Lowe's 2004 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2004 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

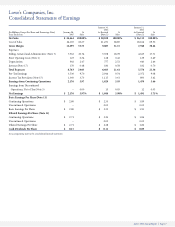

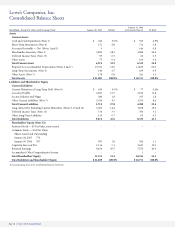

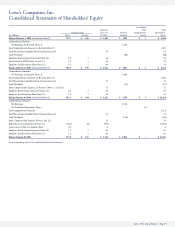

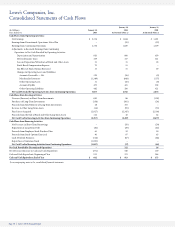

Lowe’s 2004 Annual Report Page 31

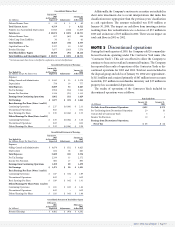

NOTE 1 Summary of significant

accounting policies

The Company is the world’s second largest home improvement retailer

and operated 1,087 stores in 48 states at January 28, 2005. Below are

those accounting policies considered to be significant by the Company.

Fiscal Year The Company’s fiscal year ends on the Friday nearest the

end of January. Each of the fiscal years presented contains 52 weeks. All

references herein for the years 2004, 2003 and 2002 represent the fiscal

years ended January 28, 2005, January 30, 2004, and January 31, 2003,

respectively.

Principles of Consolidation The consolidated financial statements

include the accounts of the Company and its subsidiaries, all of which

are wholly owned. All material intercompany accounts and transactions

have been eliminated.

Use of Estimates The preparation of the Company’s financial state-

ments in accordance with accounting principles generally accepted in

the United States of America requires management to make estimates

that affect the reported amounts of assets, liabilities, sales and expenses

and related disclosures of contingent assets and liabilities. The Company

bases these estimates on historical results and various other assumptions

believed to be reasonable, all of which form the basis for making esti-

mates concerning the carrying values of assets and liabilities that are not

readily available from other sources. Actual results may differ from these

estimates.

Cash and Cash Equivalents Cash and cash equivalents include cash

on hand, demand deposits and short-term investments with original

maturities of three months or less when purchased.

Investments The Company has a cash management program which

provides for the investment of cash balances not expected to be used in

current operations in financial instruments that have maturities of up to

10 years. Investments, exclusive of cash equivalents, with a maturity date

of one year or less from the balance sheet date or that are expected to be

used in current operations, are classified as short-term investments. All

other investments are classified as long-term. Investments consist pri-

marily of money market preferred stocks, municipal obligations, agency

bonds, corporate notes and stocks, auction rate securities and mutual

funds.

The Company has classified all investment securities as available-for-

sale, and they are carried at fair market value. Unrealized gains and loss-

es on such securities are included in accumulated other comprehensive

income in shareholders’ equity.

Derivative Financial Instruments The Company does not use deriv-

ative financial instruments for trading purposes.

Accounts Receivable The majority of accounts receivable arise from

sales to Commercial Business Customers. The Company sells its com-

mercial business accounts receivable to General Electric Company and

its subsidiaries (GE). When the Company sells its commercial business

accounts receivable, it retains certain interests in those receivables,

including the funding of a loss reserve and its obligation related to GE’s

ongoing servicing of the receivables sold. Any gain or loss on the sale is

determined based on the previous carrying amounts of the transferred

assets allocated at fair value between the receivables sold and the inter-

ests retained. Fair value is based on the present value of expected future

cash flows taking into account the key assumptions of anticipated cred-

it losses, payment rates, late fee rates, GE’s servicing costs and the dis-

count rate commensurate with the uncertainty involved. Due to the

short-term nature of the receivables sold, changes to the key assump-

tions would not materially impact the recorded gain or loss on the sales

of receivables or the fair value of the retained interests in the receivables.

See Note 5 for further discussion of the sale of the Company’s

accounts receivable during fiscal 2004.

The allowance for doubtful accounts is based on historical experi-

ence and a review of existing receivables. The allowance for doubtful

accounts was $2 million at January 28, 2005, and $7 million at

January 30, 2004.

Sales generated through the Company’s private label credit cards are

not reflected in receivables. Under an agreement with GE, credit is

extended directly to customers by GE. All credit program-related servic-

es are performed and controlled directly by GE. The Company has the

option, but no obligation, at the end of the agreement to purchase

the receivables.

The total portfolio of receivables held by GE, including both receiv-

ables originated by GE from the Company’s private label credit cards

and commercial business accounts receivable originated by the

Company and sold to GE, approximated $4.5 billion at January 28, 2005,

and $3.8 billion at January 30, 2004.

Merchandise Inventory Inventory is stated at the lower of cost or

market using the first-in, first-out method of inventory accounting. The

cost of inventory also includes certain costs associated with the prepara-

tion of inventory for resale.

The Company records an inventory reserve for the loss associated

with selling discontinued inventories below cost. This reserve is based

on management’s current knowledge with respect to inventory levels,

sales trends and historical experience relating to the liquidation of dis-

continued inventory. Management does not believe the Company’s

merchandise inventories are subject to significant risk of obsolescence

in the near term, and management has the ability to adjust purchasing

practices based on anticipated sales trends and general economic con-

ditions. However, changes in consumer purchasing patterns could

result in the need for additional reserves. The Company also records an

inventory reserve for the estimated shrinkage between physical inven-

tories. This reserve is based primarily on actual shrink results from pre-

vious physical inventories. Changes in actual shrink results from com-

pleted physical inventories could result in revisions to previously esti-

mated shrink expense. Management believes it has sufficient current

and historical knowledge to record reasonable estimates for both of

these inventory reserves.

Property and Depreciation Property is recorded at cost. Costs asso-

ciated with major additions are capitalized and depreciated. Capital

assets are expected to yield future benefits and have useful lives which

exceed one year. The total cost of a capital asset generally includes all

applicable sales taxes, delivery costs, installation costs and other appro-

priate costs incurred by the Company in the case of self-constructed

Notes to Consolidated Financial Statements

YEARS ENDED JANUARY 28, 2005, JANUARY 30, 2004 AND JANUARY 31, 2003