Lowe's 2004 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2004 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

|

|

Page 34 Lowe’s 2004 Annual Report

handling costs included in SG&A expenses were $255 million, $216 mil-

lion, and $193 million during 2004, 2003 and 2002, respectively.

Recent Accounting Pronouncements In January 2003, the

Financial Accounting Standards Board (FASB) issued Interpretation 46,

“Consolidation of Variable Interest Entities, an Interpretation of ARB

No. 51”(FIN 46). In December 2003, the FASB issued a revision to FIN

46 to make certain technical corrections and address certain implemen-

tation issues that had arisen. FIN 46 provides guidance on the identifi-

cation and consolidation of variable interest entities, or VIEs, which are

entities for which control is achieved through means other than through

voting rights. The provisions of FIN 46 are required to be applied to

VIEs created or in which the Company obtains an interest after January

31, 2003. For VIEs in which the Company holds a variable interest that

it acquired before February 1, 2003, the provisions of FIN 46 were effec-

tive for the first quarter of 2004. The adoption of FIN 46, as revised, did

not have an impact on the Company’s consolidated financial statements.

In October 2004, the EITF reached a consensus on EITF Issue

No. 04-8 (EITF 04-8), “Accounting Issues Related to Certain Features

of Contingently Convertible Debt and the Effect on Diluted Earnings

per Share.” Based on the EITF’s conclusion, the dilutive effect of con-

tingently convertible debt instruments should be included in the

calculation of diluted earnings per share regardless of whether the

contingency has been met. The Company implemented the provisions

of EITF 04-8 in the fourth quarter of 2004. In accordance with the

transition provisions of EITF 04-8, the Company has retroactively

adjusted diluted earnings per share calculations for all periods pre-

sented to include the dilutive effect of the assumed conversion of the

Company’s $580.7 million Senior Convertible Notes issued in October

2001. The implementation of EITF 04-8 reduced diluted earnings per

share by $0.03 for the year ended January 28, 2005, and $0.02 for the

each of the years ended January 30, 2004, and January 31, 2003. See

further discussion in Note 11 to the consolidated financial statements.

In December 2004, the FASB issued SFAS No. 123 (revised) “Share-

Based Payment.” This statement eliminates the alternative to account

for share-based compensation transactions using APB Opinion No. 25

and will require that compensation expense be measured based on the

grant-date fair value of the award and recognized over the requisite

service period for awards that vest. The Company is currently evaluat-

ing the impact of this Statement, which is effective as of the beginning

of the first interim or annual reporting period beginning after June 15,

2005. The Company currently recognizes stock-based compensation

expense in accordance with the fair value provisions of SFAS No. 123.

The adoption of SFAS No. 123 (revised) may affect the Company’s

methodology for determining the fair value of stock-based compensa-

tion transactions and the method for recognizing the expense associ-

ated with these transactions. However, the Company does not expect

the adoption of this statement to have a material impact on its consol-

idated financial statements.

In December 2004, the FASB issued SFAS No. 153, “Exchanges of

Nonmonetary Assets, an amendment of APB Opinion No. 29,

Accounting for Nonmonetary Transactions.” The amendments made

by SFAS No. 153 are based on the principle that exchanges of non-

monetary assets should be measured based on the fair value of the

assets exchanged. Further, the amendments eliminate the exception for

nonmonetary exchanges of similar productive assets and replace it

with a broader exception for exchanges of nonmonetary assets that do

not have commercial substance. The provisions of SFAS No. 153 are

effective for nonmonetary asset exchanges occurring in fiscal periods

beginning after June 15, 2005. The Company does not expect the

adoption of this statement to have a material impact on its consoli-

dated financial statements.

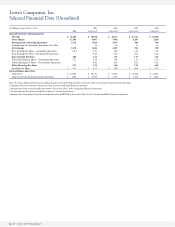

Segment Information The Company’s operations are aggregated

within one reportable segment, representing the operations of the

Company’s home improvement retail stores within the United States

of America.

Reclassifications Certain prior period amounts have been reclassi-

fied to conform to current classifications.

NOTE 2

Restatement

Subsequent to the issuance of the Company’s January 30, 2004 con-

solidated financial statements, the Company determined that its treat-

ment of certain lease-related activities did not conform to accounting

principles generally accepted in the United States of America. This was

identified as a result of the Company’s review of its accounting poli-

cies and practices surrounding leases. Subsequent to this review, the

Company, in consultation with its independent registered public

accounting firm, Deloitte & Touche LLP, and following discussions

with the audit committee of the board of directors, concluded to

restate the Company’s prior period financial statements to correct

errors resulting from its accounting for leases. Although the Company

does not believe that this error resulted in a material misstatement of

the Company’s consolidated financial statements for any annual or

interim periods, the effects of correcting the error would have had a

material effect on the Company’s results of operations for the fourth

quarter of fiscal 2004.

In the restatement, the Company accelerated its depreciation expense

for lease assets and leasehold improvements to limit the depreciable lives

of those assets to the lease term, as determined in accordance with SFAS

No. 13, “Accounting for Leases,” which the Company defines to include

the non-cancelable lease term and any option renewal period where fail-

ure to exercise such option would result in an economic penalty in such

amount that renewal appears, at the inception of the lease, to be reason-

ably assured. Previously, the Company depreciated these assets over the

estimated useful lives for similar owned assets. The Company also

revised its calculation of rent expense (and the related deferred rent lia-

bility) for its ground leases by including in its straight line rent expense

calculations any free-rent occupancy periods allowed under those

ground leases while the store is being constructed on the leased proper-

ty. The Company previously recognized rent expense for these types of

leases upon commencement of lease payments. In the restatement, the

Company also adjusted its prior period financial statements to correct

immaterial accounting errors previously identified during the audits of

those financial statements. The impact on previously reported net earn-

ings ofthese other adjustments resulted in a decrease of $18 million and

an increase of $38 million for fiscal years 2003 and 2002, respectively.

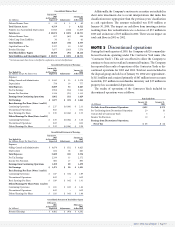

The following tables summarize the effects of the restatement on

the Company’s consolidated balance sheet as of January 30, 2004, as

well as the effects of these changes on the Company’s consolidated

statements of earnings for fiscal years 2003 and 2002 and the effect on

retained earnings as of February 1, 2002. These changes did not affect

cash flows in 2003 or 2002.