Lowe's 2002 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2002 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

|

|

32 / 33 LO WE’S CO MPANIES, INC. ANNUAL REPORT 2002

also clarifies that guarantors are required to recognize, at the incep-

tion of a guarantee, a liability for the fair value of the obligation relat-

ing to the guarantee issued. The initial recognition and measurement

provisions of this interpretation are effective for the Company relat-

ing to guarantees entered or modified after December 31, 2002. The

disclosure provisions are effective for the fiscal year ended January 31,

2003. The initial adoption of this standard has not had a material

impact on the Company’s financial statements.

In November 2002, the EITF issued EITF 02-16 “Accounting

by a Customer (Including a Reseller) for Certain Consideration

Received from a Vendor.” EITF 02-16 provides guidance for clas-

sification in the reseller’s income statement for various circum-

stances under which cash consideration is received from a vendor

by a reseller. In addition, the issue also provides guidance con-

cerning how cash consideration relating to rebates or refunds

should be recognized and measured. This standard will be effec-

tive for the Company for all vendor reimbursement agreements

entered into or modified after December 31, 2002. The Company

has historically treated volume related discounts or rebates as a

reduction of inventory cost and reimbursements of operating

expenses received from vendors as a reduction of those specific

expenses. The Company’s accounting treatment for these vendor

provided funds is consistent with EITF 02-16 with the exception

of certain cooperative advertising allowances. The Company has

previously treated these funds as a reduction of the overall adver-

tising expense. Under EITF 02-16 cooperative advertising

allowances should be treated as a reduction of inventory cost

unless they represent a reimbursement of specific, incremental,

identifiable costs incurred by the customer to sell the vendor’s

product. Cooperative advertising allowances received from ven-

dors have in the past been both specifically associated with pro-

motions to sell the vendor’s product and also, in certain cases, of a

more general nature. Since the Company had entered into sub-

stantially all of the cooperative advertising allowance agreements

relating to fiscal 2003 prior to EITF 02-16’s effective date, its adop-

tion is not expected to have a material impact on fiscal 2003. The

Company is currently evaluating the impact on fiscal 2004.

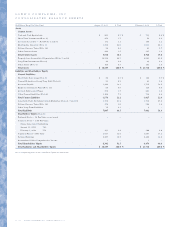

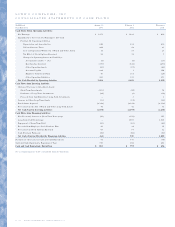

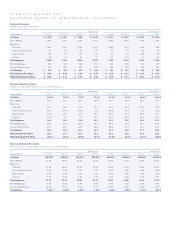

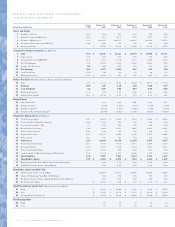

Note 2: Investments.

The Company’s investment securities are classified as available-for-

sale. The amortized cost, gross unrealized holding gains and loss-

es and fair values of the investments at January 31, 2003 and

February 1, 2002 were as follows:

January 31, 2003

Gross Gross

(In Millions) Amortized Unrealized Unrealized Fair

Type Cost Gains Losses Value

Municipal Obligations $ 82 $ – $ – $ 82

Money Market Preferred Stock 186 – – 186

Corporate Notes 5 – – 5

Classified as Short-Term 273 – – 273

Municipal Obligations 11 – – 11

Agency Bonds 17 – – 17

Other 1 – – 1

Classified as Long-Term 29 ––29

Total $ 302 $ – $ – $ 302

February 1, 2002

Gross Gross

(In Millions) Amortized Unrealized Unrealized Fair

Type Cost Gains Losses Value

Municipal Obligations $ 9 $ – $ – $ 9

Money Market Preferred Stock 40 – – 40

Corporate Notes 5 – – 5

Classified as Short-Term 54 – – 54

Municipal Obligations 16 1 – 17

Corporate Notes 5 – – 5

Classified as Long-Term 21 1 – 22

Total $ 75 $ 1 $ – $ 76

The proceeds from sales of available-for-sale securities were $2.0

million, $1.0 million and $8.6 million for 2002, 2001 and 2000,

respectively. Gross realized gains and losses on the sale of available-

for-sale securities were not significant for any of the periods pre-

sented. The municipal obligations and agency bonds classified as

long-term at January 31, 2003 will mature in one to five years.

Note 3: Property and

accumulated depreciation.

Property is summarized by major class in the following table:

January 31, February 1,

(In Millions) 2003 2002

Cost:

Land $ 3,133 $ 2,623

Buildings 5,092 4,276

Equipment 3,663 3,106

Leasehold Improvements 929 627

Total Cost 12,817 10,632

Accumulated Depreciation and Amortization (2,465) (1,979)

Net Property $ 10,352 $ 8,653

The estimated depreciable lives, in years, of the Company’s prop-

erty are: buildings, 20 to 40; store, distribution and office equipment,

3 to 10; leasehold improvements, generally the life of the related lease.

Net property includes $460.9 million in assets under capital

leases at January 31, 2003 and February 1, 2002, respectively.