Sprint - Nextel 2007 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2007 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

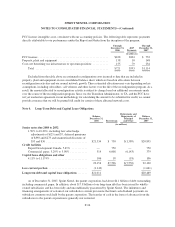

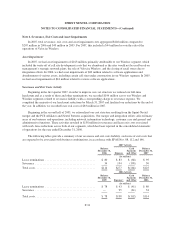

SPRINT NEXTEL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

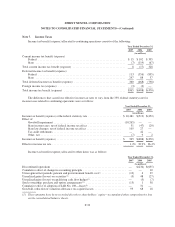

In connection with the PCS Restructuring, we are required to reimburse the former cable company partners

of the joint venture for net operating loss and tax credit carryforward benefits generated before the PCS

Restructuring if realization by us produces a cash benefit that would not otherwise have been realized. The

reimbursement will equal 60% of the net cash benefit received by us and will be made to the former cable

company partners in shares of our stock. The unexpired carryforward benefits subject to this requirement total

$187 million.

As of December 31, 2007, we had federal operating loss carryforwards of $2.8 billion and state operating

loss carryforwards of $10.5 billion. Related to these loss carryforwards are federal tax benefits of $979 million

and state tax benefits of $740 million.

In addition, we had available, for income tax purposes, federal alternative minimum tax net operating loss

carryforwards of $2.3 billion and state alternative minimum tax net operating loss carryforwards of $651 million.

The loss carryforwards expire in varying amounts through 2027. We also had available capital loss carryforwards

of $129 million. Related to these capital loss carryforwards are tax benefits of $45 million, which will expire in

2009.

We also had available $672 million of federal and state income tax credit carryforwards as of December 31,

2007. Included in this amount are $397 million of income tax credits which expire in varying amounts through

2027. The remaining $275 million do not expire.

The valuation allowance related to deferred income tax assets decreased $230 million in 2007 and decreased

$117 million in 2006. The 2007 decrease is primarily related to a reclassification to other liabilities in accordance

with the adoption of FIN 48 and the use of a capital loss on which a valuation allowance had been previously

provided. The 2006 decrease is primarily related to the use of a capital loss on which a valuation allowance had

been previously provided and the expiration of state net operating losses for which a valuation allowance had

been provided.

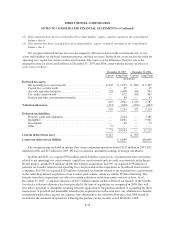

We believe it is more likely than not that these deferred income tax assets, net of the valuation allowance,

will be realized based on current income tax laws and expectations of future taxable income stemming from the

reversal of existing deferred tax liabilities or ordinary operations. Uncertainties surrounding income tax law

changes, shifts in operations between state taxing jurisdictions and future operating income levels may, however,

affect the ultimate realization of all or some of these deferred income tax assets. When we evaluated these and

other qualitative factors and uncertainties concerning our company and industry, we found that they provide

continuing evidence requiring the valuation allowance which we currently recognize related to the realization of

the tax benefit of our net operating loss and tax credit carryforwards as of December 31, 2007.

FASB Interpretation No. 48

We adopted the provisions of FIN 48 on January 1, 2007. FIN 48 clarifies the accounting for uncertainty in

income taxes recognized in an enterprise’s financial statements in accordance with SFAS No. 109 and prescribes

a recognition threshold and measurement attribute for the financial statement recognition and measurement of a

tax position taken or expected to be taken in a tax return. The cumulative effect of adopting FIN 48 generally is

recorded directly to retained earnings. However, to the extent the adoption of FIN 48 resulted in a revaluation of

uncertain tax positions acquired in any purchase business combination, the cumulative effect is recorded as an

adjustment to the goodwill remaining from the corresponding purchase business combination.

As a result of the adoption of FIN 48, we recognized a $20 million increase in the liability for unrecognized

tax benefits, which was accounted for as a $24 million increase to goodwill and a $4 million increase to retained

F-35