Lowe's 2004 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2004 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

Lowe’s 2004 Annual Report Page 33

Certain Consideration Received from a Vendor.” See further discussion

of cooperative advertising allowances and the impact of the implemen-

tation of EITF 02-16 in Vendor Funds.

Vendor Funds The Company receives funds from vendors in the

normal course of business for a variety of reasons, including purchase-

volume-related discounts and rebates, advertising allowances, reim-

bursement for third-party in-store service related costs, defective

merchandise allowances and reimbursement for selling expenses and

display costs. Management uses projected purchase volumes to deter-

mine earnings rates, validates those projections based on actual and

historical purchase trends and applies those rates to actual purchase vol-

umes to determine the amount of funds accrued by the Company and

receivable from the vendor. Amounts accrued could be impacted if actu-

al purchase volumes differ from projected purchase volumes.

The Company historically treated purchase-volume-related dis-

counts or rebates as a reduction of inventory cost and reimbursements

of operating expenses received from vendors as a reduction of those spe-

cific expenses. The Company’s historical accounting treatment for these

vendor-provided funds was consistent with EITF 02-16 with the excep-

tion of certain cooperative advertising and third-party in-store services

for which the costs are ultimately funded by vendors. The Company pre-

viously treated the cooperative advertising allowances and third-party

in-store service funds as a reduction of the related expense.

Under EITF 02-16, cooperative advertising allowances and third-

party in-store service funds are treated as a reduction of inventory cost,

unless they represent a reimbursement of specific, incremental and

identifiable costs incurred by the customer to sell the vendor’s product.

Substantially all of the cooperative advertising and third-party in-store

service funds that the Company receives do not meet the specific, incre-

mental and identifiable criteria in EITF 02-16. Therefore, for coopera-

tive advertising and third-party in-store service fund agreements

entered into after December 31, 2002, which was the effective date of the

related provision of EITF 02-16, the Company treats funds that do not

meet the specific, incremental and identifiable criteria as a reduction in

the cost of inventory and recognizes these funds as a reduction of cost of

sales when the inventory is sold. There is no impact to the timing of

when the funds are received from vendors or the associated cash flows.

Third-party in-store service costs were included in SG&A expense

and the funds received from vendors were recorded as a reduction of

inventory cost in 2004. Third-party in-store service costs for 2003 and

2002 are presented net of vendor funds of $175 million and $69 million,

respectively.

This accounting change did not have a material impact on the 2003

financial statements since substantially all of the cooperative advertising

allowance and third-party in-store service fund agreements for 2003

were entered into prior to December 31, 2002, the effective date of the

related provision of EITF 02-16. This accounting change reduced dilut-

ed earnings per share by approximately $0.16 in fiscal 2004.

Comprehensive Income The Company reports comprehensive income

in its consolidated statement of shareholders’ equity. Comprehensive

income represents changes in shareholders’ equity from non-owner

sources. For each of the three years in the period ended January 28, 2005,

unrealized holding gains/losses on available-for-sale securities were the

only items of other comprehensive income for the Company and were

immaterial. The reclassification adjustments for gains/losses included in

net earnings for 2004, 2003 and 2002 were also immaterial.

Stock-Based Compensation Prior to 2003, the Company accounted

for its stock-based compensation plans under the recognition and meas-

urement provisions of Accounting Principles Board (APB) Opinion

No. 25, “Accounting for Stock Issued to Employees,” and related

Interpretations. Therefore, no stock-based employee compensation is

reflected in 2002 net earnings, other than for restricted stock grants, as

all options granted under those plans had an exercise price equal to the

market value of the underlying common stock on the date of grant.

Effective February 1, 2003, the Company adopted the fair value

recognition provisions of Statement of Financial Accounting Standards

(SFAS) No. 123, “Accounting for Stock-Based Compensation,” prospec-

tively for all employee awards granted or modified after January 31,

2003. Therefore, in accordance with the requirements of SFAS No. 148,

“Accounting for Stock-Based Compensation-Transition and

Disclosure,” the cost related to stock-based employee compensation

included in the determination of net earnings for years ended January

28, 2005, and January 30, 2004 is less than that which would have been

recognized if the fair-value-based method had been applied to all awards

since the original effective date of SFAS No. 123. The Company recog-

nized compensation expense in 2004 and 2003 totaling $70 and $51

million, respectively, for stock options and awards granted or modified

during the year. These options generally vest over three years.

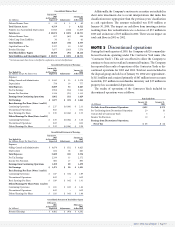

The following table illustrates the effect on net earnings and earnings

per share if the fair-value-based method had been applied to all out-

standing and unvested awards in each period:

2003 2002

As Restated As Restated

(In Millions, Except Per Share Data) 2004 (Note 2) (Note 2)

Net Earnings as Reported $ 2,176 $ 1,844 $1,491

Add: Stock-Based Compensation

Expense Included in Net Earnings,

Net of Related Tax Effects 43 32 –

Deduct: Total Stock-Based

Compensation Expense Determined

Under the Fair-Value-Based Method for All

Awards, Net of Related Tax Effects (85) (93) (85)

Pro Forma Net Income $ 2,134 $ 1,783 $1,406

Earnings Per Share:

Basic – as Reported $ 2.80 $ 2.35 $ 1.91

Basic – Pro Forma $ 2.75 $ 2.26 $ 1.81

Diluted – as Reported $ 2.71 $ 2.28 $ 1.86

Diluted – Pro Forma $ 2.66 $ 2.20 $ 1.75

The fair value of each option grant is estimated on the date of grant

using the Black-Scholes option-pricing model with the assumptions

listed in the following table.

2004 2003 2002

Weighted Average Fair Value Per Option $ 16.56 $ 17.64 $ 19.22

Assumptions Used:

Weighted Average Expected Volatility 38.3% 44.0% 43.7%

Weighted Average Expected Dividend Yield 0.22% 0.26% 0.27%

Weighted Average Risk-Free Interest Rate 2.39% 2.89% 4.35%

Weighted Average Expected Life, in Years 3.3 5.5 4.0-7.0

Shipping and Handling Costs The Company includes shipping and

handling costs relating to the shipment of products to customers by third

parties in cost of sales. Shipping and handling costs, which include salaries

and vehicle operations expenses relating to the delivery of products to cus-

tomers by the Company, are classified as SG&A expenses. Shipping and