Safeway 2001 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2001 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

16

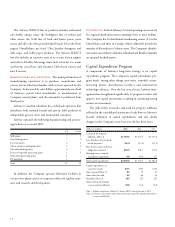

Critical Accounting Policies

Critical accounting policies are those accounting policies that

management believes are important to the portrayal of Safeway’s

financial condition and results and require management’s most

difficult, subjective or complex judgments, often as a result of

the need to make estimates about the effect of matters that are

inherently uncertain.

The Company is primarily self-insured for workers’ compensa-

tion, automobile and general liability costs. It is the Company’s pol-

icy to record its self-insurance liability, as determined actuarially,

based on claims filed and an estimate of claims incurred but not yet

reported. Any actuarial projection of losses concerning workers’

compensation and general liability is subject to a high degree of vari-

ability. Among the causes of this variability are unpredictable exter-

nal factors affecting future inflation rates, litigation trends, legal

interpretations, benefit level changes and claim settlement patterns.

The majority of the Company’s workers’ compensation liabili-

ty is from claims occurring in California. California workers’ com-

pensation has received a tremendous amount of attention from the

state’s politicians, insurers, employers and providers, as well as the

public in general. Recent years have seen an escalation in the num-

ber of legislative reforms, judicial rulings and social phenomena

affecting this business. Some of the many sources of uncertainty in

the Company’s reserve estimates include changes in benefit levels

and medical fee schedules. Other reforms address vocational reha-

bilitation limitations, restrictions on the number of allowed med-

ical-legal evaluations, the treatment of stress and post-termination

claims and the permanent disability rating schedule.

The Company’s workers’ compensation future funding esti-

mates anticipate no change in the benefit structure. Statutory

changes could have a significant impact on future claim costs.

The California Legislature is currently discussing benefit reforms.

At this point it is unknown what, if any, changes will result.

It is the Company’s policy to recognize losses relating to the

impairment of long-lived assets when future cash flows, discounted

using a risk-free rate of interest, are less than the assets’ carrying

value. For stores to be closed that are under long-term leases, the

Company records a liability for the future minimum lease pay-

ments and related ancillary costs from the date of closure to the end

of the remaining lease term, net of estimated cost recoveries. The

Company estimates future cash flows based on its experience and

knowledge of the market in which the store expected to be closed

is located. However, these estimates project cash flow several

years into the future and are affected by variable factors such as

inflation, real estate markets and economic conditions.

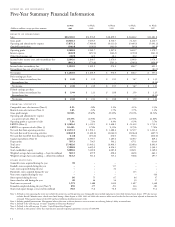

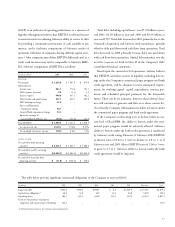

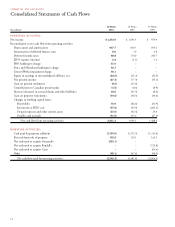

Liquidity and Financial Resources

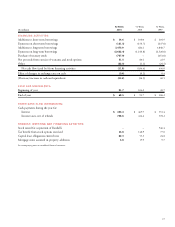

Net cash flow from operating activities was $2,231.3 million in

2001, $1,901.1 million in 2000 and $1,488.4 million in 1999. Net

cash flow from operating activities increased in 2001 and 2000

largely due to increased net income and changes in working capital.

Cash flow used by investing activities was $2,242.3 million in

2001, $1,481.0 million in 2000 and $2,064.3 million in 1999.

Cash flow used by investing activities increased in 2001 primar-

ily because of cash used to acquire Genuardi’s, as well as

increased capital expenditures. Cash flow used by investing activ-

ities declined in 2000, as compared to 1999, primarily due to

cash used to acquire Randall’s and Carrs in 1999, offset, in part,

by increased capital expenditures in 2000 over 1999. Safeway

opened 95 new stores, including 11 former ABCO stores, and

remodeled 255 stores in 2001. In 2000, Safeway opened 75 new

stores and remodeled 275 stores.

Cash flow used by financing activities was $11.8 million in

2001, primarily due to cash flow from operations being used to

pay down debt, almost entirely offset by additional borrowings

related to the Genuardi’s Acquisition. Cash flow used by financ-

ing activities was $434.4 million in 2000 primarily due to cash

flows from operations being used to pay down debt. Cash flow

from financing activities was $636.0 million in 1999 primarily

due to borrowings related to the Randall’s and Carrs acquisitions.

Net cash flow from operating activities as presented in the con-

solidated statements of cash flows is an important measure of cash

generated by the Company’s operating activities. EBITDA, as

defined below, is similar to net cash flow from operations because

it excludes certain noncash items. However, EBITDA also

excludes interest expense and income taxes. EBITDA should not

be considered as an alternative to net income or cash flows from

operating activities (which are determined in accordance with