 106

Medium Term Notes2

Series B 6.70% to 7.61% 2037 266 266

Senior Notes 6.38% 2005 100 100

Convertible Notes 0.9% to 2.5% 2021 1,119 1,103

Capital Leases 6.58% to 19.57% 2029 464 467

Total Long-Term Debt 3,765 3,793

Less Current Maturities 29 59

Long-Term Debt, Excluding

Current Maturities $3,736 $3,734

1Real properties with an aggregate book value of $132.3 million were pledged as

collateral at January 31, 2003 for secured debt.

2Approximately 37% of these Medium Term Notes may be put at the option of the

holder on either the tenth or twentieth anniversary date of the issue at par value. None of

these notes are currently putable.