Lowe's 2004 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2004 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

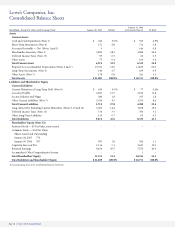

Page 18 Lowe’s 2004 Annual Report

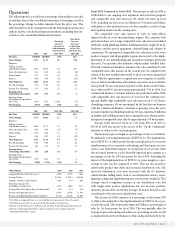

This discussion summarizes the significant factors affecting our con-

solidated operating results, financial condition, liquidity and capital

resources during the three-year period ended January 28, 2005 (our

fiscal years 2004, 2003 and 2002). Each of the fiscal years presented

contains 52 weeks of sales and expenses. This discussion should be

read in conjunction with the consolidated financial statements and

notes to the consolidated financial statements included in this

annual report.

During the fourth quarter of fiscal 2003, we sold 26 commodity-

focused locations operating under The Contractor Yard name (the

“Contractor Yards”). This sale was effected to allow us to continue to

focus on our retail and commercial business. In accordance with

Statement of Financial Accounting Standards (SFAS) No. 144,

“Accounting for the Impairment or Disposal of Long-Lived Assets,” we

have reported the results of operations of the Contractor Yards in dis-

continued operations for fiscal years 2003 and 2002.

Restatement of financial statements

As a result of our system of internal controls over financial reporting,

which includes monitoring of emerging accounting issues and the

review of peer filings, prior to fiscal 2004 year end, we initiated a

review of our accounting policies and practices surrounding leases. As

a result ofthis review, we determined that our treatment of certain

lease-related activities did not conform to accounting principles gen-

erally accepted in the United States of America. Subsequent to this

review, we concluded, in consultation with our independent registered

public accounting firm, Deloitte & Touche LLP, and following discus-

sions with the audit committee of the board of directors, to restate our

prior period financial statements to correct errors resulting from our

accounting for leases.

In the restatement, we accelerated depreciation expense for lease

assets and leasehold improvements to limit the depreciable lives of

those assets to the lease term, as determined in accordance with SFAS

No. 13, “Accounting for Leases,” which we define to include the non-

cancelable lease term and any option renewal period where failure to

exercise such option would result in an economic penalty in such

amount that renewal appears, at the inception of the lease, to be rea-

sonably assured. We also revised our calculation of rent expense (and

the related deferred rent liability) for ground leases by including in our

straight-line rent expense calculations any free-rent occupancy peri-

ods allowed under certain ground leases while our store is being con-

structed on the leased property. In the restatement, we also adjusted

our prior period financial statements to correct immaterial accounting

errors previously identified during the audits of those financial state-

ments. Our Forms 10-Q for fiscal 2005 will reflect the restated informa-

tion for the corresponding quarters in fiscal 2004.

See Note 2 to the consolidated financial statements for further dis-

cussion of the effects of these changes on our consolidated financial

statements. Unless otherwise expressly stated, all financial information

in this annual report is presented inclusive of these revisions.

Executive overview

Fiscal 2004 represented another year of growth for Lowe’s. We ended

the year with 1,087 stores in 48 states, with plans to reach all 50 states

in the coming years. We serve approximately 11 million customers per

week at our stores. Our vision is to be our customers’ first choice for

home improvement in each and every market we serve. To achieve this

vision, we continue to focus on excellent customer service, Everyday

Low Prices (EDLP), and innovative operational and merchandising

strategies. We are also striving to expand our share of the home

improvement market.

The home improvement market is large, fragmented and growing,

due in part to certain socioeconomic trends. The increase in the medi-

an income of the “baby boomer” generation, along with their record

levels of second-home ownership and desire for professional installa-

tion services, is a source of the expected growth. Individuals are also

purchasing their first homes at a younger age. In addition, the number

of households with incomes greater than $120,000 has increased 73%

since 1995. These households spend more than twice the national

average on home improvement. Another source of growth in the

home improvement market is the growing home improvement expen-

ditures by minorities and immigrant populations. Minorities are

projected to contribute at least two-thirds of household growth in

coming decades.

We believe there are still significant opportunities for us to grow

within this increasing home improvement market. Large metropolitan

markets offer a source of opportunity for our expansion. In fiscal 2004,

only 54% of our stores were in the top 100 metropolitan markets.

These 100 markets comprise over 65% of the home improvement

market. Capitalizing on that opportunity, we opened stores in the New

York City, Chicago, Minneapolis and Milwaukee markets in fiscal

2004. We opened a total of 67 stores in the top 100 markets during

2004. In addition, expansion opportunities exist in many smaller mar-

kets utilizing our 94,000-square-foot (94K) store prototype. These are

stores that offer the same look and feel of our larger 116,000-square-

foot (116K) store prototype, with consolidated service in certain

departments and fewer SKUs. These stores have a lower average invest-

ment and operating expense structure, which allows us to profitably

serve these smaller markets.

We expect to open 150 stores in fiscal 2005, increasing total square

footage by 13-14%. We estimate approximately 80% will be the larger

store prototype to serve larger markets and 20% will be 94K stores to

serve smaller markets. Approximately 57% will be in the top 100 met-

ropolitan markets across the country.

Initiatives Driving Performance There are several key initiatives that

we continue to implement to drive the growth of our business and our

results of operations. These initiatives have been put into operation to

capitalize on the growth of the home improvement industry and iden-

tified socioeconomic trends. These initiatives are primarily related to

infrastructure, specialty sales, and merchandising and marketing.

Management’s Discussion and

Analysis of Financial Condition and Results of Operations