Lowe's 2004 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2004 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

Lowe’s 2004 Annual Report Page 21

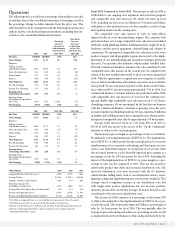

Operations

The following table sets forth the percentage relationship to net sales

of each line item of the consolidated statements of earnings, as well as

the percentage change in dollar amounts from the prior year. This

table should be read in conjunction with the following discussion and

analysis and the consolidated financial statements, including the relat-

ed notes to the consolidated financial statements.

Basis Point

Percentage Increase/

Increase/ (Decrease)

(Decrease) in in Percentage

Dollar Amounts of Net Sales

from Prior Year from Prior Year

–––––––––––––––––––––––––––––––––––– ––––––––––––––––––––––––––––––––––––

2004 2003 2003-2004 2003-2004

Net Sales 100.00% 100.00% 18% N/A

Gross Margin 33.73 31.15 28 258

Expenses:

Selling, General

and Administrative 20.74 18.09 36 265

Store Opening Costs 0.34 0.42 (4) (8)

Depreciation 2.47 2.52 16 (5)

Interest 0.48 0.58 (2) (10)

Total Expenses 24.03 21.61 32 242

Pre-Tax Earnings 9.70 9.54 20 16

Income Tax Provision 3.73 3.61 22 12

Earnings from

Continuing Operations 5.97 5.93 19 4

Earnings from

Discontinued Operations,

Net of Tax 0.00 0.05 (100) (5)

Net Earnings 5.97% 5.98% 18% (1)

2003 2002 2002-2003 2002-2003

Net Sales 100.00% 100.00% 18% N/A

Gross Margin 31.15 30.44 21 71

Expenses:

Selling, General

and Administrative 18.09 17.71 21 38

Store Opening Costs 0.42 0.49 (1) (7)

Depreciation 2.52 2.46 21 6

Interest 0.58 0.70 (1) (12)

Total Expenses 21.61 21.36 19 25

Pre-Tax Earnings 9.54 9.08 24 46

Income Tax Provision 3.61 3.42 25 19

Earnings from

Continuing Operations 5.93 5.66 24 27

Earnings from

Discontinued Operations,

Net of Tax 0.05 0.05 25 0

Net Earnings 5.98% 5.71% 24% 27

Other Metrics 2004 2003 2002

Comparable Store Sales Increases 16.6% 6.7% 5.8%

Average Ticket 2$ 63.43 $ 59.21 $ 56.80

Number of Stores (end of year) 1,087 952 828

Sales Floor Square Feet

(in millions, end of year) 123.7 108.8 94.7

Average Store Size Square Feet (in thousands) 114 114 114

Return on Beginning Assets 311.6% 11.6% 11.0%

Return on Beginning Shareholders’ Equity 421.3% 22.4% 22.6%

1 We define a comparable store as a store that has been open greater than 13 months.

2 We define average ticket as net sales divided by number of transactions.

3 Return on beginning assets is defined as net earnings divided by beginning total assets.

4 Return on beginning shareholders’ equity is defined as net earnings divided by

beginning shareholders’ equity.

Fiscal 2004 Compared to Fiscal 2003 The increase in sales in 2004 is

attributable to our ongoing store expansion and relocation program

and comparable store sales increases. We added 140 stores in fiscal

2004, including our first stores in Minnesota, Wisconsin and Maine,

with plans to add additional stores in these markets as well as large

metropolitan markets in the coming years.

The comparable store sales increase of 6.6% in 2004 reflects

improved sales in every merchandising category. The categories that

performed above our average comparable store sales increase included

millwork, rough plumbing, lumber, building materials, rough electrical,

hardware, outdoor power equipment, seasonal living and cabinets &

countertops. We experienced comparable store sales increases for every

product category and all geographic regions due in part to the imple-

mentation of our merchandising and operations strategies previously

discussed. Our specialty sales initiatives, which include Installed Sales,

SOS and Commercial Business Customer sales, also contributed to the

comparable store sales increase in the current year. We completed the

rollout of the new installed sales model to all of our stores during fiscal

2004. With the opportunity to expand into new categories of installa-

tion, we believe installed sales will continue to provide an area of future

sales growth. We also experienced positive results from our SOS initia-

tives, with total SOS sales increasing approximately 27% in 2004. Our

Commercial Business Customer initiative also performed well in 2004,

with comparable store sales increases of over twice the company aver-

age and double-digit comparable store sales increases in 15 of 18 mer-

chandising categories. We are encouraged by the fact that our business

with the Commercial Business Customer is growing across the store,

not just in lumber and building materials. We also experienced inflation

in lumber and building material prices during the year, which positive-

ly impacted comparable store sales by approximately 150 basis points.

Average ticket increased $4.22 or 7.1% from $59.21 in 2003 to

$63.43 in 2004, due in part to the success of the “Up the Continuum”

initiative as well as Lowe’s credit programs.

The increase in gross margin as a percentage of sales was attributa-

ble primarily to the implementation of EITF 02-16. The implementa-

tion of EITF 02-16, which resulted in the reclassification of our vendor

reimbursements for cooperative advertising and third-party in-store

service costs from SG&A expense to a reduction of cost of sales when

the associated inventory is sold, favorably impacted gross margin as a

percentage of sales by 258 basis points for fiscal 2004. Excluding the

impact of the implementation of EITF 02-16, gross margin as a per-

centage of sales was flat compared to 2003. This was due in part to

unfavorable product mix shifts and increased distribution costs. The

increased distribution costs were associated with the R3 initiative,

which includes adding safety stock to our distribution centers, recon-

figuring racking and implementing new productivity standards. This

strategy caused a temporary increase in our distribution costs, but

with longer-term positive implications for our in-stock position,

inventory productivity and SG&A leverage. Increased fuel prices also

contributed to the increase in distribution costs.

The increase in SG&A expenses as a percentage of sales from 2003

to 2004 is due primarily to the implementation of EITF 02-16, as pre-

viously discussed. This unfavorably impacted SG&A as a percentage of

sales by 316 basis points for fiscal 2004. This was partially offset by

leverage in gross advertising and salaries as a percentage of sales, as well

as improvements in the performance of the credit portfolio held by GE.