Safeway 2001 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2001 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

27

Standards (“SFAS”) No. 109, “Accounting for Income Taxes.”

Deferred income taxes represent tax credit carryforwards and

future net tax effects resulting from temporary differences

between the financial statement and tax basis of assets and lia-

bilities using enacted tax rates in effect for the year in which the

differences are expected to reverse.

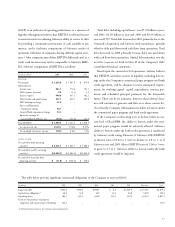

OFF-BALANCE SHEET FINANCIAL INSTRUMENTS As discussed

in Note F, the Company has, from time to time, entered into

interest rate swap agreements to limit the exposure of certain of

its floating-rate debt to changes in market interest rates. As of

year-end 2001, the Company did not have any outstanding inter-

est rate swap agreements.

FAIR VALUE OF FINANCIAL INSTRUMENTS Generally accepted

accounting principles require the disclosure of the fair value of

certain financial instruments, whether or not recognized in the

balance sheet, for which it is practicable to estimate fair value.

Safeway estimated the fair values presented below using appro-

priate valuation methodologies and market information available

as of year-end. Considerable judgment is required to develop

estimates of fair value, and the estimates presented are not nec-

essarily indicative of the amounts that the Company could real-

ize in a current market exchange. The use of different market

assumptions or estimation methodologies could have a material

effect on the estimated fair values. Additionally, these fair values

were estimated at year-end, and current estimates of fair value

may differ significantly from the amounts presented.

The following methods and assumptions were used to esti-

mate the fair value of each class of financial instruments:

Cash and Equivalents, Accounts Receivable, Accounts Payable and

Short-Term Debt. The carrying amount of these items approxi-

mates fair value.

Long-Term Debt. Market values quoted on the New York Stock

Exchange are used to estimate the fair value of publicly traded

debt. To estimate the fair value of debt issues that are not quot-

ed on an exchange, the Company uses those interest rates that

are currently available to it for issuance of debt with similar

terms and remaining maturities. At year-end 2001, the estimat-

ed fair value of debt was $7.1 billion compared to a carrying value

of $6.9 billion. At year-end 2000, the estimated fair value of debt

was $6.1 billion compared to a carrying value of $6.0 billion.

Off-Balance Sheet Instruments. The fair value of interest rate swap

agreements are the amounts at which they could be settled based

on estimates obtained from dealers. At year-end 2001, no such

agreements were outstanding. The net unrealized loss on such

agreements was $1.9 million at year-end 2000.

STORE CLOSING AND IMPAIRMENT CHARGES Safeway contin-

ually reviews the operating performance of its stores and assesses

its plans for certain store and plant closures. In accordance with

SFAS No. 121, “Accounting for the Impairment of Long-Lived

Assets and for Long-Lived Assets to be Disposed Of,” losses

related to the impairment of long-lived assets are recognized

when future cash flows, discounted using a risk-free rate of inter-

est, are less than the assets’ carrying value. At the time manage-

ment commits to close or relocate a store location or because of

changes in circumstances that indicate the carrying value of an

asset may not be recoverable, the Company evaluates the carry-

ing value of the assets in relation to its expected discounted

future cash flows. If the carrying value is greater than the dis-

counted cash flows, a provision is made for the impairment of

the assets. The Company calculates its liability for impairment on

a store-by-store basis. These provisions are recorded as a compo-

nent of operating and administrative expense and are disclosed

in Note C.

For stores to be closed that are under long-term leases, the

Company records a liability for the future minimum lease pay-

ments and related ancillary costs from the date of closure to the

end of the remaining lease term, net of estimated cost recoveries

that may be achieved through subletting properties or through

favorable lease terminations, discounted using a risk-free rate of

interest. This liability is recorded at the time management com-

mits to closing the store. Activity included in the reserve for store

lease exit costs is disclosed in Note C.

The operating costs, including depreciation, of stores or

other facilities to be closed are expensed during the period they

remain in use.