Lowe's 2004 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2004 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

|

|

Page 36 Lowe’s 2004 Annual Report

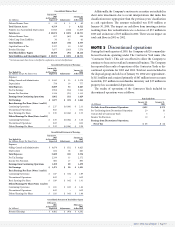

NOTE 4

Investments

The Company’s investment securities are classified as available-for-

sale. The amortized cost, gross unrealized holding gains and losses and

fair values of the investments at January 28, 2005, and January 30,

2004, were as follows:

January 28, 2005

Gross Gross

Type Amortized Unrealized Unrealized Fair

(In Millions) Cost Gains Losses Value

Municipal Obligations $ 162 $ – $ – $ 162

Money Market Preferred Stock 9 – – 9

Classified as Short-Term 171 – – 171

Municipal Obligations 97 – (1) 96

Corporate Notes 19 – – 19

Asset-Backed Obligations 16 – – 16

Mutual Funds 14 1 – 15

Classified as Long-Term 146 1 (1) 146

Total $ 317 $ 1 $ (1) $ 317

January 30, 2004

Gross Gross

Type Amortized Unrealized Unrealized Fair

(In Millions) Cost Gains Losses Value

Municipal Obligations $ 626 $ – $ – $ 626

Money Market Preferred Stock 78 – – 78

Corporate Notes 7 – – 7

Classified as Short-Term 711 – – 711

Municipal Obligations 92 – – 92

Corporate Notes 32 – – 32

Agency Bonds 23 – – 23

Asset-Backed Obligations 16 – – 16

Mutual Funds 5 1 – 6

Classified as Long-Term 168 1 – 169

Total $ 879 $ 1 $ – $ 880

The proceeds from sales of available-for-sale securities were $117

million, $204 million and $2 million for 2004, 2003 and 2002, respec-

tively. Gross realized gains and losses on the sale of available-for-sale

securities were not significant for any of the periods presented. The

municipal obligations classified as long-term at January 28, 2005, will

mature in one to five years. Corporate notes classified as long-term at

January 28, 2005, will mature in one to two years. Asset-backed obli-

gations classified as long-term at January 28, 2005, will mature in two

to seven years.

NOTE 5

Accounts receivable

In May 2004, the Company entered into an agreement with GE to sell

its then-existing portfolio of commercial business accounts receivable

to GE. During the term of the agreement, which ends on December 31,

2009, unless terminated sooner by the parties, GE also purchases at

face value new commercial business accounts receivable originated by

the Company and services these accounts. These receivables arise pri-

marily from sales of goods and services to the Company’s Commercial

Business Customers.

The Company accounts for the transfers as sales of the accounts

receivable. When the Company sells its commercial business accounts

receivable, it retains certain interests in those receivables, including the

funding of a loss reserve and its obligation related to GE’s ongoing

servicing of the receivables sold. Any gain or loss on the sale is deter-

mined based on the previous carrying amounts of the transferred

assets allocated at fair value between the receivables sold and the inter-

ests retained. Fair value is based on the present value of expected

future cash flows taking into account the key assumptions of antici-

pated credit losses, payment rates, late fee rates, GE’s servicing costs

and the discount rate commensurate with the uncertainty involved.

Due to the short-term nature of the receivables sold, changes to the key

assumptions would not materially impact the recorded gain or loss on

the sales of receivables or the fair value of the retained interests in the

receivables.

The initial portfolio of commercial business accounts receivable

sold to GE in May 2004 totaled $147 million. Total commercial busi-

ness accounts receivable sold to GE since program inception through

the end of 2004 totaled $1.2 billion. During 2004, the Company rec-

ognized losses of $34 million on these sales as SG&A expense, which

primarily relate to the fair value of the obligations incurred related to

servicing costs that are remitted to GE monthly. At January 28, 2005,

the fair value of the retained interests was a net liability of $0.2 million

and was determined based on the present value of expected future

cash flows.

NOTE 6

Property and accumulated

depreciation

Property is summarized by major class in the following table:

Estimated Depreciable January 28, January 30,

(In Millions) Lives (In Years) 2005 2004

Cost:

Land N/A $ 4,197 $ 3,635

Buildings 7-40 7,007 5,950

Equipment 3-10 5,405 4,355

Leasehold Improvements* 7-30 1,401 1,133

Total Cost 18,010 15,073

Accumulated Depreciation and Amortization (4,099) (3,254)

Net Property $ 13,911 $ 11,819

* Leasehold improvements are depreciated over the shorter of their estimated useful lives

or the term of the related lease, which is defined to include the non-cancelable lease term

and any option renewal period where failure to exercise such option would result in an

economic penalty in such amount that renewal appears, at the inception of the lease, to

be reasonably assured. During the term of a lease, if a substantial additional investment

is made in a leased location, the Company also reevaluates its definition of lease term to

determine whether the investment would constitute an economic penalty in such

amount that renewal appears, at the time of the reevaluation, to be reasonably assured.

Included in net property are assets under capital lease of $538 mil-

lion, less accumulated depreciation of $227 million, at January 28,

2005, and $539 million, less accumulated depreciation of $201 million,

at January 30, 2004.

NOTE 7

Impairment and store

closing costs

The Company periodically reviews the carrying value of long-lived

assets for potential impairment. When management commits to close

or relocate a store location, or when there are indicators that the car-

rying value of a long-lived asset may not be recoverable, the Company

evaluates the carrying value of the asset in relation to its expected

future cash flows. If the carrying value of the asset is greater than the