Safeway 2001 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2001 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

28

STOCK-BASED COMPENSATION Safeway accounts for stock-

based awards to employees using the intrinsic value method in

accordance with Accounting Principles Board Opinion No. 25,

“Accounting for Stock Issued to Employees.” The disclosure

requirements of SFAS No. 123, “Accounting for Stock-Based

Compensation,” are set forth in Note G.

NEW ACCOUNTING STANDARDS In June 2001, the Financial

Accounting Standards Board issued SFAS No. 141, “Business

Combinations,” and SFAS No.142, “Goodwill and Other

Intangible Assets.” SFAS No. 141 requires that all business com-

binations initiated after June 30, 2001 be accounted for under

the purchase method and addresses the initial recognition and

measurement of goodwill and other intangible assets acquired in

a business combination. In the event Safeway acquires goodwill

in the future it will not be amortized. SFAS No. 142 addresses

the initial recognition and measurement of intangible assets

acquired outside of a business combination and the accounting

for goodwill and other intangible assets subsequent to their

acquisition. SFAS No. 142 provides that intangible assets with

finite useful lives be amortized and that goodwill and intangible

assets with indefinite lives will not be amortized, but will rather

be tested at least annually for impairment. Under the provisions

of SFAS No. 142, any impairment loss identified upon adoption

of this standard is recognized as a cumulative effect of a change

in accounting principle. Any impairment loss incurred subse-

quent to initial adoption of SFAS No. 142 is recorded as a charge

to current period earnings. SFAS No. 142 was effective for

Safeway beginning on December 30, 2001 and, since that time,

Safeway has stopped amortizing goodwill. Goodwill was $5.1

billion at year-end 2001 and $4.7 billion at year-end 2000.

Goodwill amortization was $140.4 million in 2001, $126.2 mil-

lion in 2000 and $101.4 million in 1999. Other than the elimi-

nation of goodwill amortization, the Company has not yet

determined the effect that adoption of SFAS No. 142 will have

on its financial statements.

In October 2001, the Financial Accounting Standards Board

issued SFAS No. 144, “Accounting for the Impairment or Disposal

of Long-Lived Assets.” SFAS No. 144, which replaces SFAS

No. 121 and APB No. 30, became effective for Safeway on

December 30, 2001. Adoption of this standard did not have a

material effect on the Company’s financial statements.

Emerging Issues Task Force (“EITF”) Issue Nos. 00-14,

“Accounting for Certain Sales Incentives”; 00-22, “Accounting for

‘Points’ and Other Time-Based or Volume-Based Sales and

Incentive Offers, and Offers for Free Products or Services to be

Delivered in the Future”; and 00-25, “Vendor Income Statement

Characterization of Consideration from a Vendor to a Retailer,”

became effective for Safeway beginning in the first quarter of 2002.

These Issues address the appropriate accounting for certain vendor

contracts and loyalty programs. Adoption of these issues did not

have a material effect on the Company’s financial statements.

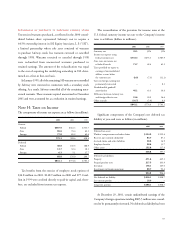

Note B: Acquisitions

The following unaudited pro forma combined summary financial

information is based on the historical consolidated results of oper-

ations of Safeway, Carrs, Randall’s and Genuardi’s as if the acqui-

sitions had occurred, all related debt was assumed and related

goodwill was recorded, at the beginning of 1999. The information

for 2001 is not materially different than actual results and is not

included. This pro forma financial information is presented for

informational purposes only and may not be indicative of what

the actual consolidated results of operations would have been if

the acquisitions had been effective as of the beginning of 1999.

Pro forma adjustments were applied to the respective historical

financial statements to account for the acquisitions as purchases.

Under purchase accounting, the purchase price is allocated to

acquired assets and liabilities based on their estimated fair values at

the date of acquisition, and any excess is allocated to goodwill.

Pro Forma

(in millions, except per-share amounts) 2000 1999

Sales $ 32,904.1 $ 31,595.9

Net income $ 1,100.9 $ 954.5

Diluted earnings per share $2.15$1.81