Lowe's 2002 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2002 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

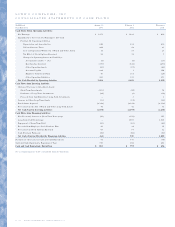

22 / 23 LO WE’S CO MPANIES, INC. ANNUAL REPORT 2002

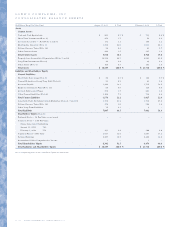

The primary sources of liquidity are cash flows from operating

activities and various lines of credit. Net cash provided by operating

activities was $2.7 billion for 2002 compared to $1.6 billion and

$1.1 billion in 2001 and 2000, respectively. The increase in cash

provided by operating activities during 2002 resulted primarily from

increased net earnings, improved payables leverage due to better

inventory turns and an increase in operating liabilities primarily due

to the increase in sales volume. The increase in cash provided by

operating activities during 2001 resulted primarily from increased

net earnings, the funding of the Company’s ESOP with the issuance

of common stock versus cash in the prior year and improved inven-

tory management. Working capital at January 31, 2003 was $2.0 bil-

lion compared to $1.9 billion at February 1, 2002.

The primary component of net cash used in investing activities

continues to be new store facilities and the infrastructure to sup-

port this growth. Cash acquisitions of fixed assets were $2.4 billion

for 2002. This compares to $2.2 billion and $2.3 billion for 2001

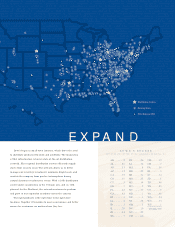

and 2000, respectively. Retail selling space as of January 31, 2003

increased 17% over the selling space as of February 1, 2002. The

February 1, 2002 selling space total of 80.7 million square feet rep-

resents a 19% increase over February 2, 2001.

Cash flows used in financing activities were $64.4 million in

2002. Cash flows provided by financing activities were $929.5 mil-

lion and $1.1 billion in 2001 and 2000, respectively. Financing uses

of cash in 2002 primarily consisted of $66.3 million from cash div-

idend payments, $62.0 million in scheduled debt repayments and

$50.0 million from the repayment of short-term borrowings. These

uses were partially offset by proceeds generated from stock option

exercises totaling $64.5 million and $49.3 million in cash proceeds

from the employee stock purchase plan. The cash provided by

financing activities in 2001 primarily resulted from the issuance of

$580.7 million aggregate principal amount of senior convertible

notes due October 2021 and $1.005 billion aggregate principal

amount of convertible notes due February 2021. These cash inflows

were offset by a decrease in cash due to the payment of $59.9 mil-

lion in cash dividends, $63.8 million in scheduled debt maturities

and the repayment of $150 million in short-term borrowings. In

2000, cash provided by financing activities included the issuance of

$500 million aggregate principal amount of 8.25% notes due June

2010 and $500 million aggregate principal amount of 7.50% notes

due December 2005. These proceeds were offset by a decrease in

cash of $53.5 million from cash dividend payments and $61.3 mil-

lion in scheduled debt repayments. The ratio of long-term debt to

equity plus long-term debt was 31.2%, 36.2% and 33.3% as of the

fiscal years ended 2002, 2001 and 2000, respectively.

The Company has an $800 million senior credit facility. The

facility is split into a $400 million five-year tranche, expiring in

August 2006 and a $400 million 364-day tranche, expiring in July

2003, which is renewable annually. The facility is used to support

the Company’s $800 million commercial paper program and for

short-term borrowings. Any loans made are priced based upon

market conditions at the time of funding in accordance with the

terms of the senior credit facility. The senior credit facility contains

certain restrictive covenants which include maintenance of specif-

ic financial ratios, among others. The Company was in compliance

with these covenants at January 31, 2003. Sixteen banking insti-

tutions are participating in the $800 million senior credit facility

and, as of January 31, 2003, there were no outstanding loans

under the facility.

The Company also has a $100 million revolving credit and

security agreement with a financial institution, expiring in

November 2003 which is renewable for successive periods not to

exceed 364 days each. Interest rates under this agreement are

determined at the time of borrowing based on market conditions

in accordance with the terms of the agreement. The Company had

$50 million outstanding at January 31, 2003 under this agree-

ment, and $136.3 million in customer accounts receivable pledged

as collateral.

Five banks have extended lines of credit aggregating $249.8

million for the purpose of issuing documentary letters of credit

and standby letters of credit. These lines do not have termination

dates but are reviewed periodically. Commitment fees ranging

from .25% to .50% per annum are paid on the amounts of stand-

by letters of credit issued. Outstanding letters of credit totaled

$122.4 million as of January 31, 2003 and $162.2 million as of

February 1, 2002.

In January 2003, the Company exercised its purchase option to

acquire all properties leased under certain operating lease agree-

ments for $261.5 million, which approximated the assets’ original

cost. The Company had three operating lease agreements whereby

lessors committed to purchase land, fund construction costs and

lease properties to the Company. The Company had financed four

regional distribution centers and fourteen retail stores through

these lease agreements. Upon repurchase of these properties, the

three operating leases were terminated.

The Company’s 2003 capital budget is $2.9 billion, inclusive

of approximately $181 million of operating or capital leases.

Approximately 80% of this planned commitment is for store

expansion and new distribution centers. Expansion plans for 2003

consist of approximately 130 stores, including approximately five