Nike 2016 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2016 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

|

|

PART II

The following tables present the amounts affecting the Consolidated Statements of Income for the years ended May 31, 2016, 2015 and 2014:

(In millions)

Amount of Gain (Loss)

Recognized in Other

Comprehensive Income

on Derivatives(1)

Amount of Gain (Loss)

Reclassified From Accumulated

Other Comprehensive Income into Income(1)

Year Ended May 31, Location of Gain (Loss)

Reclassified From Accumulated Other

Comprehensive Income Into Income

Year Ended May 31,

2016 2015 2014 2016 2015 2014

Derivatives designated as cash flow hedges:

Foreign exchange forwards and options $ 90 $ (202) $ (48) Revenues $ (88) $ (95) $ 14

Foreign exchange forwards and options (57) 1,109 (78) Cost of sales 586 220 12

Foreign exchange forwards and options — — 4 Total selling and administrative expense — — —

Foreign exchange forwards and options (25) 497 (21) Other (income) expense, net 219 136 10

Interest rate swaps (83) 76 — Interest expense (income), net — — —

Total designated cash flow hedges (75) 1,480 (143) 717 261 36

Derivatives designated as net investment hedges:

Foreign exchange forwards and options $ — $ — $ — Other (income) expense, net $ — $ — $ —

(1) For the years ended May 31, 2016, 2015 and 2014, the amounts recorded in Other (income) expense, net as a result of hedge ineffectiveness and the discontinuance of cash flow hedges

because the forecasted transactions were no longer probable of occurring were immaterial.

Amount of Gain (Loss) Recognized in

Income on Derivatives

Location of Gain (Loss) Recognized

in Income on Derivatives

Year Ended May 31,

(In millions) 2016 2015 2014

Derivatives designated as fair value hedges:

Interest rate swaps(1) $ 2 $ 5 $ 5 Interest expense (income), net

Derivatives not designated as hedging instruments:

Foreign exchange forwards and options (68) 611 (75) Other (income) expense, net

Embedded derivatives $ (2) $ (1) $ (1) Other (income) expense, net

(1) All interest rate swaps designated as fair value hedges meet the shortcut method requirements under the accounting standards for derivatives and hedging. Accordingly, changes in the

fair values of the interest rate swaps are considered to exactly offset changes in the fair value of the underlying long-term debt. Refer to “Fair Value Hedges” in this note for additional detail.

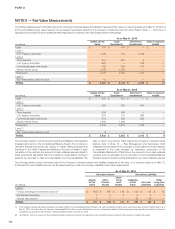

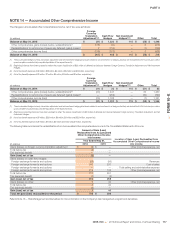

Refer to Note 6 — Fair Value Measurements for a description of how the

above financial instruments are valued and Note 14 — Accumulated Other

Comprehensive Income and the Consolidated Statements of Shareholders’

Equity for additional information on changes in Accumulated other

comprehensive income for the years ended May 31, 2016, 2015 and 2014.

Cash Flow Hedges

The purpose of the Company’s foreign exchange risk management program

is to lessen both the positive and negative effects of currency fluctuations on

the Company’s consolidated results of operations, financial position and cash

flows. Foreign currency exposures that the Company may elect to hedge in

this manner include product cost exposures, non-functional currency

denominated external and intercompany revenues, selling and administrative

expenses, investments in U.S. Dollar-denominated available-for-sale debt

securities and certain other intercompany transactions.

Product cost exposures are primarily generated through non-functional

currency denominated product purchases and the foreign currency

adjustment program described below. NIKE entities primarily purchase

products in two ways: (1) Certain NIKE entities purchase product from the

NIKE Trading Company (“NTC”), a wholly owned sourcing hub that buys

NIKE branded products from third party factories, predominantly in U.S.

Dollars. The NTC, whose functional currency is the U.S. Dollar, then sells the

product to NIKE entities in their respective functional currencies. When the

NTC sells to a NIKE entity with a different functional currency, the result is a

foreign currency exposure for the NTC. (2) Other NIKE entities purchase

product directly from third party factories in U.S. Dollars. These purchases

generate a foreign currency exposure for those NIKE entities with a functional

currency other than the U.S. Dollar.

The Company operates a foreign currency adjustment program with certain

factories. The program is designed to more effectively manage foreign

currency risk by assuming certain of the factories’ foreign currency

exposures, some of which are natural offsets to the Company’s existing

foreign currency exposures. Under this program, the Company’s payments

to these factories are adjusted for rate fluctuations in the basket of currencies

(“factory currency exposure index”) in which the labor, materials and overhead

costs incurred by the factories in the production of NIKE branded products

(“factory input costs”) are denominated. For the portion of the indices

denominated in the local or functional currency of the factory, the Company

may elect to place formally designated cash flow hedges. For all currencies

within the indices, excluding the U.S. Dollar and the local or functional

currency of the factory, an embedded derivative contract is created upon the

factory’s acceptance of NIKE’s purchase order. Embedded derivative

contracts are separated from the related purchase order, as further described

within the Embedded Derivatives section below.

The Company’s policy permits the utilization of derivatives to reduce its

foreign currency exposures where internal netting or other strategies cannot

be effectively employed. Typically, the Company may enter into hedge

contracts starting up to 12 to 24 months in advance of the forecasted

transaction and may place incremental hedges up to 100% of the exposure

by the time the forecasted transaction occurs. The total notional amount of

outstanding foreign currency derivatives designated as cash flow hedges

was $11.5 billion as of May 31, 2016.

As of May 31, 2016, the Company had a series of forward-starting interest

rate swap agreements with a total outstanding notional amount of $1.5 billion.

These instruments were designated as cash flow hedges of the variability in

the expected cash outflows of interest payments on future debt due to

changes in benchmark interest rates. During the second quarter of fiscal

2016, the Company terminated certain forward-starting interest rate swaps

with a total notional amount of $1 billion in connection with the October 29,

2015 debt issuance (refer to Note 8 — Long-Term Debt). Upon termination of

these forward-starting swaps, the Company received a cash payment from

the related counterparties of $34 million, which was recorded in Accumulated

other comprehensive income and will be released through Interest expense

(income), net as interest payments are made over the term of the issued debt.

NIKE, INC. 2016 Annual Report and Notice of Annual Meeting 119

FORM 10-K